Japan

Wood Products Prices

Dollar Exchange Rates of 10th

April

2026

Japan Yen 159.29

Reports From Japan

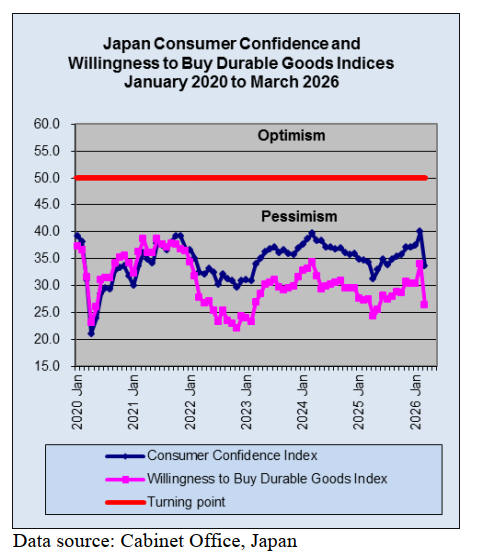

Consumer confidence - steepest decline since 2020

Japan's consumer confidence experienced its steepest

decline since April 2020 with the index plunging to 33.3 in

March 2026 driven by rising fuel costs, inflation fears and

Middle East tensions. This suggests that high inflation and

weakened sentiment will hurt household spending and

challenge the Bank of Japan's monetary policy, with

households especially worried about their livelihood and

future costs.

The decline in confidence is expected to lead to a

significant slowdown in consumer spending and the weak

data complicates the Bank of Japan's plans to raise interest

rates, as it battles with an economic slowdown. Japanese

consumers are tightening their belts due to the rising cost

of living, which is threatening the nation's fragile

economic recovery.

The latest data suggest escalating tensions in the Middle

East have already weighed heavily on Japan’s consumers,

raising the risk that softening sentiment could lead to a

decline in consumer spending. In the middle of last month,

Japan’s gasoline prices hit the highest in three decades

before coming down a little owing to government

subsidies.

See: https://www.businesstimes.com.sg/international/japans-

consumer-confidence-drops-most-covid-19

In related news, Japanese households' spending increased

at a slower pace than income over the past five years,

according to the latest Cabinet Office report indicating that

people saved more amid inflation.

According to the fiscal 2025 report on the country's

economic conditions, disposable income rose across all

age and income groups from 2019 to 2024 but

consumption growth was sluggish, with spending falling

in some groups.

The savings rate increased for all groups except those in

their 20s. Lower-income households were more affected

by inflation, as rising food costs accounted for a larger

share of their spending.

See:

https://www.nationthailand.com/blogs/news/general/40062377

Firms negatively affected by Iran crisis

A survey by Tokyo Shoko Research Ltd. showed that

around 80% of Japanese firms are experiencing negative

impacts from the ongoing crisis in the Middle East. Of

7,196 companies surveyed, 78% responded that they are

suffering negative effects.

Asked about reasons, 70%, the largest share, cited higher

costs stemming from soaring prices of crude oil-derived

materials, followed by climbing gasoline prices, cited by

65%. These response were especially prevalent in the

manufacturing and transportation sectors.

See:

https://www.nippon.com/en/news/yjj2026040900886/nearly-80-

pct-of-japan-firms-negatively-affected-by-iran-crisis.html

In related news, the Japan Center for Economic Research

(JCER) has published an assessment of how the Japanese

economy may be affected by the current oil crisis. The

analysis was prepared by Jun Saito, a Senior Research

Fellow.

JCER signals that the war in the Middle East will have a

serious effect if it last long as most of the crude oil

imported from the Middle East comes to Japan passing

through the Straits of Hormuz.

Any long term blockade of shipping through the Strait of

Hormuz will inevitably have a serious effect on the

Japanese economy through sharp drop in supply and steep

increase of prices in crude oil and everyday items

manufactured from oil based products.

See: https://www.jcer.or.jp/english/japanese-economy-

update_march-2026

Yen below 160 would be weakest in almost 40 years

In early April the yen fell to 159 to the US dollar, a rate

last seen in January.

Many suspect that if the yen drops to 160, the weakest in

almost 40 years, intervention becomes more likely The

yen lost ground against the dollar because oil prices soared

when the Middle East conflict started in late February.

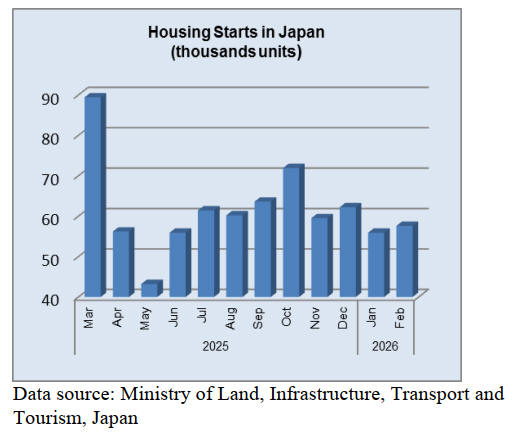

Housing starts down sharply

Japan’s housing starts fell almost 55% year on year in

February 2026 after another decline in January. The

February fall marked the fourth month of contraction and

the steepest decline since November 2025 pointing to

sustained weakness in the property sector amid higher

construction costs and soft demand.

Declines were broad-based across all segments, including

rental housing, owner-occupied homes, built-for-sale

housing, prefabricated housing and two-by-four homes.

See: https://www.mlit.go.jp/toukeijouhou/chojou/stat-e.htm

and

https://www.tradingview.com/news/providers/trading-

economics/

Strong fundamentals to support Japan real estate

outlook into 2026

According to Real Estate Asia, investor appetite for

Japanese real estate remains robust across sectors as the

real estate market continues to demonstrate resilience

despite global headwinds and rising interest rates. The

confidence is said to be “underpinned by stable economic

performance and strong corporate profits”.

See: https://realestateasia.com/commercial-other/news/strong-

fundamentals-support-japan-real-estate-outlook-2026

Japanese home builders gaining firm base in the US

Despite a cool housing market in the US Japanese builders

are moving in and soon will own 6% of the business in

America. Since 2020 Japanese builders have acquired 23

US single-family home builders, more than double the

number from 2013 to 2019. That doesn’t include the

multifamily developers and construction-supply

companies they have also bought.

Japanese companies are ramping up their presence in the

US at a time when the American home-construction

market is slowing down.

High mortgage rates have kept many US home buyers on

the sidelines. But for these Japanese builders, even a soft

US market is a better alternative than trying to expanding

at home.

See: https://www.resiclubanalytics.com/p/japanese-firms-buying-

spree-american-homebuilders-keeps-daiwa-house-trumark-

jkmonarch

and

https://www.wsj.com/real-estate/japan-is-placing-a-multibillion-

dollar-bet-on-the-u-s-housing-market-2ced2a01

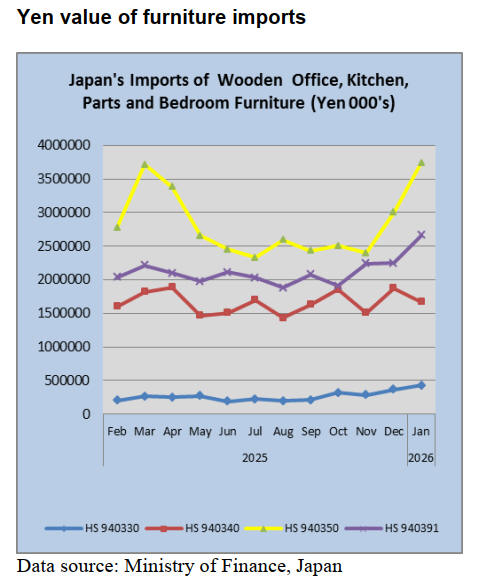

January 2026 wooden office furniture imports

(HS940330)

The value of January 2026 imports of wooden office

furniture (HS940330) was 16% higher than in December

2025 and around 8% higher than in January 2025. The top

supplier in January 2026 was China, accounting for 86 %

of imports. The other main suppliers were Turkey (2.5%)

and Italy (2.4%).

The value of imports from Turkey were considerably

higher than seen in the previous 12 months and the value

of imports from Italy, while only a small share of the value

of imports in January, was also much higher than in the

previous month.

A significant value of shipments was recorded from

Malaysia and Indonesia along with Denmark and Spain.

The top three shippers accounted for over 90% of Japan’s

January 2026 imports of wooden office furniture.

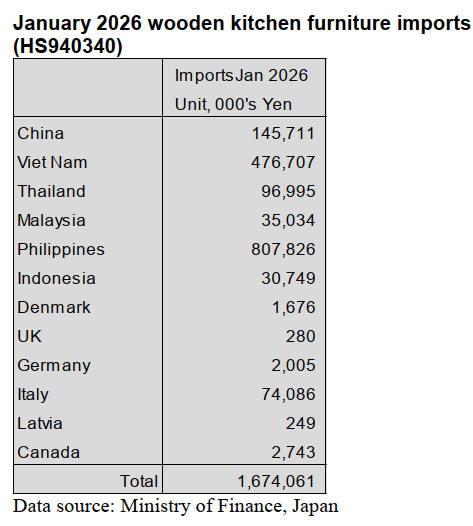

January 2026 wooden kitchen furniture imports

(HS940340)

In January 2026 the top three shippers of wooden kitchen

furniture (HS940340) were the Philippines, Viet Nam and

China. The value of shipments from the Philippines was

the highest accounting for 48% of the total value of

shipments of wooden kitchen furniture.

The other main suppliers were Viet Nam (28% of January

arrivals) and China at 9%. The other significant source of

imports of wooden kitchen furniture in January was

Thailand (6% of the monthly total).

Year on year the value of January wooden kitchen

furniture imports was down 11% compared to the valus of

December 2025 imports but 27% higher than in January

2025.

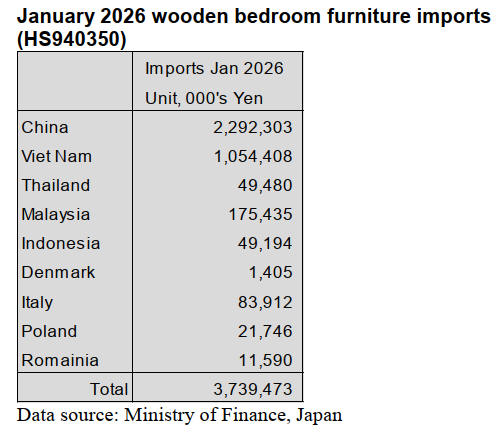

January 2026 wooden bedroom furniture imports

(HS940350)

There was a steep rise in the value of December 2025

imports of wooden bedroom furniture and the upward

trend continued into January 2026. January imports were

27% higher than in December 2025 and 8% more than in

January 2025. Over 95% of the value of HS940350 in

January was shipments from China (61%), Viet Nam

(28%) and Malaysia 9%.

The value of January shipments from China, Viet Nam

and Malaysia were all higher than in December 2025. The

other significant supplier of wooden bedroom furniture to

Japan is Italy but January arrivals were around the same

level as in December 2025. Year on year there was an 8%

rise in the value of January imports.

In January 2026 the number of shippers of wooden

bedroom furniture fell to 9 from the 15 main supply

sources in December 2025.

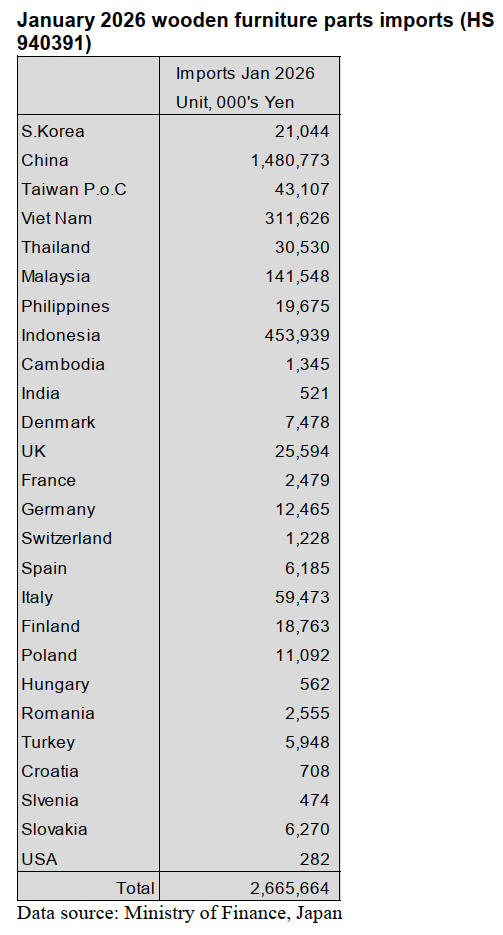

January 2026 wooden furniture parts imports

(HS940391)

Shippers in China and three SE Asian countries,

Indonesia, Viet Nam and Malaysia continued to account

for most of Japan’s imports of wooden furniture parts

(HS940391) in January 2026.

The main shipper in January was China (56% of total

imports of wooden furniture parts – 53% in December)

followed by Indonesia (17%) Viet Nam (12%) and

Malaysia (5%).

The value of arrivals of HS940391 in January 2026 from

the top three shippers, China, Indonesia and Viet Nam was

higher than in the previous month, it was only Malaysia

that recorded a slight month on month drop in the value of

shipments.

Trade news from the Japan Lumber Reports (JLR)

The Japan Lumber Reports (JLR), a subscription trade

journal published every two weeks in English, is

generously allowing the ITTO Tropical Timber Market

Report to reproduce news on the Japanese market

precisely as it appears in the JLR. For the JLR report

please see: https://jfpj.jp/japan_lumber_reports/

Lumber prices to rise further

Some lumber manufacturers belonging to the Miyakonojo

District Sawmill Cooperative in Miyazaki Prefecture plan

to raise prices for kiln-dried lumber products by ¥3,000

per cubic meter starting in March.

Freight rates, which had already been rising in stages due

to the “2024 logistics problem,” began climbing again late

last year. Shipping costs from Miyakonojo to the Kanto

region have reached ¥8,000 per cubic meter, while

transport to the Kansai region now costs ¥6,000 per cubic

meter. In addition, electricity bills, labor expenses, and

other sawmilling costs have continued to rise, prompting

industry to seek long-needed improvements in

profitability. The cooperative plans to implement further

increases in stages, with an eye toward a 10% rise within

the year.

South Sea logs and products

The supply–demand balance for tropical hardwood logs

remains stable. From late last year through January, Japan

received bulk shipments from Papua New Guinea and

container shipments from Malaysia’s Sabah and Sarawak

regions. While PNG cargoes arrived on schedule,

Malaysian container vessels were delayed by about a

month due to flooding at intermediate port following

severe rainstorms across Southeast Asia.

Loading operations in producing regions were only

slightly affected and because the delays occurred during a

period of relatively ample supply, sawmills and plywood

manufacturers were still able to secure the logs they

needed, limiting the overall market impact. The next round

of arrivals is expected around April to May, with contract

negotiations likely to accelerate once the rainy season ends

in producing regions.

For tropical hardwood and China-made products, prices

for Indonesian meranti laminated free boards have been

rising. The heavy rains that struck Southeast Asia also

caused damage in parts of Indonesia, slowing meranti log

production. Reduced log output has pushed up raw

material costs, prompting local manufacturers to move

quickly to pass these increases on to export prices. As a

result, upward price pressure is expected to continue until

production conditions normalize.

¥3,000 price hike

Acing persistently high costs across the board, Chugoku

Lumber implemented a ¥3,000-per-cubic-meter price

increase in March for its main products, including dry

beams, hybrid beams, and laminated cedar columns. This

marked the first price increase in about a year, the last one

having been implemented last spring.

Since last year, the yen has continued to weaken, with the

exchange rate fluctuating sharply in the mid-¥150 range to

the dollar. As a result, procurement costs for Douglas-fir

logs from the United States remain high. Cedar logs are

also firming nationwide due to tight supply. Over the past

one to two years, manufacturing costs—including labor

and electricity—have continued to rise. Delivery expenses

have also surged, keeping overall costs at elevated levels.

Although the company had made sustained efforts to

absorb these increases, maintaining current prices had

become difficult, leaving conditions increasingly

challenging.

Following the ¥3,000 increase, dry-beam standard

products are now priced at just over ¥73,000 per cubic

meter (delivered to precut plants), hybrid beams at slightly

above ¥80,000 per cubic meter, and laminated cedar

columns at ¥67,000 per cubic meter.

Wood demand forecast revised downward

At a meeting of the Forestry Policy Council, the Forestry

Agency presented proposed targets for the supply and use

of forest products to be included in the Basic Plan on

Forest and Forestry, which is being revised for the first

time in about five years.

The total wood demand and domestic timber utilization

targets for 2030 set in the current Basic Plan were revised

downward to reflect the declining trend in new housing

starts and a policy shift toward greater use of existing

housing stock. However, the plan again sets a target of 4.2

million cbms for domestic timber use in 2035, aiming for

an increase of 2 million cbms compared with the 2030

target.

The Basic Plan on Forest and Forestry is reviewed roughly

every five years, and the current plan was approved by the

Cabinet in June 2021. The plan sets target volumes for

total demand (domestic and imported) and domestic

timber utilization for five and ten years ahead.

At the latest council meeting, the ministry presented

proposed targets for 2030 and 2035, as shown in the

accompanying table.

For total demand for domestic and imported wood, the

category of ‘construction-use materials,’ which includes

lumber for residential and non-residential buildings, is

projected to see a modest increase. In contrast, ‘non-

construction materials,’ such as those used for pulp and

biomass power generation, are expected to remain flat

compared with 2024 levels.

Japan launches CO2 absorbing wood board

Four Japanese companies, Behomal, Swood, Kuwahara,

and Naito Architects, have jointly commercialised a new

domestically produced wood-based building material, the

“DAC Strand Board,” which absorbs and stores CO2.

They are now seeking corporate and municipal partners to

collaborate on construction projects, exhibitions, and

demonstration sites to support wider adoption of the

material. The product combines Swood’s non-oriented

strand board made from locally sourced timber with

Behomal’s CO2-absorbing material.

In addition to the strand board’s inherent carbon-

sequestration properties, the plant-derived material

developed by Behomal adds further CO2-fixing capacity.

As the material continues to absorb CO2 even after

installation, it effectively extends the time horizon of

carbon removal. The development of the DAC Strand

Board was driven by Behomal, a research-focused startup,

in collaboration with local companies across

manufacturing, design, and construction. Together, they

established an open-innovation framework that brought

regional expertise into each stage of the process.

See also: https://zenbird.media/new-japanese-building-material-

absorbs-carbon-dioxide-after-installation/

|