Japan

Wood Products Prices

Dollar Exchange Rates of 24th

April

2026

Japan Yen 158.64

Reports From Japan

Oil crisis - economic implications have been immediate

The economy in Japan is holding up well at the moment in

the face of the impact of the Iran crisis on the price of

energy imports but things could become serious if the oil

supply chain does not recover quickly. The crisis in Iran

and the disruption around the Strait of Hormuz have

driven up oil prices as about a fifth of global oil and LNG

supplies usually pass through the Strait.

For Japan, the economic implications have been

immediate. Real GDP grew 0.3% quarter on quarter in

October-December 2025 and 1.2% for the full year while

the February 2026 Consumer Price Index was up 1.3% and

unemployment stood at 2.6%. Household spending in

February fell 1.8% in real terms and consumer confidence

dropped.

What makes Japan notable is the widening gap between

relatively calm markets and a much darker mood on the

ground. The Bank of Japan said this month that regional

economies were "recovering at a moderate pace, though

some areas remain weak."

However, the outlook has deteriorated with the Cabinet

Office's Economic Survey showing the, the Economy

Watchers Outlook Index, falling in March to its lowest

level since the COVID-19 period. This has been

interpreted as suggesting consumers are likely to cut back

further on spending, particularly on discretionary

spending.

See: https://japan-forward.com/how-serious-is-the-hormuz-risk-

for-japans-economy

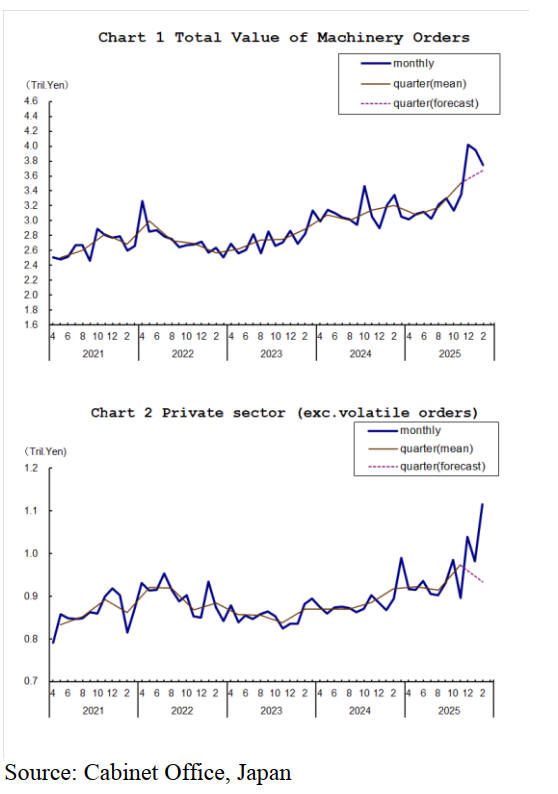

Machinery orders in February 2026

The value of machinery orders received by 280

manufacturers operating in Japan decreased by 5% from

the previous month in February. Private-sector machinery

orders, excluding those for ships and those from electric

power companies, increased by almost 14% in February.

Machinery orders are a critical leading economic indicator

in Japan. Released monthly by the Cabinet Office, data on

private-sector order (excluding volatile, large-scale ships

and electric power items) provide insights into corporate

capital expenditure trends 6–9 months ahead. They serve

as a proxy for business sentiment and planned investment

in manufacturing and non-manufacturing sectors.

See:

https://www.esri.cao.go.jp/en/stat/juchu/2026/2602juchu-e.html

2025 - Fifth year of trade deficit

Government data shows Japan suffered a trade deficit of

around US$11 billion in the last financial year, remaining

in the red for the fifth straight year. In 2025, high US

tariffs, implemented since April 2025, dragged down auto

exports, a cornerstone of Japan’s international trade.

The country's trade deficit has been declining since a

massive drop in fiscal 2022 due to the Corona Virus

pandemic but it has deepened this business year due to the

Middle East conflict which is driving up the cost of

imports especially as the yen is particularly weak at

present.

See:

https://mainichi.jp/english/articles/20260422/p2g/00m/0bu/019000c

March trade balance - good news

The latest data from the Ministry of Finance shows that

the trade balance for March 2026 was a surplus of yen 667

billion, an explosive growth compared to February. This

marked the second consecutive month of a surplus trend.

Although the overall figure still fell short of the market

consensus it indicates that, supported by external demand,

Japan's trade fundamentals are gradually recovering.

Exports in March increased by 12% year-on-year, beating

market expectations and setting a new single-month record

high, primarily benefiting from strong orders for electronic

components such as semiconductors and non-ferrous

metals. However, imports in March grew by 11% year-on-

year, significantly higher than the initially estimated 7%.

See: https://datatrack.trendforce.com/blog/content/56468/japans-

march-trade-surplus-surges-to-667-billion-yen-exports-hit-

single-month-record-high-but-import-cost-pressures-emerge

Household spending stalled

Despite household savings reaching a record high in Japan

people are reluctant to spend highlighting a growing

preference for savings amid concerns that rising oil prices

will drive inflation higher.

See:

https://mainichi.jp/english/articles/20260421/p2a/00m/0bu/022000c

Interest rates

As anticipated, the Bank of Japan (BoJ) maintained its

benchmark short-term interest rate at approximately

0.75%, the third time holding rates steady. At the same

time policymakers simultaneously raised inflation

forecasts, indicating potential future hikes.

The Bank updated projections, raising the fiscal year 2026

core inflation forecast to 2.8% (up from 1.9%) while

cutting growth projections, highlighting concerns over

energy-driven inflation.

Despite the pause, the BoJ Board indicated that monetary

tightening is their aim when economic conditions allow.

The latest decision aims to balance keeping a check on

weak yen-induced inflation while not choking off

economic growth amid global uncertainty.

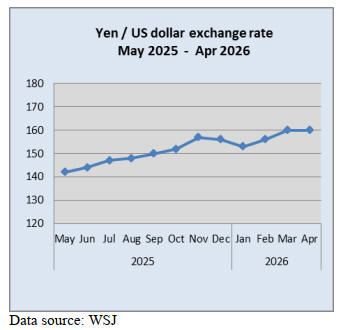

Yen steady after BoJ meeting

The yen strengthened modestly immediately following the

26 April Bank of Japan (BoJ) meeting as the Board

members delivered a "hawkish tone." Although rates

remained at 0.75%, three board members dissented in

favor of an increase.

The yen saw temporary support and strengthened against

the dollar bringing US$/JPY exchange rate below the 159

level. Despite keeping policy steady, the increased dissent

(3 members) in favour of a rate increase was viewed as a

move toward policy normalisation, which supported the

currency.

However, the yen breached the 160 to the US dollar in the

last few days of April.

Brisk private consumption and production across

the

country

The Ministry of Finance kept its economic assessments

unchanged for all of the country's 11 regions in its latest

quarterly report citing brisk private consumption and

production activity. The Ministry kept its overall

assessment of the Japanese economy unchanged for the

11th straight quarter, saying that it was recovering

gradually.

The ministry upgraded its view on production activity for

the Kanto eastern and Shikoku western regions. On

employment, it lowered its view for Hokkaido, the

country's northernmost prefecture. The report listed

concerns about the impact of the conflict in Iran.

See: https://www.nippon.com/en/news/yjj2026042200597/

Policymakers concerned speculative investment

driving home prices out of reach

There are signs that policymakers are growing cautious

about speculative investment that could drive home prices

out of reach. The Bank of Japan has indicated it will

monitor real estate loans by regional banks. Local

governments have warned against quick reselling of

properties.

Used condominium prices in central Tokyo fell for the

second month in March, raising concerns that Japan’s

property boom may be losing momentum and a correction

is possible.

See:

https://www.japantimes.co.jp/business/2026/04/23/economy/toky

o-used-condominium-price-fall/

Import update

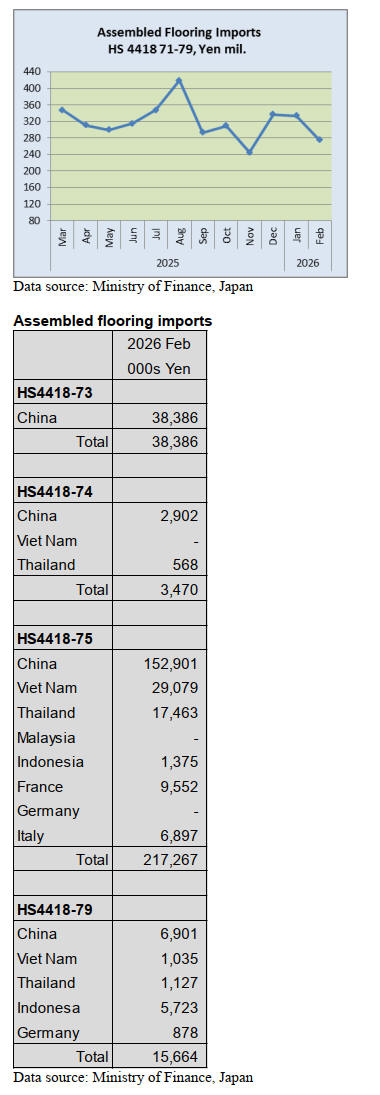

Assembled wooden flooring - Import update

Imports of assembled wooden flooring (HS441871-79)

dropped sharply in February. Shippers in China account

for most of Japan’s imports of assembled flooring and

shipments slowed due to the Spring Festival holidays.

Manufacturing activity in China historically slows

significantly during the Spring Festival (Lunar New Year),

with factory operations often pausing for 1–2 weeks and

experiencing reduced output for up to a month. In

February 2026, the official manufacturing Purchasing

Managers' Index (PMI) fell to 49.0, marking a second

straight month of contraction largely due to the holiday,

which coincided with the longest on record (February15–

23).

Shipments of HS441871-79 from China in February were

down 75% year on year and down 18% month on month.

The other main shippers also saw February shipments

slide. The drop was mainly the result of Lunar New Year

holidays celebrated in Malaysia and Viet Nam. The Lunar

New Year, known locally as Imlek, is a major public

holiday in Indonesia and this holiday also slowed output

and shipments.

Of the various categories of assembled flooring imports in

February around 75% of total imports were of HS4418-74

with most originating in China (90% in January).

All imports of HS4418-73 originated in China. For the

other categories, HS4418-79 accounted for 6% (7% in

January followed by HS4418-74 at 1.5% (4% in January).

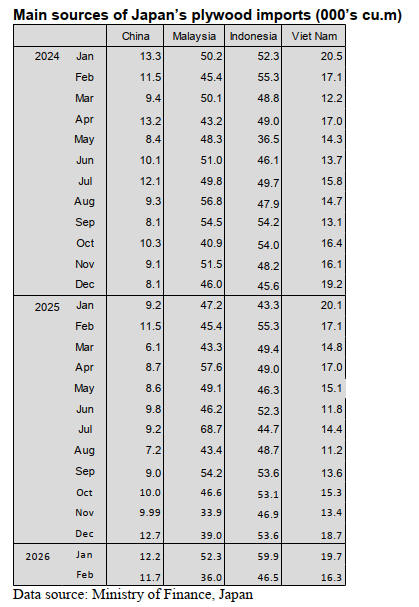

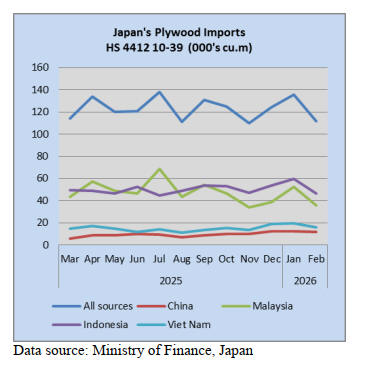

Plywood imports

In February 2026 Indonesia and Malaysia continued as the

top suppliers of plywood to Japan with the combined

volume of shipments from the two main shippers

accounting for 74% of February arrivals (83% in January).

January 2026 shipments from Malaysia were down sharply

compared to the volume shipped to Japan in January 2025

whereas shipments from Indonesia were up slightly.

The other main shippers of plywood to Japan in February

were Viet Nam and China. February arrivals from Viet

Nam were down from the previous month whereas arrivals

from China were at around the same level as in January.

In February 2026 arrivals of HS441210-39 were reported

at 111,600 cu.m (135,803 cu.m in January). As in

previous months, of the various categories of plywood

imported in January 2026, HS441231 accounted for most

followed by HS4412-33 and HS4412-34 with the balance

being HS4412-39 and HS4412-10.

Trade news from the Japan Lumber Reports (JLR)

The Japan Lumber Reports (JLR), a subscription trade journal

published every two weeks in English, is generously allowing the

ITTO Tropical Timber Market Report to reproduce news on the

Japanese market precisely as it appears in the JLR. For the

JLR report please see: https://jfpj.jp/japan_lumber_reports/

Hormuz shock hits raw materials

As the effective closure of the Strait of Hormuz enters its

second month, naphtha prices have surged, and concerns

over petrochemical supply disruptions are spreading

across global markets. What began as an impact centered

on resin-based construction materials is now extending to

engineered wood products such as plywood and laminated

lumber, both of which rely heavily on adhesives in their

manufacturing.

Some market participants have already begun moving in

anticipation of further price increases, while others are

voicing growing concern about the outlook for supply and

the possibility of additional disruptions as the situation

continues to evolve and remains difficult to foresee with

any confidence, especially given the broader geopolitical

uncertainty surrounding the Middle East.

By late March, adhesive manufacturers had not yet made

formal moves to request price increases from plywood,

laminated-lumber, or other engineered-wood producers.

Industry observers note that raw-material suppliers are

announcing price hikes at different times and with

varying timing, making it difficult for adhesive

manufacturers to determine the eventual scale of cost

increases.

The rapidly shifting situation has also made it harder to

judge whether higher prices will actually secure stable

supply, especially as discussions of production cuts

among petrochemical manufacturers continue to circulate

and add to uncertainty across the industry as a whole,

creating a sense of unease among many involved in the

supply chain and prompting increasingly cautious

attitudes among producers and buyers alike.

Adhesive manufacturers say they are making every

effort

to ensure stable supply, though some have indicated that

certain product categories may face supply restrictions or

potential price revisions depending on procurement

conditions.

Among domestic plywood manufacturers, the degree of

impact varies depending on procurement routes and

suppliers of adhesives and adhesive raw materials, but no

major disruptions were reported in March. Plywood mills

had already begun calling for higher prices for structural

plywood in February, before the effective closure of the

Strait of Hormuz, yet sluggish demand in March has

slowed their efforts.

The possibility of adhesive price increases, combined

with rising transportation costs, is adding further strain to

the market and complicating attempts to improve

profitability for many producers who were already facing

challenging conditions and limited room to maneuver in

their pricing strategies, especially as cost pressures

accumulate and uncertainty persists.

Laminated-lumber manufacturers have not yet received

concrete requests from adhesive suppliers regarding price

increases or supply adjustments. For now, they are focused

on passing through higher import costs for whitewood and

redwood lamina—cost increases driven by the weaker

yen— as they move from March into April.

Many manufacturers have also begun considering the scale

and timing of additional price increases from May onward,

reflecting the growing pressure they face as procurement

costs continue to rise and as the broader market

environment becomes increasingly uncertain and difficult

to navigate, with little clarity on how long current

conditions may persist or how severely they may intensify

in the months ahead, particularly if the geopolitical

situation remains unstable and continues to influence raw-

material markets.

Manufacturers of petrochemical-based building materials

have been announcing significant price increases one after

another. Kaneka Kentec will raise prices for extruded

polystyrene foam by 40 percent for orders placed on or

after April 1, while DuPont Styro will implement a similar

40 percent increase from May 1.

Both companies cite rising procurement costs due to the

weaker yen and the deteriorating situation in the Middle

East, along with continued increases in logistics expenses.

Other companies, including Otani Paint, Fukuvi Chemical

Industry, Sangetsu, Achilles and Oshika have announced

supply controls or potential price revisions across a wide

range of petrochemical products.

Some have already begun shipment adjustments and have

indicated that further increases may be unavoidable if

procurement conditions worsen, particularly for products

that rely heavily on petrochemical-derived raw materials

whose availability is becoming more uncertain as the

situation develops and remains unstable, with companies

preparing for the possibility of prolonged constraints and

further volatility.

Logistics costs are also rising. With crude oil prices

surging, five major container carriers—Maersk, ONE,

Hapag-Lloyd, CMA CGM and MSC—have introduced

emergency fuel surcharges ranging from USD 50 to 200

per container. These surcharges apply to all long-haul

routes and are expected to raise transportation costs for

imported materials, particularly European products that

require long-distance shipping. European suppliers have

already been informed of the surcharges and have begun

reconsidering their second-quarter contract prices.

As a result, negotiations are expected to begin later than

planned, with a strong upward pricing stance that reflects

the increasingly difficult procurement environment and the

uncertainty surrounding future supply conditions as the

situation in the Middle East continues to unfold and shows

no clear sign of resolution, leaving many market

participants wary of further volatility and preparing for the

possibility of prolonged instability in both supply and

pricing across multiple sectors that depend on

petrochemical-related materials.

Plywood

Domestic demand for Japanese softwood structural

plywood remains weak due to sluggish housing starts,

though geopolitical tensions in the Middle East have

triggered some speculative buying. The effective closure

of the Strait of Hormuz has raised concerns about adhesive

raw-material supplies, and some manufacturers are already

facing procurement limits for April.

This uncertainty has led certain buyers to place larger-

than-usual orders, even as plywood mills maintain a

cautious stance because their inventories are not abundant

and raw-material outlooks remain unclear.

Manufacturers had planned to raise prices for 12-mm

softwood structural plywood above ¥1,100 per sheet from

March, but actual market prices in the Tokyo area settled

at ¥1,040–1,060. With raw-material costs expected to rise

further, producers are pushing more firmly for price

increases in April.

Imported tropical hardwood plywood is experiencing

similar dynamics. Concerns about future supply and

expectations of higher prices have prompted some

domestic buyers to secure physical stock. In Tokyo,

coated formwork plywood is trading at ¥1,840–1,900 per

sheet, while standard formwork and structural plywood

remain around ¥1,620. Indonesian ordinary plywood

also shows stable pricing across major thicknesses.

Export prices for tropical hardwood plywood remain firm.

Indonesian ordinary plywood is offered at US$970 per m³

for 2.4-mm panels, US$880 for 3.7-mm, and US$850 for

5.2-mm. Prices for 12-mm coated formwork, formwork,

and structural plywood remain unchanged.

Indonesian manufacturers appear inclined to delay

contract negotiations in hopes of passing on rising

adhesive and freight costs.

Domestic logs and lumber

Domestic Japanese softwood products—especially

cedar—remain in tight supply in the Kanto region. Precut

factories have recently been actively securing 4-meter KD

premium-grade cedar bracing, quickly reducing available

volumes, though overall market activity is sluggish and

prices stay flat at ¥65,000–70,000 per m³.

Some precut factories are shifting from whitewood to

cedar as a more economical option, reflecting weak

whitewood demand. Cedar beams (4 m × 105 mm) are

also harder to source, though prices remain steady at

¥63,000–65,000 per m³.

Douglas fir products saw slow movement in March.

Meanwhile, KD premium-grade cedar studs (3 m × 105

mm) continue to sell briskly in direct-to-user channels,

with some wholesalers calling supply “tight.”

Some sawmills have raised direct-shipment prices by

about ¥2,000, bringing transactions to ¥60,000–62,000 per

m³, though the wholesale market remains subdued.

In log markets, Japanese cypress has seen notable

declines. In the Chugoku region, post-grade logs dropped

to ¥18,000 per m³ and sill-grade and medium-diameter

logs to ¥17,000, each down ¥6,000. Kyushu and Tochigi

also saw continued declines, extending a trend since last

autumn.

High prices last fall encouraged more harvesting, while

demand, especially for sill products, slowed, contributing

to the downturn.

New U.S. certification for Japanese timber

The Japan Wood Products Export Association announced

on January 8 that the ALSC (American Lumber Standard

Committee) has approved design values for Japanese cedar

timber.

In the United States, structural lumber is generally

classified as “lumber” for residential 2x4 materials with a

cross-sectional thickness of less than four inches and as

“timber” for larger sections,those with a thickness of four

inches or more,used mainly in commercial buildings such

as stores and offices.

With the ALSC’s approval, Japan has effectively laid the

groundwork for exporting larger-section cedar products—

such as square and rectangular timbers—to the U.S.

market.

Japan’s government is stepping up support for domestic

timber exports, and the industry is aiming to expand sales

channels for higher value-added structural lumber in the

U.S., the world’s largest market for wood-frame housing.

Japan has already obtained ALSC approval for design

values for domestically produced structural lumber,

cypress in April 2024 and cedar in April 2025, allowing

both to be used as 2x4 structural materials.

This marks the third such approval, following a project

commissioned to the Japan Lumber Inspection & Research

Association and carried out with support from Oregon

State University and the Forestry and Forest Products

Research Institute.

According to the Association, efforts are now underway to

obtain approval for cypress timber as well, a move that is

expected to support the development of overseas markets

for Japan-style homes built with traditional post-and-beam

construction using cedar and cypress.

Japan’s flat-home market surges

The share of single-story homes in the housing market is

on the rise. According to the Ministry of Land,

Infrastructure, Transport and Tourism’s Building Starts

Statistics, single-story homes accounted for 22.4% of all

residential units started in 2025, up 5.7 percentage points

from the previous year.

Even looking only at the past five years, the share has

risen steadily, from 12.4% in 2021 to 13.5% in 2022,

14.9% in 2023, and 16.7% in 2024, before surpassing 20%

in 2025. In terms of unit numbers, annual starts hovered in

the 50,000 range from 2021 to 2023, climbed into the

60,000 range in 2024, and exceeded 80,000 in 2025.

One factor behind the trend is the expansion of single-

story home offerings by major housing manufacturers,

along with increased supply of single-story subdivisions

by builders in suburban and regional markets. Franchise-

based homebuilders are also seeing strong sales of single-

story models. The industry’s push toward single-story

homes is driven by factors such as shrinking household

sizes, the need for senior-friendly layouts, and efforts to

reduce the amount of building materials used.

The rise in single-story homes may also reflect the impact

of the April 2025 revision to the Building Standards Act,

which narrows the scope of the Category 4 exemption.

Japan’s building confirmation system, similar to building-

permit reviews in other countries, was revised to tighten

oversight of most structures. While building confirmation

reviews have become mandatory in principle under the

amended law, single-story wooden structures with a total

floor area of 200 square metres or less are now classified

as “new Category 3 buildings” and remain exempt from review.

|