US Dollar Exchange Rates of

24th

April

2026

China Yuan 6.82

Report from China

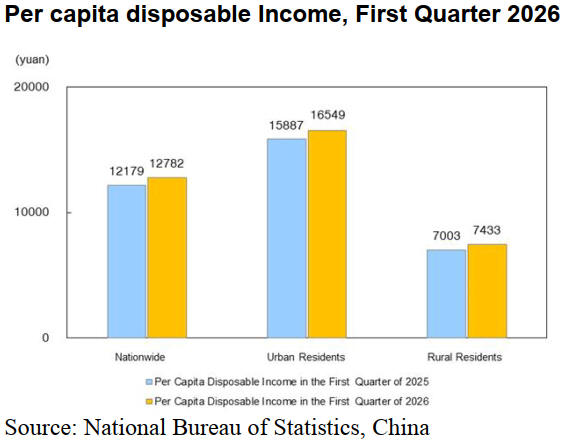

Rise in per capita income

The National Bureau of Statistics has reported Household

Income and Expenditure in the first quarter of 2026. The

nationwide per capita disposable income was 12,782 yuan,

a nominal increase of 4.9% over the same period of the

previous year and a real increase of 4.0% after deducting

price factors.

The per capita disposable income of urban residents was

16,549 yuan, an increase of 4.2% and the per capita

disposable income of rural residents was 7,433 yuan, an

increase of 6.1%.

Per capita disposable Income, First Quarter 2026

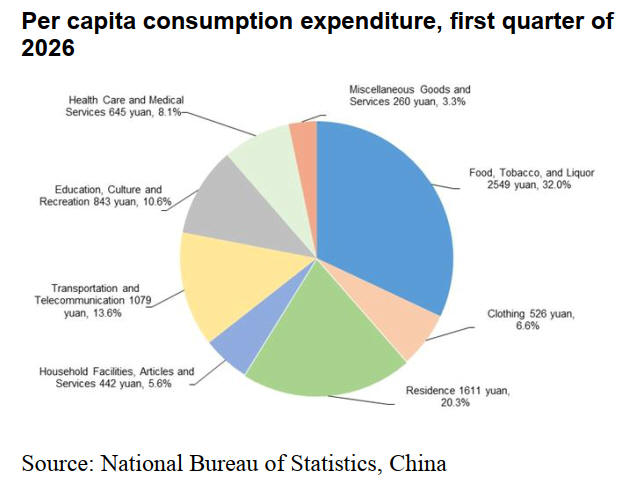

Household consumption expenditure

In the first quarter of 2026 the nationwide per capita

consumption expenditure was 7,955 yuan, a nominal

increase of 3.6% over the same period of the previous

year. The per capita consumption expenditure of urban

residents was 9,635 yuan, an increase of 2.9% and the per

capita consumption expenditure of rural residents was

5,569 yuan, an increase of 4.4%.

Per capita consumption expenditure, first quarter of 2026

In the first quarter, the nationwide per capita consumption

expenditure on household facilities, articles and services

was 442 yuan, an increase of 6.1%, accounting for 5.6% of

the per capita consumption expenditure.

See:

https://www.stats.gov.cn/english/PressRelease/202604/t2026041

7_1963349.html

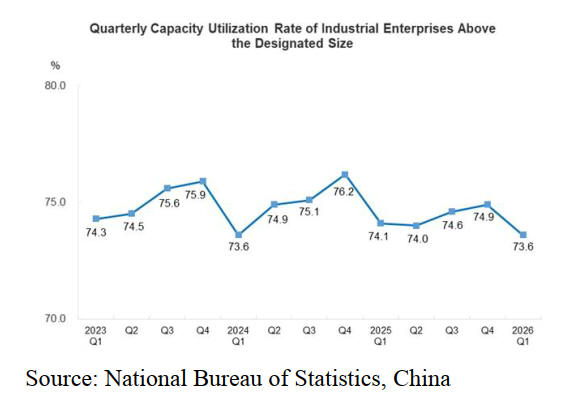

Industrial capacity utilisation rate

In the first quarter of 2026 the capacity utilisation rate of

industrial enterprises above the designated size nationwide

was 73.6%, down by 1.3 percentage points from the fourth

quarter of the previous year and down by 0.5 percentage

points from the same period of the previous year.

In terms of three main sectors in the first quarter of 2026,

the capacity utilisation rate of the mining industry was

72.1%, that of the manufacturing industry 73.9% and that

of the production and supply of electricity, gas and water

was 71.9%.

See: https://www.stats.gov.cn/english/PressRelease/202604

Canada initiates anti-dumping/subsidy investigations against Chinese

plywood

The Canada Border Services Agency (CBSA) has initiated

investigations under the Special Import Measures Act in

respect of alleged injurious dumping and subsidising of

decorative and other non-structural plywood originating in

or exported from China. The investigations follow a

complaint filed by Columbia Forest Products (CFP),

Hearst, Ontario and the Canadian Hardwood Plywood and

Veneer Association (CHPVA).

The goods subject to investigation fall under the following

HS tariff classifications: 4412.10.00.00, 4412.31.00.00,

4412.33.00.10, 4412.33.00.20, 4412.33.00.30,

4412.33.00.90, 4412.34.00.00, 4412.39.00.10,

4412.39.00.21, 4412.39.00.22, 4412.39.00.23,

4412.39.00.90, 4412.91.00.00, 4412.92.00.00 and

4412.99.00.00.

The CBSA will investigate whether imports are being

dumped and/or subsidised and will make preliminary

decisions within 90 days of 10 April at which time

provisional duties may apply.

See: https://www.cbsa-asfc.gc.ca/sima-lmsi/i-

e/donp22026/donp22026-in-eng.html

Panel industry has entered era where human values

become decisive

The ‘2026 Guangzhou Custom Furniture Exhibition and

the ‘57th China Home Industry Fair’ (Guangzhou)’ was

concluded.

One conclusion was that an industry direction has become

clearer as eastern aesthetics infuses the board materials

with cultural warmth, hardcore technology builds a solid

health foundation and humanistic care defines a new

height of value.

For enterprises, only by embracing eastern aesthetics,

delving into technology and reconstructing the value logic

can they establish a firm footing in an industry under

transformation.

For consumers, the future choice of board materials is

essentially a choice of lifestyle, health needs and cultural

preferences. There is no need to make trade-offs between

environmental protection, appearance level and

functionality.

The E1-level standard merely marks the beginning of an

industry transformation. The competition for human value

will be the ultimate battlefield of the industry. Departing

from Guangzhou, Chinese wood panel materials are

moving from Made in China to Created in China and from

Material Suppliers to Life Style Service Providers. With

the spirit of the East and the backbone of technology, they

are creating a new global brand for Chinese wood panel

materials and opening a brand-new chapter for the high-

quality development of the industry.

See:

https://www.wood365.cn/Industry/IndustryInfo_283962.html

China's exports of woodworking machinery and

accessories - US$2 billion in 2025

As one of the world's largest suppliers of woodworking

machinery and furniture accessory suppliers China's

exports of woodworking machinery (including

accessories) reached US$2.308 billion in 2025. Of the

total, the Asian market accounted for nearly 50%.

Southeast Asia contributed over 60% of the growth in the

Asian market becoming the driving force for exports.

Currently, the furniture industry in Southeast Asia is in a

period of capacity expansion and equipment upgrading. As

a result of the global shift in industrial production furniture

production capacity is shifting from China, Europe and the

United States to Southeast Asia.

It has been estimated that the total investment in the

furniture manufacturing sector in Southeast Asia reached

US$131 billion in 2025, with a year-on-year growth of

approximately 19%.

Most of the manufacturing plants in SE Asia are small and

medium-sized enterprises and face problems such as

outdated equipment and an automation rate of less than

30%.

They plan to update their equipment and at the same time

raise the self-sufficiency rate of raw materials to lower

dependence on imports.

Against the background of the reshaping of the global

economic landscape and the persistent sluggishness of

demand in Europe and the United States, Southeast Asia

has emerged as the major overseas market for Chinese

enterprises in woodworking machinery, accessories and

raw materials.

According to 2025 data, Viet Nam, with its strongest

manufacturing capacity, the most vigorous demand for

equipment and materials and the most closely coordinated

China-Viet Nam supply chain has become the foundation

of Chinese machinery and accessory suppliers.

In addition, Malaysia, Indonesia and Thailand constitute a

diversified matrix for Chinese enterprises to go global in

Southeast Asia. Overall, Viet Nam is the top priority

market for Chinese woodworking machinery and

accessory enterprises to expand their business. The main

reason for this is:

Viet Nam, as a rising star in global furniture exports, has

seen a simultaneous surge in capacity expansion and

equipment renewal. It has the highest reliance on China's

woodworking machinery, wood panels and accessories

and Viet Nam imports and growth rate rank first in

Southeast Asia.

The Vietnamese furniture industry focuses mainly on low-

end export assembly work and this is highly compatible

with the mid-range equipment and general materials

available in China. The cost for Chinese machinery

exporters to adapt equipment for Viet Nam is low and the

two-way timber trade between China and Viet Nam has

further strengthened the synergy of the industrial chain.

Viet Nam has a high dependence on products from China.

Vietnam's imports of woodworking machinery and

accessories from China reached US$420 million in 2025,

an increase of 18% on 2024. China became Viet Nam's

largest supplier of woodworking machinery in Southeast

Asia. Among these, the import growth rates of high-end

products such as automated panel saws, edge banding

machines and CNC equipment exceeded 25%.

Analysts suggest in the short term, Chinese enterprises

should seize the opportunity for equipment renewal by

Southeast Asian furniture manufacturers, leveraging their

cost-competitive advantages and the benefits of the RCEP

policy to quickly capture market share.

In the medium term it was suggested enterprises could

establish a regional value chain of Chinese R&D +

Southeast Asian production + global sales, promoting

product localisation and service localisation to reduce

trade risks.

In the long term, they should rely on the growth potential

of the Southeast Asian market to achieve an upgrade from

product export to brand, seizing the initiative in the

reshaping of the global furniture industry landscape and

promoting the expansion of China's woodworking

machinery and furniture industries.

See:

https://www.wood365.cn/Industry/IndustryInfo_284000.html

China GTI report for March

Data from the China Green Times revealed that China's

annual timber output reached 140 million cubic metres in

2025, an increase of almost 37% from 2020. The output

value of wood processing and the manufacturing of wood-

and bamboo-based products stood at 3.4 trillion yuan and

the total value of customised home furnishings exceeded

300 billion yuan.

To-date, China's forestry and grassland industry has

formed four pillar sectors, wood and bamboo processing,

economic forests, ecotourism and non-timber forest-based

economy, each with an annual output value exceeding one

trillion yuan making the country the world's largest

producer, consumer and trader of major forest products.

In terms of sustainable forest management, China is also

making rapid progress. In 2025, the country completed

afforestation and forest improvement on around 3.56

million hectares, while the three-year pilot programme for

sustainable forest management covered an area of over

2.66 million hectares. In the real estate sector, the Chinese

government is working to stabilise the property market

and promote the construction of better homes.

The latest government work report stressed the need for

city-specific policies to control new supply, reduce

existing inventory and optimise housing availability while

accelerating the renovation of dilapidated and unsafe

housing and methodically advancing the construction of

homes which are safe, comfortable, green and smart.

In March 2026 China released the Outline of the 15th

Five-Year Plan (2026-2030) for National Economic and

Social Development which proposes improving the

housing security system and promoting the stable and

healthy development of the real estate market, moves

expected to drive further improvement in demand for the

timber industry.

In March 2026 the GTI-China index registered 61.1%, an

increase of 30.0 percentage points from the previous

month and rose above the critical value (50%) after five

months, indicating that the business prosperity of the

timber enterprises represented by the GTI-China index

expanded from the previous month.

The main reason was that enterprises fully resumed work

and production after a long Spring Festival holiday, with

both production volume and new orders in the timber

industry increasing significantly from the previous month.

Regarding the twelve sub-indices, all (production, new

orders, export orders, existing orders, inventory of finished

products, purchase quantity, purchase price, import,

inventory of main raw materials, employees, delivery time

and market expectation) were above the critical value of

50%. Compared to the previous month all the twelve

indices had increased with growth ranging from 7.7 to

44.3 percentage points.

The challenges reported by enterprises included

insufficient orders, high cost of raw materials, weak and

intense price competition.

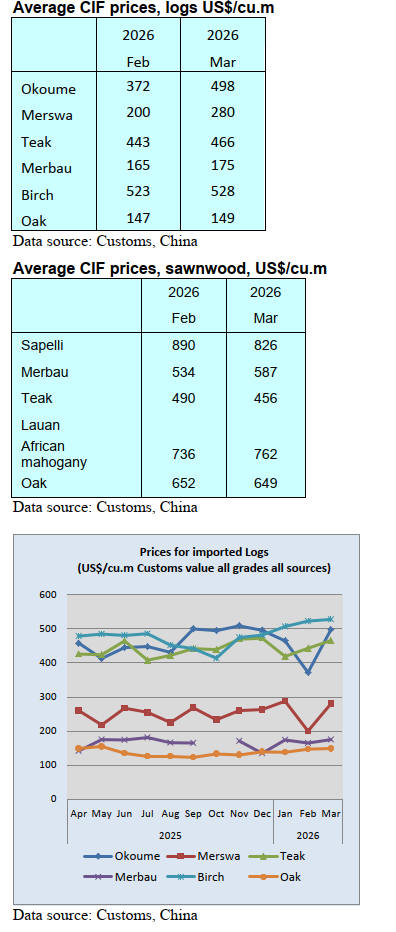

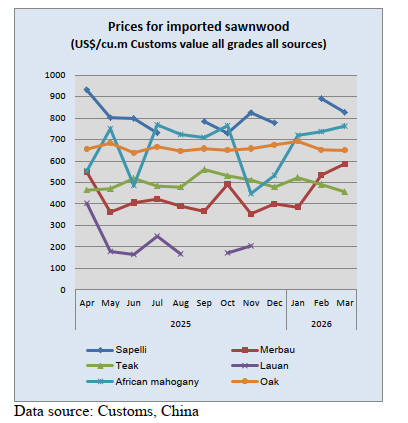

Price trends

|