|

Report from

Europe

Anti-dumping measures drove shift in European

plywood imports

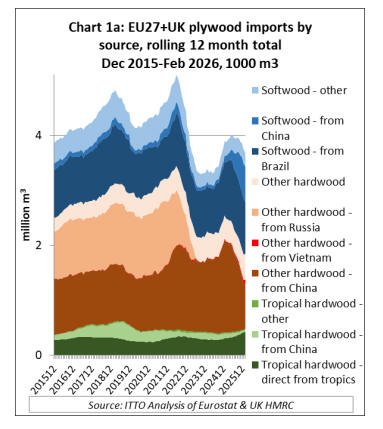

Total EU+UK imports of plywood from outside the region

in 2025 were 3.87 million cu.m, up 3% compared to 2024.

Import value was US$1819mil. in 2025, the same as the

previous year.

This apparent stability in overall imports last year

obscures major shifts in the sourcing of plywood by

European manufacturers, particularly driven by anti-

dumping measures imposed by the EU. Looking at the

data more closely, it becomes clear that total imports

increased rapidly in the first half of 2025 but then fell

sharply in the second half of the year (Chart 1a).

The decline in EU+UK imports in the second half of the

year followed imposition of provisional anti-dumping

duties of 62.4% on EU imports of all hardwood plywood

from China, excepting only those from a single Chinese

supplier for which a preliminary duty of 25.1% was

imposed after they provided additional information during

the EU’s anti-dumping investigation.

On 19 November 2025, a definitive duty of 86.8% was

imposed on all EU imports of hardwood plywood from

China, excepting products from the one company that

provided additional information which is subject to 43.4%

duty.

EU+UK imports of Chinese plywood faced with temperate

hardwood fell 40% to 959,800 cu.m in 2025, while

imports of Chinese plywood faced with tropical hardwood

were down 58% to 38,200 cu.m.

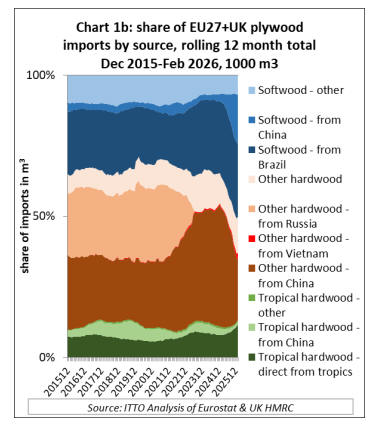

In terms of share of total plywood import quantity in the

EU+UK region, the share of Chinese temperate hardwood

products fell from 43% in 2024 to 25% in 2025 while the

share of Chinese tropical hardwood products fell from

2.4% to just 1% over the same period (Chart 1b).

The imposition of definitive anti-dumping duties implies

this downward trend will likely continue. The duties do

not apply in the UK, but the UK’s large plywood

importers also sell into the EU single market, notably in

Northern Ireland and are also expected to reduce their

imports of Chinese hardwood plywood in the future.

Direct EU+UK imports of tropical hardwood plywood

from tropical countries made significant gains in 2025.

Import volume increased 36% to 405,800 cu.m while

import value was up 22% to US$266m. The share of direct

imports of tropical hardwood plywood in total EU+UK

plywood imports increased from 7.9% in 2024 to 10.5% in

2025.

This rise in volume and share for Europe’s direct imports

of tropical hardwood plywood showed signs of

accelerating in the opening weeks of 2026.

This trend may well continue, particularly following the

EU’s decision to impose definitive anti-dumping duties of

5.4% on Brazilian softwood plywood on 15 April 2026.

Provisional duties at the same rate had already been in

effect since 5 November 2025.

The EU+UK imported 1,043,900 cu.m of softwood

plywood from Brazil in 2025, 9% more than the previous

year. The share of Brazilian softwood plywood in total

EU+UK imports increased from 25.3% in 2024 to 27.0%

in 2025. However, by the end of February 2026, EU+UK

imports of this commodity were already down 30%

compared to the same period in 2025, this at a time when

there is typically a rush to import before the annual duty-

free quota is fulfilled.

However, almost inevitably, the potential gap in supply

that opened following the imposition of EU anti-dumping

duties imposed on hardwood plywood from China and

softwood plywood from Brazil is now being filled by a big

increase in EU+UK imports of softwood plywood from

China.

EU+UK imports of Chinese softwood plywood increased

six-fold from 95,000 cu.m in 2024 to 630,000 cu.m in

2025. The primary raw material for coniferous plywood

exported from China to European markets is understood to

be radiata pine imported in log form from New Zealand.

Plywood production and consumption still slow in

Europe

While EU plywood manufacturers have been very actively

engaged in raising anti-dumping concerns with the

European authorities to boost market prospects for their

own products, the signs are this has yet to raise domestic

production levels.

Data for EU wide production of plywood in 2025 is not

yet available, but production in Finland, a leading supplier,

is projected to have fallen 5% last year, impaired by high

raw material and production costs and continuing market

volatility.

The combined effects of import stockpiling in advance of

the definitive anti-dumping duties and weak activity in the

European construction sector have dampened overall

demand. Construction activity has been slow in Europe in

the last twelve months, and the latest data suggests this

trend is set to continue.

The latest PMI data from S&P Global indicates that

eurozone construction activity was contracting in the first

quarter of this year.

The PMI posted 44.6 in March, well below the 50.0

threshold separating growth from contraction, and falling

from 46.0 in February, signaling that activity continued to

fall sharply, with the rate of contraction accelerating, and

pointing to deteriorating conditions in each of the last 47

months.

The rate of decline in the eurozone construction PMI in

March was the sharpest seen for five months and

accompanied by the most pronounced reduction in new

order intakes since last October. The reduction came amid

rapid inflation in input prices during March, with inflation

at the highest level since November 2022.

Firms often pointed to surging energy prices as a key

factor behind the acceleration following the outbreak of

war in the Middle East. The conflict also led firms to be

pessimistic regarding the outlook for the coming year,

sharply reversing a brief spell of more positive sentiment

seen in February.

The three largest eurozone economies all recorded

declines in construction output during March. France

registered the strongest decrease, the strongest in a year-

and-a-half. Italian construction companies saw a renewed

and solid decline, while construction activity in Germany

bucked the wider trend to record a slower reduction.

Similarly in the UK, the S&P Global Construction Sector

PMI stood at 45.6 in March, well below the neutral 50.0

value for the fifteenth month in a row. March data

indicated a solid reduction in UK construction output,

albeit at a slightly less marked pace than in the previous

month. Residential work remained by far the weakest-

performing category.

The latest UK survey also suggested that operating

margins were under considerable pressure from a rapid

acceleration in input cost inflation. Construction

companies widely noted that the war in the Middle East

had pushed up fuel, transportation and raw material prices.

They also cited falling confidence among clients and a

lack of new project starts.

One of the few bright spots for the European plywood

trade is that freight rates have remained quite low and

stable over the last twelve months. According to the

Drewry's World Container Index, rates from Shanghai to

Genoa are currently hovering around US$3,071 per 40ft

container, while rates to Rotterdam are at around

US$2,147 per 40ft container. The latter rate has remained

broadly stable since September last year and is down from

US$3450 in July 2025 and from rates exceeding US$8000

a year earlier in 2024.

Strong start to the year for direct European imports of

tropical hardwood plywood

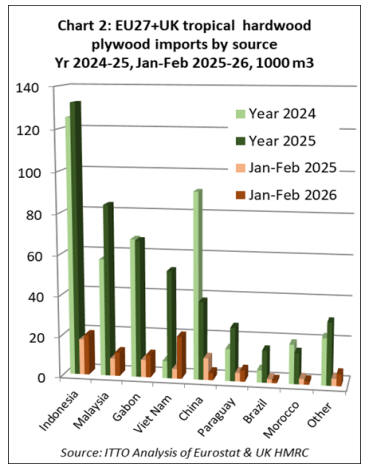

Imports of plywood faced with tropical hardwood into the

EU+UK region were 462,200 cu.m in 2025, 12% more

than in 2024. In value terms, imports increased 9% to

US$301m last year.

EU+UK imports of tropical hardwood plywood have

started this year strongly. In the opening two months, they

were 81,100 cu.m, 30% more than in the same period in

2025. Imports have increased particularly strongly from

Malaysia and Vietnam, offsetting the large decline in

imports from China. (Chart 2).

EU+UK hardwood plywood imports direct from tropical

countries were 405,800 cu.m in 2025, 36% more than in

2024. In the opening two months of this year, they were

75,000 cu.m, a gain of 55% compared to the same period

last year.

EU+UK hardwood plywood imports from Indonesia were

132,300 cu.m in 2025 and 19,700 cu.m in the first 2

months of 2026, respectively 6% and 12% more than the

previous year. Imports from Malaysia increased 46% to

83,900 cu.m in 2025 and were up 37% to 11,700 cu.m in

the first two months of this year.

EU+UK imports of plywood from Gabon were 67,000

cu.m in 2025, 1% less than the previous year. However,

they were 11,100 cu.m in the opening two months of this

year, 29% more than in the same period in 2025.

According to Eurostat statistics, the pace of increase in

EU+UK imports of tropical hardwood plywood from

Vietnam has been rapid, although from a small base.

Imports from this source increased more than five-fold to

52,700 cu.m in 2025. In the first two months of 2025, they

were 20,900 cu.m, a gain of 338% compared to the same

period last year.

EU+UK imports of tropical hardwood plywood have also

been rising from Latin America. Imports from Paraguay

were 26,300 cu.m in 2025, 67% more than the previous

year. In the opening two months of this year, they were

5,500 cu.m, 32% more than the same period in 2025.

Imports of tropical hardwood plywood from Brazil were

15,700 cu.m in 2025, a gain of 164%. Imports from Brazil

have started this year more slowly, at 1,200 cu.m in the

first two months, 33% less than the same period in 2025.

The increase in direct EU+UK imports of tropical

hardwood plywood from tropical countries has offset the

significant decline in imports from China. Imports of

38,200 cu.m from China in 2025 were 58% less than the

previous year. The decline has accelerated this year with

imports of just 3,600 cu.m in the first two months of 2026,

67% less than the same period in 2025.

Sharp fall in European imports of temperate hardwood

plywood

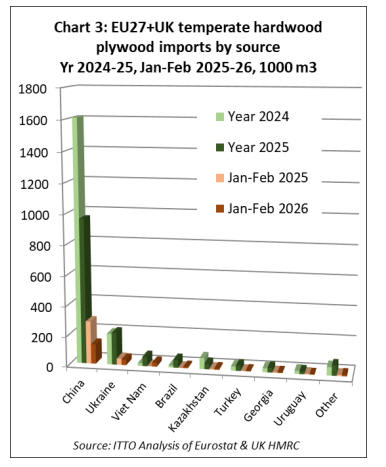

EU+UK imports of temperate hardwood plywood from

outside the region fell dramatically last year driven by the

sharp decline in imports from China, beginning in June

following imposition of the EU anti-dumping measures.

Total imports during 2025 were 1,479,000 cu.m valued at

US$795m, respectively 28% and 24% less than the

previous year. Import quantity from China fell 40% to

960,000 cu.m, while value from China was down 44% to

$392m (Chart 3).

With Russia out of the picture due to the sanctions

imposed in 2022 by both the EU and UK following the

invasion of Ukraine, no other non-EU supply country

comes to close to China in terms of volume production.

EU+UK imports of temperate hardwood plywood from

Ukraine staged a minor recovery last year, rising 4% to

214,000 cu.m, but were down 10% to 37,600 cu.m in the

opening two months of 2025.

Brazil is supplying Europe with more plywood

manufactured from hardwood plantation logs in the south

of the country. EU+UK imports of this commodity

increased 314% to 53,000 cu.m in 2025. The EU’s

imposition of anti-dumping duties on softwood plywood

from Brazil, starting November last year, seems to have

intensified this trend, with imports of non-tropical

hardwood plywood from the country reaching 8,400 cu.m

in the first two months of 2026, a four-fold gain compared

to the same period in 2025.

Vietnam is also now exporting significant quantities of

temperate hardwood plywood manufactured from

imported logs. EU+UK imports from this source increased

253% to 63,000 cu.m in 2025. In the first two months of

2026, imports of this commodity from Vietnam, at 26,600

cu.m, were nearly ten times the volume imported during

the same period in 2025.

Despite efforts in the EU+UK to crackdown on

circumvention of sanctions on Russian wood products,

temperate hardwood plywood products from countries

neighboring Russia - which may contain Russian wood -

have continued to flow into the region.

EU+UK imports of temperate hardwood plywood from

Kazakhstan fell 50% to 37,000 cu.m in 2025, but were up

again, by 53% to 8,700 cu.m, in the opening two months

of 2026. Imports from Georgia were 30,000 cu.m in 2025,

14% more than the previous year. Imports of 4,300 cu.m

from Georgia in the January to February period this year,

were 17% more than the same period in 2025.

EU+UK imports of temperate hardwood plywood from

Turkey are also increasing. They gained 27% to reach

35,000 cu.m in 2025 and were up 84% to 5,100 cu.m in

the first two months of 2026. Although early days, this is a

particularly intriguing development that might point the

way to a wider trend in the European plywood market.

There are reports of northern European plywood

manufacturers establishing new ventures in Turkey reliant

on logs imported from the EU and that sell finished

plywood back into the EU. The aim is to reduce plywood

manufacturing costs by locating in a country where labour

and energy costs are lower than in the EU, while allowing

much shorter shipping cycles compared to locations in

China and Southeast Asia and offering FSC and EUDR

compliance through their reliance on wood originating in

the EU.

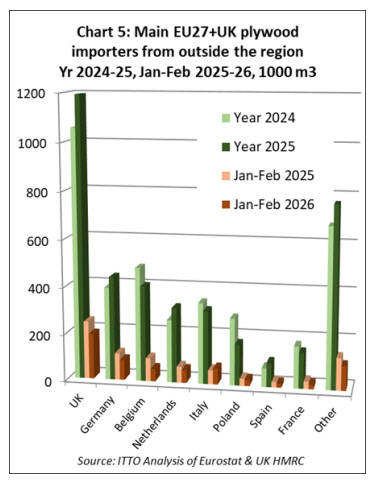

Shifting plywood destinations in Europe

The UK is by far the largest single destination for plywood

imported into the EU+UK from outside the region,

accounting for 31% of the total (Chart 5). Lying outside

the EU single market and having no domestic production,

this is not surprising.

Imports into the UK from outside the region were

1,192,800 cu.m in 2025, 13% more than the previous year.

However, UK imports so far this year have been slower,

down 22% in the first two months compared to the same

period in 2025.

Total EU imports of plywood from outside the region were

2,666,800 cu.m in 2025, a 1% decline compared to the

previous year. The decline in imports has accelerated in

the first two months of this year, down 24% to 85,400

cu.m.

Imports from outside the region increased last year into

Germany (+13% to 439,400 cu.m), Netherlands (+20% to

317,700 cu,m), and Spain (+31% to 102,800 cu.m), but

declined into Belgium (-16% to 403,800 cu.m), Italy (-

10% to 310,100 cu.m), Poland (-38% to 174,600 cu.m),

and France (-15% to 150,500 cu.m).

Imports so far this year are down significantly into nearly

all the main EU markets, the only exception being Italy

where imports are up 14% in the opening two months.

|