|

1.

CENTRAL AND WEST AFRICA

China is gradually returning to the market

Price increases are now becoming more visible in the West

and Central African timber sector. These increases are

mainly linked to higher export taxes and lower production

levels in certain key species, particularly Azobé and

increasingly Okan, where log availability remains limited.

China is gradually returning to the market, bringing some

renewed activity to the sector. Chinese-owned mills are

again actively cutting Okoume and although price

increases remain modest, operators are satisfied to see

orders returning after a quieter period.

Operators in the region say the Philippines market has

stabilised while Vietnam continues to perform strongly.

Demand remains firm not only for Tali but also for

Padouk and Ovangkol, helping to support production

levels in several exporting countries.

Demand in Europe, however, remains slow.

Environmental policies and CO₂ reduction measures

continue to affect industrial activity and construction

demand.

Across West and Central Africa the rainy season

continues, except in the central and northern regions of

Cameroon and in the CAR where conditions are drier.

Operationally, there are no major changes to report. Many

countries continue to struggle with recurring electricity

cuts.

Gabon

The Gabonese timber sector remains active despite

continued operational and financial pressures. The

domestic market for Okoume and Bilinga remains stable,

particularly for local housing and construction demand.

Okoume peeler logs supplied to the NKok Special

Economic Zone are reportedly trading around

FCFA85,000 per cu.m, with higher quality CS-grade logs

reaching as much as FCFA90,000 per cu.m. Local sawn

Okoume prices in retail outlets have increased

significantly and are now ranging between FCFA140,000

and 150,000 per cu.m.

Although estimates suggest that China’s Zhangjiagang

Port still holds roughly one year of mixed tropical log

stocks, Chinese buyers have unexpectedly returned to the

Okoume market with renewed demand bringing some

optimism to producers and exporters.

The repairs to the road between Okondja and Makokou

have now been partially completed, however, transport

conditions remain difficult due to heavy rains. Road

repairs continue across central Gabon, particularly in the

regions of Lastourville, Lopé and Makokou. Under

normal conditions, transport to Owendo Port now takes

approximately three days but bad weather still causes

delays.

Electricity disruptions continue across the country. Power

shortages remain a concern for both industrial activity and

daily operations.

Producers say the fiscal climate in the country with

regards to strict enforcement of some regulations is

creating challenges. Recently, the Forestry Task Force has

intensified tax inspections and reportedly identified more

than 50 companies with outstanding tax obligations. Land

Tax payments, originally due before 21 March 2026,

continue to be a major burden. Many companies are

seeking instalment arrangements due to weak market

conditions and the impact of increased export duties

introduced earlier this year.

Analysts suggest the outlook for Gabon remains mixed.

Chinese demand for Okoume is improving and local

construction demand continues to support domestic

consumption. However, persistent infrastructure

weaknesses, delayed government projects, electricity

shortages and increased fiscal pressure continue to weigh

heavily on the sector.

The market remains operational but cautious, with

producers closely monitoring demand recovery in Asia

and the impact of ongoing regulatory and tax measures.

Cameroon

Harvesting activity continues to increase across

Cameroon, supported by improving operational conditions

and the gradual return of Chinese demand. Production

levels are rising and most Chinese operators are now back

in operation. It appears that China’s renewed purchasing

activity is providing some support to the sector after a

prolonged slowdown.

Demand conditions remain mixed depending on

destination and species. Middle East: stable demand for

redwood species, Vietnam: continues to be a strong

market, Philippines: remains weaker than a year ago,

Europe: still slow, particularly for Padouk due to CITES

restrictions,

Italy and the Netherlands: Ayous demand remains low.

CITES regulations continue to affect trade flows,

particularly for Padouk and it has been suggested that

some operators are increasingly seeking alternative export

destinations with fewer regulatory constraints.

Environmental and regulatory pressures continue to shape

the market environment. In addition to existing EUTR

requirements and the change to the EUDR, there is

growing concern about the possible expansion of species

under CITES regulation.

Operating costs in Cameroon remain high compared to

neighbouring countries. Fuel prices are significantly above

those in Gabon, for example it has been reported petrol is

priced at around 964FCFA/litre in Cameroon versus

575FCFA/litre in Gabon and diesel is sold at: around

808FCFA/litre versus 595FCFA/litre in Gabon.

High logistics and transport costs continue to affect

competitiveness.

Republic of the Congo

Harvesting operations in Congo remain generally stable

with production continuing across both northern and

southern regions. Road repairs on laterite transport routes

are ongoing and helping improve logistics in some

production areas.

Southern Congo continues to be the country’s main

Okoume producing region while northern Congo remains

focused primarily on Sapelli, Sipo and other redwood

species. Sawmills are currently holding log stocks

estimated at two to three months of production.

No major disruptions are reported in sawmill activity.

Spare parts availability remains stable and labour

conditions are generally manageable. Port operations are

reported as stable. Pointe-Noire continues to function

efficiently as a major deep-sea hub port with no container

shortages reported.

Northern Congo operators continue exporting logs and

sawn timber through Douala and Kribi in Cameroon, while

southern operations mainly use Pointe-Noire. This split

export structure remains important due to geography and

infrastructure conditions.

Although Congo introduced restrictions on log exports the

trade continues under a quota and an authorisation system.

Demand conditions remain relatively stable. The

Philippines has reduced purchases of sawn Okoume, in

Viet Namg demand for Tali continues, demand in China

for Okoume, Okan, Ovangkol, Belli and Azobé has

become more active. In Europe demand remains very

selective for mainly redwoods.

Chinese demand is becoming increasingly important again

for the regional market.

See: https://afrinz.ru/en/2026/04/russian-orthodox-church-

receives-official-status-in-congo/

The Congolese timber sector remains operationally stable

supported by active Asian demand and functioning

logistics. However, the continued use of export quotas and

other related trade regulations has created uncertainty

around the long-term policy direction. Demand from

China and Vietnam currently remains the main support for

the industry.

2.

GHANA

Stemming illegal logging continues to be a challenge

The Ghana Timber Millers Organisation (GTMO) has

expressed concern over the increasing incidence of illegal

logging, describing it as a menace that is undermining

operations and threatening livelihoods in the sector.

The Chief Executive Officer of the GTMO, Dr. Kwame

Asamoah Adam, said the situation was forcing companies

to scale down production and lay off workers while

struggling to meet financial obligations, raising concerns

about the sustainability of the industry.

At a media briefing, he explained that, while registered

companies operate under agreements (Timber Utilization

Contracts) with the Forestry Commission to harvest timber

annually for both domestic use and export, illegal

operators are entering legally assigned concessions to steal

logs.

Dr. Adam further suggested that a large proportion of

illegally harvested timber is being exported to

neighbouring countries depriving Ghana of revenue.

Concerned civil society organisations and Ghana Coalition

Against ‘galamsey’ have expressed their concerns to the

government. They are calling for government to move

beyond routine responses and adopt a more coordinated

and decisive national strategy to stem out illegal logging.

Meanwhile, the Minister for Lands and Natural Resources,

Emmanuel Armah-Kofi Buah, has highlighted Ghana’s

efforts to combat deforestation and environmental

degradation at the ongoing 21st Session of the United

Nations Forum on Forests in New York. He outlined key

initiatives including the Ghana Forest Plantation Strategy

and REDD+ Strategy while reaffirming government’s

commitment to fighting illegal mining to protect forests

and water bodies.

500 FLEGT licenses issued

The Forestry Commission has said it is intensifying

measures to ensure forest laws compliance and curb illegal

logging through its Forest Law Enforcement, Governance

and Trade (FLEGT) licensing system.

The Executive Director of the Timber Industry

Development Division (TIDD), Dr. Richard Gyimah,

disclosed that Ghana has issued around 500 FLEGT

licenses valued at approximately Eur14.3 million covering

about 22,500 cubic metres.

He explained that under Ghana’s Voluntary Partnership

Agreement with the EU, the system has helped to ensure

that exporters comply with all legal requirements, from

obtaining valid harvesting permits to meeting social

responsibility obligations with forest fringe communities

through both digital and field verification systems to

monitor compliance.

See: https://ghanaiantimes.com.gh/ghana-timber-millers-raise-

alarm-over-rising-illegal-logging/

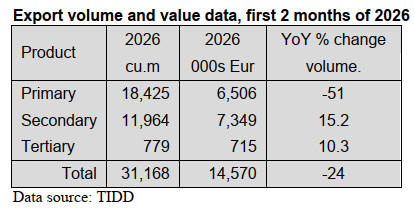

Secondary and tertiary wood products supersede

primary product exports

According to the Timber Industry Division (TIDD) report

for the first two months of 2026, wood products export for

the period were 31,168 cu.m valued at Eur14.57 million.

In the same period in 2025 the figures were 38,658 cu.m

and Eur18.15 million.

TIDD data revealed that Ghana’s primary products export

of air-dried sawnwood, billets, kindling, air-dried boules

and poles in 2026 dipped by 51% and 40% in volume and

value respectively against figures for the same period in

2025.

For the first two months of 2026 the total volume of air-

dried sawnwood exports dropped by 30% compared to the

same time in 2025. Earnings for the period also fell (-38%)

compared to the same period in 2025.

Secondary wood products export sincluding kiln-dried

sawnwood, sliced and rotary veneers and plywood

increased to Eur7.35 million in the first two months of this

year, up from the Eur6.63 million during the same period

in 2025.

Kiln-dried sawnwood exports in 2026 were 3,619 cu.m, or

12% of total export volume. This was a slight drop in

volume when compared to 2025 levels. Kiln dried

sawnwood exports generated 6% less revenue, declining

from Eur3.29 million in 2025 to Eur3.10 million this year.

Asia continued as Ghana’s leading trading partner for

wood product exports for the period January to February

2026 accounting for 18,776 cu.m in volume and Eur7.72

million in value. This represented 60% and 53% in volume

and value respectively of total wood exports for the first

two months. Compared to the same period in 2025, this

showed decreases of 28% in value and 31% in volume.

India, Viet Nam and China were the key markets while

exports to the EU market in January and February

accounting for 20% of the volume and 26% of the value of

the total export for the period, down slightly on the same

period in 2025.

Ghana’s wood exports to the ECOWAS region were

Eur1.15 million or 77% of the total export values within

Africa. The major trade was plywood shipments to

Gambia, Burkina Faso, Togo, Senegal, Benin and Nigeria.

Appeals for additional resources to protect forests

The Forestry Commission has called for increased

resources to strengthen the protection of forest reserves

across the country. Speaking to the media, the Manager of

Field Verification and Audit at the Forestry Commission,

Frank Ankomah, said illegal activities within forest

reserves continue to pose a major challenge.

He indicated some individuals invading forest reserves are

heavily armed, making it difficult for Forestry

Commission personnel assigned to protect the reserves to

confront them effectively. He therefore appealed to

government to provide the necessary resources to enable

the commission to effectively safeguard the country’s

forest reserves.

The Director of Operations for the Timber Industry

Development Division (TIDD), Mawuli Doe, also said the

Commission has intensified efforts to deal with illegal

timber operators and other offenders.

In a related development, Members of Parliament’s Select

Committee on Lands and Natural Resources have called

for urgent reforms in Ghana’s forest protection strategy

following a visit to the Nkawie Forest District in the

Ashanti Region. The Committee expressed concern over

the growing threat posed by illegal chainsaw operators,

illegal mining activities and inadequate staffing within the

Forestry Commission.

Chairman of the Committee, Collins Dauda, said the

country’s long-standing reliance on task forces to fight

illegal logging and ‘galamsey’ has failed to yield results.

Ghana has declared forest and rivers security zones where

the government has charged the National Anti-Illegal

Mining operations Secretariat (NAIMOS) to be ruthless in

dealing with illegal miners.

See: https://www.adomonline.com/forestry-commission-calls-

for-more-resources-to-protect-forest-reserves/

and

https://3news.com/news/parliamentary-select-committee-on-

lands-raises-concern-over-galamsey-illegal-logging-and-staff-

shortages-in-forest-reserves

Ghana trade delegation to participate at Carrefour

International du Bois

Following Ghana’s start of FLEGT licensing in October

2025 a trade delegation is to attend the Carrefour

International du Bois in Nantes, France in 2-4 June. The

Ghana delegation will be hosted by the ATIBT on its stand

in the Nantes Parc Beaujoire Fair complex.

On 2 June there will be an EU–Ghana Timber Trade and

Investment Forum in the Canopée meeting room at the

show ground. This will address the key issues facing the

Ghanaian timber sector in the European market and will

include a dialogue on the ‘future of collaboration between

EU and Ghana forest-based industries’.

Participants will hear an update on the European tropical

timber market, demand trends, EUDR and CITES

requirements and the prospects for FLEGT-licensed

timber presented by the European timber import sector.

ATIBT has reported a panel, moderated by a

representative from FAO will also explore EU–Ghana

collaboration opportunities in forest plantation

development, implementation of the Ghana Plantation

Strategy 2016–2040, smart forestry technologies and

potential partnerships between Ghanaian and European

actors.

This will be followed by an open Q&A roundtable and

B2B matchmaking.

ATIBT said; “This forum represents a concrete

commercial opportunity for European importers and

distributors seeking to secure their supply chains in the

face of growing requirements under the EU Deforestation

Regulation (EUDR). Ghanaian FLEGT licenses attest that

the timber is legal, traceable from forest to port and

sourced from forests managed in accordance with national

laws”.

See - https://www.atibt.org/en/news/13861/ghana-comes-to-cib-

2026-a-flegt-licensed-sector-ready-to-meet-european-markets

3. MALAYSIA

Wood-based sector facing a triple burden

The Malaysian Timber Association (MTA) has called for

government intervention warning that the wood-based

sector is facing a triple burden of higher taxes, rising

diesel costs and foreign labour shortages which have

eroded its competitiveness in global markets. The

Association also said the combined pressures are driving

up costs and constraining production in the sector.

MTA warned that “this is no longer a cyclical challenge

but a structural threat to one of Malaysia’s key export

industries”, adding that decisive policy action now will

determine whether Malaysia strengthens or surrenders its

position in the global timber and furniture market.

MTA noted that Malaysia remains among the world’s

leading furniture exporters and stressed that any prolonged

disruption to the sector risks far-reaching economic

consequences, including job losses, weakened supply

chains and erosion of global market share.

It said the expansion of the Sales and Service Tax (SST),

effective since July 2025 which removed the tax

exemption for sawn timber, has resulted in cost increases

across the entire value chain. Sawn timber is now subject

to a 5% sales tax leading to an estimated 8% to 12%

increase in downstream production costs due to a “tax-on-

tax” effect from mill to finished products.

The Association urged the Ministry of Finance to reinstate

the full tax exemption for sawn timber and recognise it as

a raw material for construction materials to eliminate

cascading cost and restore export competitiveness. In

addition, the industry is also grappling with elevated diesel

prices. Given the industry remains heavily dependent on

diesel it has no buffer against price volatility.

To mitigate the impact the MTA has proposed a targeted

fuel support mechanism, including a subsidy quota and

called for diesel prices to be capped to provide immediate

relief and stabilise the supply chain. At the same time, the

timber and furniture sector continues to face acute labour

shortages, with some mills operating at just 60% capacity

due to delays in workers quota approvals.

MTA also said the industry faces escalating recruitment

costs, including agent fees, levies, compliance, medical

screening and accommodation. Together with a multi-tier

levy system these are squeezing already thin margins,

particularly for small and medium enterprises.

“These pressures are also limiting reinvestment in

automation and long-term productivity improvements,” it

added. The Association called for a fast-tracked and one-

stop recruitment system to reduce delays and costs.

Sabah Ports congestion

The media in Sabah reports the Federation of Malaysian

Manufacturing (FMM), Sabah Branch, has raised concerns

on congestion at Sabah Ports, describing the disruption as

a manmade logistical crisis that is crippling the State’s

industrial competitiveness.

FMM Sabah chaiperson, Liaw Hen Kong, said port

operations in the State had reached a “state of paralysis”,

with severe disruptions to container trucking, frequent

vessel omissions, massive container rollovers and

prolonged delays in gate-in and gate-out activities

becoming the “new normal”.

“What is truly infuriating is that feeder operators

announced a ‘Congestion Surcharge’ and ‘General Rate

Increase (GRI)’ effective 7 May, citing the port’s failure to

clear the backlog,” he said.

“This is a direct consequence of port operational failure

and means Sabah businesses must bear the cost”, Liaw

stressed.

He said, Sabah manufacturers, already burdened by higher

raw material and fuel costs compared to Peninsular

Malaysia, are now facing soaring detention and demurrage

charges as well as additional surcharges.

Operational bottlenecks at the port have created a

significant cost-push inflationary environment. As

manufacturers absorb punitive surcharges and storage fees

they have reached a breaking point where these expenses

must be passed on to consumers. This not only erodes

public purchasing power but also stifles business

profitability” he said. The Federation urged immediate

intervention to resolve the crisis and safeguard the

competitiveness of Sabah industries.

See:https://theborneopost.pressreader.com/article/281565182380325

and

https://theborneopost.pressreader.com/article/281590952188211

Kenaf downstream industry

Malaysia is intensifying efforts to develop its kenaf

downstream industry as part of a broader strategy to

enhance agro-commodity value and support smallholder

incomes.

This was highlighted by Plantation and Commodities

Minister Dr Noraini Ahmad while visiting the non-woven

thermobonding kenaf processing plant in Saujana which is

operated by the National Kenaf and Tobacco Board. This

facility, developed with an investment of RM25 million,

has an annual production capacity of up to 2,400 metric

tonnes of non-woven kenaf products.

It is estimated these factories could generate a market

value of between RM16 million and RM18 million

annually, catering to both domestic and export demands.

Fire resistant doors from oil palm trunk

A Malaysian company has been recognised by the

Malaysia Book of Records (MBR) for developing the

country’s first fire-resistant door made from oil palm trunk

(OPT) biomass.

The MBR said the pioneering innovation transformed

agricultural waste into a high-performance building

material, marking a significant step forward in sustainable

manufacturing and green construction solutions.

It noted that Malaysia, as one of the world’s largest palm

oil producers, managed approximately 5.6 million hectares

of plantations, which accounted for about 17% per cent of

the nation’s land use.

See: https://www.bernama.com/en/general/news.php?id=2537256

4.

INDONESIA

Export benchmark prices for May 2026

Veneers

Natural Forest Veneer US$755/cu.m

Plantation Forest veneer US$946/cu.m

Wooden Sheet for

Packaging Box US$1,101/cu.m

Wood Chips

Woodchips in chips or

Particles US$90/tonne

Woodchips US$97/tonne

Processed Wood

Processed wood products which are leveled on all four

sides so that the surface becomes even and smooth with

the provisions of a cross-sectional area of 1,000 sq.mm to

4,000 sq.mm (ex 4407.11.00 to ex 4407.99.90)

Meranti (Shorea sp) US$1,346/cu.m

Merbau (Intsia sp) US$1,047/cu.m

Rimba Campuran

(Mix Tropical hardwood) US$740/cu.m

Eboni US$2,785/cu.m

Teak US$3,252/cu.m

Pinue and Gmelina US$731cu.m

Acacia US$652/cu.m

Sengon (P. falcataria) US$1,350/cu.m

Rubberwood US$433/cu m

Balsa (Ochroma sp) and

Eucalyptus. US$559/cu.m

Sungkai (P. canescens) US$1,298/cu.m

Processed wood products which are leveled on all four

sides so that the surface becomes even and smooth of

Merbau wood with the provisions of a cross-sectional area

of 4,000 sq.mm to 10,000 sq.mm (ex 4407.11.00 to ex

407.99.90) US$1,500/cu.m.

Tight log supply and soaring prices - plywood

production impacted

Indonesia’s plywood industry experienced a sharp decline

in early 2026 as a result of tight log supply and rising log

prices. The Indonesian Wood Panel Association (Apkindo)

reported that roundwood production from natural forests in

the first quarter fell by around 30% year-on-year. This

decline affected all major production regions, with

Sumatra recording the steepest drop, followed by

Kalimantan, Java-Bali and Eastern Indonesia.

Apkindo said the reduction in supply was partly caused by

the revocation of several forest concession permits, which

reduced raw material availability for processing industries.

At the same time log prices continued to climb. Meranti

log prices rose to around Rp2.5 million–Rp2.6 million per

cubic metre while prices in Java reached Rp3.8 million–

Rp4 million per cubic metre. Apkindo said the

combination of limited supply and rising prices was

reflected in plywood production figures, with national

output in March 2026 falling to approximately 158,000

cubic metres, down 31% from February and around 40%

lower than the same month last year. Overall production in

the first quarter 2026 declined by about 30% year-on-

year.

The industry’s challenges have been compounded by

soaring energy costs. Since early March 2026 industrial

fuel prices reportedly surged by around 100% due to

global energy supply disruptions linked to geopolitical

tensions in the Middle East. The higher fuel costs have

affected logging operations, transportation, factory

activities and supporting materials such as adhesives,

while international shipping costs have also become

increasingly volatile.

Apkindo warned that manufacturers now face a difficult

dilemma as rising production costs are forcing companies

to consider higher selling prices even as global demand

weakens, threatening the competitiveness and profitability

of Indonesian plywood exports.

See:

https://ekonomi.bisnis.com/read/20260502/257/1970799/produks

i-kayu-lapis-anjlok-apkindo-pasokan-seret-dan-harga-log-naik.

and

https://ekonomi.bisnis.com/read/20260504/257/1971008/manufa

ktur-tertekan-sektor-kayu-lapis-diversifikasi-tekstil-desak-

stimulus-fiskal

Calls for productivity-driven labour policies to

strengthen manufacturing competitiveness

The Indonesian Furniture Industry and Craft Association

(HIMKI) has called on the government to adopt

productivity-driven labour policies to strengthen the

competitiveness of the manufacturing sector amid growing

geopolitical and economic pressures.

HIMKI Chairman Abdul Sobur emphasised that, while

labour protection remains a fundamental principle in

industrial development, it must be balanced with the need

to improve efficiency, flexibility and global

competitiveness. He noted that Indonesia’s manufacturing

sector is facing challenges, not only from global market

conditions but also from domestic issues such as low

labour productivity and rising production costs.

To address these challenges HIMKI is advocating flexible

work policies based on productivity and output, incentives

for companies investing in workforce training and

technology and wage systems that incorporate

performance-based incentives.

The Association also urged the government to strengthen

workforce skills development programmes that are better

aligned with industry demands. Abdul Sobur added that

the effectiveness of labour policies at the implementation

stage is often influenced by public communication and

industrial relations dynamics on the ground.

See: https://www.antaranews.com/berita/5546811/himki-dorong-

kebijakan-tenaga-kerja-berbasis-produktivitas

Indonesia opens carbon market to communities and

businesses

Indonesia has introduced a new regulation opening its

forestry carbon market to communities and private sector

players in an effort to accelerate emissions trading and

maximise the economic value of its tropical forests.

Through Forestry Ministry Regulation (Permenhut) No.

6/2026, companies are now allowed to offset greenhouse

gas emissions by investing in forest conservation,

sustainable forest management and ecosystem protection.

Forestry Minister, Raja Juli Antoni, said the policy marks

a shift toward a more transparent and inclusive carbon

market after years of slow progress. The regulation is also

intended to ensure that local communities benefit directly

from conservation efforts.

The Minister emphasised that Indonesia’s new forestry

carbon trading regulation is designed to ensure greater

transparency, accountability and trust in the carbon

market. Through Ministerial Regulation No. 6/2026, the

government aims to establish a clearer framework for

businesses, local communities and international partners

involved in forestry-sector carbon trading. The minister

highlighted that maintaining integrity in carbon trading is

a top priority.

See: https://jakartaglobe.id/news/indonesia-opens-forestry-

carbon-market-to-communities-businesses

and

https://en.antaranews.com/news/414063/forestry-minister-vows-

transparent-accountable-carbon-trading

Industry welcomes new carbon trading regulation

Industry stakeholders have welcomed Indonesia’s new

forestry carbon trading regulation, describing it as a major

step toward strengthening the country’s carbon market and

accelerating the green economy.

During a forum in Jakarta discussing the regulation’s

implications, representatives from the government, the

Indonesian Chamber of Commerce and Industry and

carbon project developers said the policy provides greater

certainty for the forestry carbon sector.

Business leaders emphasised that the success of

Indonesia’s carbon market will depend on strong

coordination and trust among stakeholders. The regulation

introduces clearer project developer criteria, carbon credit

issuance procedures, participation mechanisms for

international markets and stronger environmental and

social safeguards.

However, industry players also urged the government to

quickly issue implementing rules on project risk

management and long-term investment certainty to

encourage greater green investment in Indonesia.

In related news, the Association of Indonesia Forest

Concession Holders (APHI) plans to expand forestry

carbon projects by utilising 16–17 million hectares of

natural forest within its concession areas, beyond the 16

carbon project pipelines it currently manages.

Purwadi Soeprihanto said the initiative is part of APHI’s

response to the issuance of Minister of Forestry

Regulation No. 6/2026 which regulates carbon trading

through greenhouse gas emission offsets in the forestry

sector. He explained that some concession areas will

continue to be used for timber production, while others

have strong potential for carbon credit development.

Purwadi expressed optimism that forestry carbon trading

could generate circular economic benefits for Indonesia’s

timber industry, provided the resulting carbon credits

remain competitive in the market.

He emphasised that carbon projects should not only focus

on generating carbon units, but also on delivering social

and environmental benefits. This includes benefit-sharing

mechanisms for local communities so that profits from

carbon trading are distributed more broadly, as well as

ensuring biodiversity conservation and ecosystem

protection in project areas.

See: https://ecobiz.asia/industry-welcomes-indonesias-new-

forestry-carbon-trading-regulation/

and

https://lestari.kompas.com/read/2026/04/22/093307686/kadin-

permenhut-baru-jadi-angin-segar-kembangkan-pasar-karbon-

sukarela

and

https://katadata.co.id/ekonomi-hijau/ekonomi-

sirkular/69e83badba1e9/aphi-siap-tambah-proyek-karbon-

kehutanan-pascaterbitnya-permenhut-62026

Studies to strengthen anti-corruption measures in the

forestry sector

Indonesia’s Corruption Eradication Commission (KPK) is

conducting two studies to strengthen corruption prevention

in the country’s forestry sector, focusing on corruption

risks in forest product trade and downstream processing,

as well as vulnerabilities in the governance of forest area

allocation procedures.

The initiative was launched due to the sector’s high

strategic and economic value which KPK Deputy for

Prevention and Monitoring, Aminuddin, said requires

transparent, accountable and integrity-based management.

He emphasised that the KPK’s role extends beyond law

enforcement to supporting systemic improvements in

corruption prevention.

To carry out the studies the KPK is collaborating with the

Ministry of Forestry, Ministry of Industry and Ministry of

Trade on efforts focused on integrating data, aligning

policies and strengthening supervision across the forestry

supply chain.

Aminuddin stated that the collaboration is intended to

improve regulations, oversight effectiveness and

information system integration throughout the sector. The

studies are expected to be completed in 2026 and are

intended to produce not only recommendations but also

concrete implementation measures to improve forestry

governance in Indonesia.

See: https://www.antaranews.com/berita/5547695/kpk-buat-dua-

kajian-guna-cegah-korupsi-pada-sektor-kehutanan-indonesia

Ford Foundation cooperation on customary forest

recognition

Indonesia’s Ministry of Forestry is strengthening

cooperation with the Ford Foundation to accelerate the

recognition and designation of customary forests as part of

broader efforts to improve forest governance and empower

indigenous communities in forest conservation.

The initiative was discussed during a meeting between

Forestry Minister, Raja Juli Antoni, Deputy Minister

Rohmat Marzuk and Heather Gerken, President of the

Ford Foundation. Raja Juli Antoni stated that accelerating

customary forest recognition has become a key focus of

current forestry governance reforms.

To support this goal the Ministry has established an

inclusive task force involving government institutions,

academics, civil society groups and non-governmental

organisations. The government is also seeking to

accelerate recognition for 95 Indigenous Law

Communities.

Heather Gerken reportedly praised Indonesia’s

commitment to indigenous peoples and forest protection,

saying the country has demonstrated strong global

leadership on indigenous issues following COP30.

She added that the Ford Foundation is prepared to provide

technical and legal assistance to help realise Indonesia’s

long-term vision for customary forest recognition and

conservation.

See: https://infopublik.id/kategori/nasional-sosial-

budaya/968199/kemenhut-dan-ford-foundation-perkuat-kerja-

sama-pengakuan-hutan-adat

Indonesia forms task force for national park financing

Indonesia has established a task force to develop

innovative financing mechanisms for national park

management as part of efforts to strengthen biodiversity

conservation and improve community welfare.

Hashim Djojohadikusumo, who chairs the task force,

emphasised that the initiative is aimed at protecting

ecosystems for future generations rather than

commercialising conservation areas. He stressed the

principle of “ecology before tourism,” with tourism

intended to support conservation efforts rather than

dominate them.

See: https://mediaindonesia.com/humaniora/884868/pemerintah-

bentuk-satgas-inovasi-pembiayaan-taman-nasional-dorong-

skema-di-luar-apbn

5.

MYANMAR

6.

INDIA

Duty-free access for New Zealand softwood

It has been suggested that Duty-Free access for New

Zealand softwood under the recently signed FTA may

drive down prices, raising questions about long-term

impacts on domestic log suppliers.

The Indian media has hailed the Free Trade Agreement

(FTA) between New Zealand and India, signed in April

2026 as this will open trade opportunities with duty-free

access for 100% of India‘s exports and lower tariffs for

95% of imports from New Zealand.

Mr. Agneshwar Sen, the Trade Policy Leader from Earnst

and Young (EY India) said “India has secured this without

compromising its most sensitive sectors. Dairy, edible oils,

sugar, spices, onions and key agricultural commodities are

explicitly excluded from India’s concession list, protecting

domestic farmers and industry”.

Other sensitive products, such as apples, kiwis and

Manuka honey, while not excluded, are protected through

Tariff Quote Ratios (TQR).

TQR sets limits on the amount of product that can be

exported and applies additional tariffs once those limits

are exceeded.

However, over 54% of New Zealand products, such as

wood, wool and sheep meat are duty free. Some have

raised questions about the FTA‘s impact on domestic

suppliers, especially softwood producers. As domestic

softwood production is minimal India relies on imports,

importing around 85% of its softwood. New Zealand is

one of the main exporters of softwood to India.

According to the Ministry of Commerce, in 2019 NZ

pinewood imports were valued at around US$521 million.

This dropped to US$381 million in 2020 due to the

pandemic leading to a decline in imports until 2024.

In 2024-25, imports increased to around US$587 million.

This is expected to be further amplified by the FTA,

especially given the duty-free status of wood products

from the start of the Agreement.

India’s softwood market has been estimated as growing at

11% annually and is projected to reach US$1.06 billion by

2032. This surge is driven by rapid urbanisation,

construction requirements and furniture manufacturing.

Used frequently in plywood, softwood is a cost-effective

choice for many plywood producers. However, plywood

producers in many parts of south India say they primarily

use domestic hardwoods such as rubberwood and Gurjan

for plywood production.

According to the online marketplaces IndiaMart

and TradeIndia, the current price of Indian softwood,

varying by type of wood, ranges from around INR150 to

INR1,200 per cubic foot. NZ Radiata Pine prices are said

to be around INR500 per cubic foot.

Prior to the FTA, most softwood imports from New

Zealand faced duties of around 5.5 to 11%, hence the

higher price. Given the FTA, further price declines are

expected for imported pine making the sector even more

price-competitive. Even if the shift is not immediate, the

potential drop in imported softwood prices could gradually

influence how manufacturers source materials, leading to

altered market dynamics.

See: https://www.theweek.in/news/biz-

tech/2026/05/01/softwood-imports-india-nz-fta-impact.html

and

https://www.mfat.govt.nz/en/trade/free-trade-agreements/free-

trade-agreements-concluded-but-not-in-force/new-zealand-india-

free-trade-agreement

The Maharashtra Global Furniture City

Bharat Cluster Ventures Private Limited has signed a

Memorandum of Understanding (MoU) with the State

government of Maharashtra for the development of India’s

first integrated furniture Park, the ‘Maharashtra Global

Furniture City’ said the Association of Furniture

Manufacturers & Traders.

This is envisioned as a world-class integrated industrial

ecosystem that will empower MSMEs, reduce import

dependency, create large scale employment, strengthen

exports and position Maharashtra as a global hub for

furniture manufacturing.

This MoU is not merely an agreements it is a shared

commitment to nation-building through organised

industry, innovation and collaboration, according to the

Association of Furniture Manufacturers & Traders.

See: https://www.linkedin.com/posts/bharat-cluster-ventures-

private-limited_today-marks-a-truly-historic-and-deeply-

emotional-activity-7419752788177567744-h2W8

Seeking a decentralised energy strategy

Biju Dharamapalan, Dean of Academic Affairs at Garden

City University in writing for The Pioneer, says recent

disruptions in LPG supply across several parts of India

have exposed an uncomfortable reality, the country’s

energy security rests on a fragile and highly centralised

system. In this context, the idea of social forestry deserves

renewed attention.

Introduced in India during the 1970s and 1980s, social

forestry was never just about planting trees. It was a

broader vision of community self-reliance, encouraging

villages and local institutions to grow fuelwood, fodder

and timber on common lands, roadsides, canal banks and

private fields. At its core was a simple but powerful

principle: essential resources, especially cooking fuel,

should remain locally available and sustainable.

Over the years, however, the rapid spread of LPG

connections has changed India’s energy habits. LPG

improved millions of lives by reducing indoor pollution

and relieving women of the burden of collecting firewood.

Yet it also created near-total dependence on a centralised

fossil-fuel-based system.

India already possesses strong policy frameworks for

afforestation and green development. Programmes such as

the Green India Mission, the National Afforestation

Programme, CAMPA funding and the Nagar Van Yojana

have invested heavily in restoring degraded landscapes

and expanding tree cover. Yet these initiatives are largely

viewed through the lens of environmental conservation

and carbon capture, rather than as part of a decentralised

energy strategy. Reviving social forestry today does not

mean returning to the past. It means combining traditional

wisdom with modern planning and science.

See: https://dailypioneer.com/news/why-india-must-revive-

social-forestry-for-energy-security

7.

VIETNAM

Wood and Wood Product (W&WP) trade highlights

As of early May 2026, Viet Nam's wood and wood

product (W&WP) industry has been navigating a complex

landscape marked by significant legal and trade-defense

challenges in key markets. Despite these hurdles, the

industry has remained resilient, supported by a strategic

shift toward market diversification.

While the U.S. continues to be Viet Nam’s largest export

market, exporters are actively expanding their presence in

Japan, China, South Korea, EU and the Middle East, with

approximately 45 new markets being targeted as a buffer

against potential US tariffs.

Japan has shown particularly strong growth, becoming

Viet Nam’s second-largest export destination, with exports

increasing by more than 23% over the past year. China

remains the third-largest market, driven by rising demand

for Vietnamese wood chips, with imports increasing by

around 3.5% annually in recent reporting periods. Exports

to Spain rose sharply by 63% due to strong market

demand while Canada has emerged as an important

market, especially for bedroom furniture products.

Viet Nam’s hardwood and decorative plywood exports to

the United States are currently facing severe pressure,

following the announcement of preliminary anti-dumping

and countervailing duties exceeding 190% in March 2026.

Final determinations are scheduled for May 2026.

According to statistics from the Viet Nam Customs Office,

W&WP exports in April 2026 reached US$1.43 billion, up

3% compared to March 2026, but down 1% compared to

April 2025. Of this total, WP exports accounted for

US$941.7 million, increasing by 5% month-on-month but

decreasing by 4% year-on-year. Overall, during the first

four months of 2026, W&WP exports totalled US$5.4

billion, up 0.4% compared to the same period in 2025. WP

exports contributed US$3.5 billion, representing a decline

of 5% year-on-year.

Viet Nam’s wooden furniture exports in April 2026 were

valued at US$822.4 million, up 3% compared to March

2026 but down 6% compared to April 2025.

In the first four months of 2026, total wooden furniture

exports reached US$3.1 billion, down 6% compared to the

same period in 2025.

Viet Nam’s imports of raw wood (logs and sawnwood) in

March 2026 reached 601,109 cubic metres, valued at

US$204.5 million, up 58% in volume and 58.8% in value

compared to February 2026. Compared to March 2025,

imports increased by 3% in volume and 15.0% in value.

Overall, during the first three months of 2026 raw wood

imports totalled 1.6 million cubic metres, worth US$542.7

million, representing increases of 11% in volume and 20%

in value compared to the same period in 2025.

Viet Nam’s non-timber forest product (NTFP) exports in

March 2026 were estimated at US$83.37 million,

representing a significant increase of 50% compared to

February 2026 and an increase of 6% compared to March

2025. In the first three months of 2026, total NTFP exports

reached US$239.18 million, up 14% over the same period

in 2025.

As of early May 2026, Viet Nam’s wood and wood

product industry is targeting total exports of approximately

US$18 billion for 2026.

In the first quarter of 2026, exports were estimated at

around US$3.95 billion, representing a modest increase of

approximately 1% compared to the same period in 2025.

Stronger demand from China, Japan and the EU has

helped offset weaker demand from the US market, while

many enterprises have reportedly secured export orders

through August 2026.

The Vietnamese Government plans to initiate negotiations

in June to transfer more than 5 million forest carbon

credits to the non-profit organisation Emergent at a

minimum price of US$10 per credit. These credits are

generated from projects implemented in Viet Nam’s

Central Highlands and South-Central regions.

To maintain timber exports to Europe, Viet Nam is

accelerating the completion of provincial forest boundary

databases and forest mapping systems to ensure

compliance with the EU Deforestation Regulation

(EUDR) before the end of 2026. In addition, beginning in

2026, Viet Nam has been deploying advanced

technologies including Artificial Intelligence (AI), big data

and cloud computing to monitor forest changes through

satellite imagery and strengthen forest governance and

traceability systems.

See: https://english.thesaigontimes.vn/vietnam-targets-q2-2026-

completion-of-forest-carbon-credit-issuance/

Viet Nam boosts shipments to Europe

The Viet Nam Timber and Forest Products Association

said that wood industry enterprises are accelerating

exports to the European Union (EU) as demand recovers

and EU partners increase orders. According to Viet Nam

Customs, exports of wood and wood products reached

about US$17.2 billion in 2025, up nearly 6% from the

previous year, the highest level on record.

In addition to traditional markets such as the United

States, Japan and China, exports to the EU have shown

positive signs, driven by rising demand for processed

wood products and high-end furniture. European orders

maintained a positive trend in the first months of 2026.

Many wood exporters are ramping up shipments to the

European market.

As EU demand rebounds, Vietnamese enterprises are

boosting exports and front-loading shipments ahead of

traceability requirements while investing in supply chain

digitalisation and raw material transparency.

See: https://en.sggp.org.vn/vietnams-wood-producers-

boost-shipments-to-european-market-

post123776.html?utm_source=chatgpt.com

US - 196% preliminary duties on Vietnamese hardwood

plywood

The US Department of Commerce issued preliminary

antidumping duty rates of 196.14% on hardwood and

decorative plywood imports from Viet Nam in February

this year, one of the steepest trade barriers imposed on any

wood product category this decade.

Chinese hardwood plywood faces a 187.27% rate, while

Indonesian exporters suffer rates ranging from 19.98% to

84.94%, according to the Federal Register notice

published in March.

These antidumping duties stack on top of countervailing

duties announced in January: 4.37% to 26.75% for Viet

Nam, 2.40% to 128.66% for Indonesia and a country-wide

81.34% rate for China. US Customs and Border Protection

began collecting cash deposits in March meaning

importers are already bearing these costs. Final

determinations for Viet Nam and Indonesia are scheduled

for mid-July 2026.

What's Covered and What's Not

The investigations, petitioned by the Coalition for Fair

Trade in Hardwood Plywood, target a specific product

scope: hardwood and decorative plywood. This includes

veneered panels, furniture-grade sheets and decorative

laminates used in cabinetry, flooring underlayment and

interior fit-out. Procurement managers should note that

structural plywood products, including film-faced

formwork plywood, construction sheathing and marine-

grade structural panels, fall under different tariff

classifications and are not subject to these particular

orders.

Trade barriers reshaping sourcing

The combination of steep AD/CVD duties on hardwood

plywood and Section 232 tariffs on softwood is

fundamentally reshaping procurement economics for US

importers. With combined duty rates potentially exceeding

200% on Vietnamese and Chinese decorative panels,

buyers will likely increasingly look to domestic

production, alternative sources not yet subject to orders or

reformulate their product specifications to fall outside the

scope of the investigations.

For structural and formwork plywood, which remains

outside these AD/CVD actions, the trade environment is

comparatively stable though Section 232 baseline duties

still apply. European demand offers steady growth without

the tariff complexity, while Middle East and Indian

infrastructure programmes continue to absorb volume.

Procurement teams should closely track the mid-July final

determinations, as duty rates may shift significantly from

preliminary levels.

See: https://vinawoodltd.com/blog/plywood-timber-market-brief-late-april-

2026?utm_source=chatgpt.com

8. BRAZIL

Brazil’s planted forest sector

Brazil’s planted forest sector covered 10.52 million

hectares in 2024 when the last survey was conducted,

representing a 2.8% year on year increase and

consolidating its position as one of the pillars of the

national bio-economy. Eucalyptus leads at 8.1 million

hectares, followed by pine with 1.9 million hectares,

mainly concentrated in the states of Minas Gerais, Mato

Grosso do Sul, São Paulo, Paraná and Santa Catarina.

The sector also stands out for its high productivity with

Brazilian eucalyptus reaching an average of 34.4 cu.m per

hectare per year, one of the highest rates in the world,

increasing competitiveness and reducing costs.

For rural producers, planted forests represent an

alternative for income diversification, especially with the

expansion of eucalyptus cultivation in marginal areas. This

growth follows the global demand for renewable products

with Minas Gerais standing out as one of the main

productive and industrial hubs.

In 2024, the planted tree industry generated gross revenue

of BRL240 billion, with record production of pulp (25.5

million tonnes), paper (11.3 million tonnes) and wood

panels (9.7 million cubic metres). The sector created

around 720,000 direct jobs and up to 3.86 million jobs

when considering indirect economic effects.

From an environmental perspective, expansion occurs

mainly on degraded land, contributing to soil recovery,

water resource protection and carbon capture, reinforcing

Brazil’s strategic role in the transition to a low-carbon

economy.

See: https://maisfloresta.com.br/setor-de-florestas-plantadas-

fatura-r-240-bilhoes-e-bate-recordes/

Larger area needs to be brought under management

plans

The State of Mato Grosso has consolidated itself as the

main hub of the Amazon timber industry, accounting for

44% of roundwood transactions in the region (64 million

cubic metres) and 40% of other timber products between

2010 and 2023. In 2024, the State recorded a 38% decline

in domestic market sales, while exports grew by 81%,

mainly to the United States, China and Europe, increasing

demands for traceability and environmental compliance.

One of the main challenges lies in the regularisation of the

activity, since 39% of the 2.95 million hectares exploited

in those days had no forest management plan or official

authorisation.

Although the State maintains 1.8 million hectares under

Sustainable Forest Management Plans (SFMP), experts

highlight the need to expand this area by an additional

3.24 million hectares to ensure economic, environmental

and commercial sustainability. Despite being the national

leader in forest management, illegal logging has been

reported in strategic municipalities such as Aripuanã,

Colniza and Juara.

The analysis from Imaflora highlights that Mato Grosso

has strong potential to strengthen its leadership in the

sustainable production of native Amazon timber.

However, progress in traceability, monitoring,

environmental regularisation and diversification of species

and products will be essential to improve competitiveness

in both domestic and international markets.

See: https://imaflora.org/noticias/mato-grosso-lidera-a-industria-

madeireira-na-amazonia-com-oportunidades-de-expansao-do-

manejo-e-da-rastreabilidade

Costs rising and export competiveness slipping

The escalation of geopolitical tensions involving the

United States and Iran has affected Brazilian timber

exports through higher logistics costs, increased

operational risks, changed trade routes and reduced

shipments. Consequently, this situation has put pressure

on the entire forestry production chain due to rising oil

prices and higher freight, fuel and industrial input costs in

early 2026.

Brazilian timber exports to the Middle East recorded a

sharp decline in the first quarter of 2026. After shipments

reached nearly US$18 million in January, volumes

dropped significantly in February and fell to around US$6

million in March. Countries such as the United Arab

Emirates and Saudi Arabia recorded declines of up to

80%, mainly affecting products such as pine sawnwood,

plywood and furniture.

Economic and geopolitical instability has reduced

international demand for forest products and made

strategic planning more difficult for exporting companies

as the forestry sector operates on long-term cycles. Market

volatility and rising oil prices have increased operating

costs and undermined business competitiveness and

predictability.

In response, the Brazilian forest sector is seeking to

diversify markets, strengthen the domestic market, invest

in higher value-added products and improve logistics

efficiency.

See: https://www.portaldoagronegocio.com.br/florestal/mercado-

florestal/noticias/guerra-no-oriente-medio-derruba-exportacoes-

de-madeira-do-brasil-e-eleva-custos-no-setor-florestal

Cipem and IDB develop strategy to expand exports

The Center of Timber Producers and Exporters of Mato

Grosso State (Cipem) has launched a new strategy to

expand exports of the forest sector in partnership with the

Inter-American Development Bank (IDB).

The initiative is part of the Export Culture Promotion Plan,

coordinated by the Ministry of Development, Industry,

Trade and Services (MDIC), with a focus on increasing

competitiveness, economic diversification and the

sustainable promotion of Brazilian exports.

During a meeting with the IDB, Cipem presented an

overview of the state’s forest sector, highlighting its

productive potential, product diversity and the main

bottlenecks limiting access to international markets. The

institution emphasised that the main objective is to

structure development policies and trade promotion

measures without changing the current environmental

legislation.As a first step, a survey will be conducted

among member companies to identify their profile, interest

in exporting and the main sector challenges.

The information will be collected by the unions affiliated

with Cipem and consolidated to support future strategic

actions.

An export promotion policy will be based on strategic

pillars such as institutional coordination, business

promotion, strengthening the sector’s image and financing

mechanisms.

Cipem also highlighted Brazil’s strong growth potential in

the global forest products market, emphasising sustainable

forest management as a key competitive advantage of

production in Mato Grosso.

See: https://cipem.org.br/cipem-sela-parceria-com-bid-para-

ampliar-exportacoes/

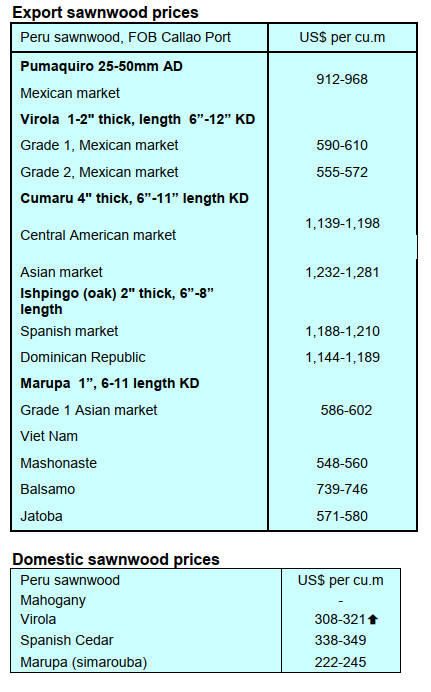

9. PERU

February exports of semi-finished products

encouraging

According to information provided by the Services and

Extractive Industries Management of the Association of

Exporters (ADEX) in February, exports of semi-finished

products reached a value of US$5.4 million FOB,

representing a growth of over four times that in the same

period of 2025.

France was the main export destination accounting for

49% of the total for this product group share. The value of

exports to France was over six times that in the same

period in 2025. Belgium ranked second with a 16% share,

showing a positive growth four times that compared to the

same period of the previous year. Denmark ranked third

with a 7% share, registering a positive percentage change

eight times that in the same period in 2025.

SERFOR - new forest fire detection and response plan

Within the framework of the 2025–2027 Multi-sectoral

Plan for Forest Fires, the National Forest and Wildlife

Service (SERFOR) has strengthened monitoring, early

detection and response to forest fires by optimising its

SERFOR Forest Fire Alert platform which operates

throughout the country.

Through an updated network of contacts, SERFOR

coordinates directly with regional and local governments

to verify alerts in the field. This mechanism has increased

fire confirmation by 70%, allowing for better resource use

and improved planning of response and restoration

actions.

With this initiative the Agency reaffirms its commitment

to using technology to improve prevention, strengthening

environmental safety and enabling timely responses to

forest fires in Peru.

See: https://www.gob.pe/institucion/serfor/noticias/1388745-

serfor-optimiza-la-deteccion-y-respuesta-ante-incendios-

forestales-con-plataforma-de-monitoreo-a-nivel-nacional

OSINFOR to Monitor 337,000 ha.of forests in 2026

With the goal of promoting the sustainable use of forest

resources in the Amazon the Supervisory Agency for

Forest Resources and Wildlife (OSINFOR) has scheduled

134 monitoring operations in 2026 in areas with

authorised permits located in the Department of Loreto.

These actions aim to cover 337,193 hectares of forest

where the State has authorised the harvesting through

permits. According to OSINFOR's 2026 Annual

Monitoring Plan and Five-Year Evaluation Program, 48

monitoring operations will be carried out in forestry

permits granted to indigenous communities, 54 on private

properties, 11 on timber concessions and five on

conservation concessions.

See: https://www.gob.pe/institucion/osinfor/noticias/1390351-

loreto-el-osinfor-supervisara-mas-de-337-000-hectareas-de-

bosques-en-2026

Peru's forest economy is built on massive Amazonian

resources, the second largest in South America, yet it

remains underutilised, contributing less than 1% to GDP.

While harbouring high biodiversity and timber potential,

the sector is heavily plagued by informality, with roughly

75% of timber harvested informally and high rates of

deforestation driven by agriculture, illegal mining and

illegal logging.

See: chrome-

extension://efaidnbmnnnibpcajpcglclefindmkaj/https://www.idos

-research.de/uploads/media/GGGI-

DIE_Fact_Sheet_Estimating_the_Ecomomic_Value_of_Peru__s

_Forest_Sector_-_Beyond_Conventional_Wisdom.pdf

|