US Dollar Exchange Rates of

25th

May

2026

China Yuan 6.77

Report from China

Decline in China’s sawnwood imports

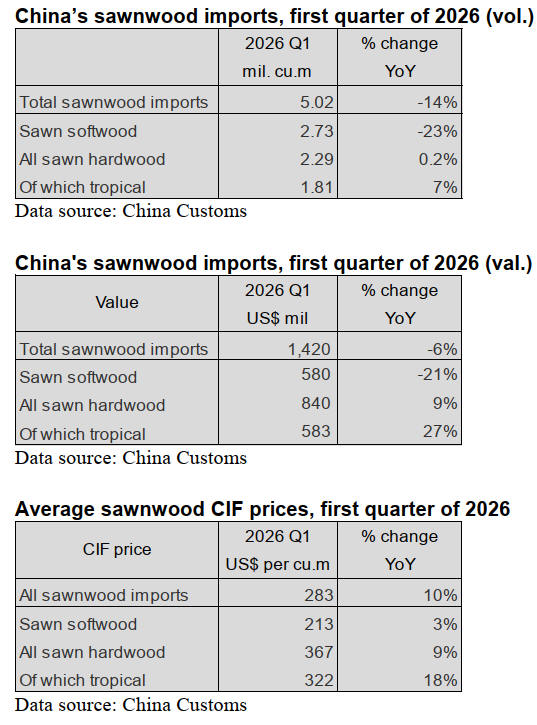

According to China Customs, China’s sawnwood imports

in the first quarter of 2026 totalled 5.02 million cubic

metres valued at US$1.42 billion, down 14% in volume

and 6% in value compared to the first quarter of 2025.

The average price for imported sawnwood was US$283

CIF per cubic metre, up 10% over the same period of

2025.

Of total sawnwood imports, sawn softwood imports

dropped 23% to 2.73 million cubic metres and accounted

for 54% of the national total. The average price for

imported sawn softwood rose 3% to US$213 CIF per

cubic metre over the same period of 2025.

Sawn hardwood imports rose just 0.2% to 2.29 million

cubic metres and accounted for 46% of the national total.

The average price for imported sawn hardwood increased

9% to US$367 CIF per cubic metre over the same period

of 2025.

Of total sawn hardwood imports, imports of sawnwood

from tropical countries were 1.81 million cubic metres

valued at US$583 million CIF, up 7% in volume and 27%

in value from the same period of 2025 and accounted for

36% of the national total import volume. The average

price for imported tropical sawnwood was US$322 CIF

per cubic metre, up 18% from the same period of 2025.

China's imports of sawnwood decreased by 14% year-on-

year to 5.02 million cubic metres in the first quarter of

2026. The main reasons for the decline were the continued

sluggishness in new housing construction which

suppressed the demand for construction-grade sawn

softwood coupled with the contraction of Russian as well

as a short-term decline due to the Spring Festival holidays.

Weak demand for real estate

The import volume of construction sawnwood, especially

sawn softwoods like fir, spruce and scots pine which

account for nearly 50% of the total imports, dropped

significantly dragging down total import volumes.

Russian supply contraction

Russian imports have dropped by almost 30% year-on-

year, with the share of total imports decreasing from 47%

to 39%. Russian exports to China have been affected by

the geopolitical strategy shift to Central Asia/Middle East

and the cautious purchasing approach in China.

Spring Festival and seasonal factors:

The volume of China’s sawnwood imports in February

2026 dropped by 25% year-on-year. Although it partially

recovered after the Spring Festival with the decline

narrowing to 16% in March 2026, the overall quarterly

volume still contracted significantly.

Optimisation of import structure

High value-added sawn hardwood species such as ash and

North American hardwoods have experienced some

growth but their share was insufficient to offset the

declining overall trend of sawnwood imports. At the same

time, some sawnwood originally sourced from the United

States and Canada is arriving in China via Viet Nam

reflecting a supply chain restructuring rather than a

decline.

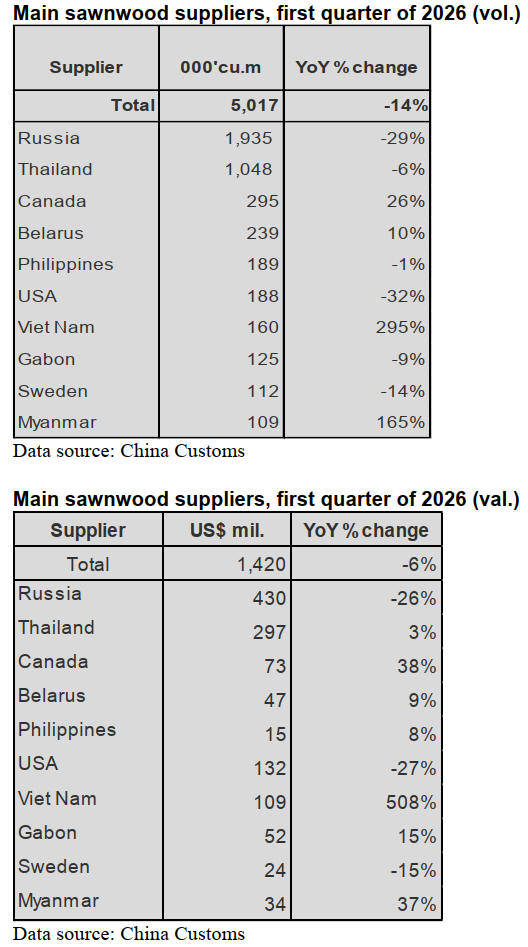

Decline in sawnwood imports from Russia

China’s sawnwood imports from Russia and Thailand fell

29% and 6% to 1.935 million cubic metres and 1.048

million cubic metres respectively in the first quarter of

2026. The decrease in sawnwood imports from the two top

countries directly resulted in the significant decline of the

total sawnwood imports in the first quarter of 2026.

Russia still was the largest suppliers of China’s sawnwood

imports in the first quarter of 2026. The proportion of

China’s sawnwood imports from Russia accounted for

39% of the total sawnwood imports volume, down 7

percentage points over the same period of 2025.

Thailand was the second largest supplier of China’s

sawnwood imports in the first quarter of 2026. The

proportion of China’s sawnwood imports from Thailand

accounted for 21% of the total sawnwood imports volume,

up 2 percentage points over the same period of 2025.

China’s sawnwood imports from the two top countries,

Russia and Thailand, accounted for 60% of the national

total in the first quarter of 2026.

China’s imported

sawnwood species from Russia were

spruce and fir, Korean pine and Mongolian scots pine,

birch, oak, ash, poplar and maple dropped 32%, 29%,

17%, 26%, 24, 59% and 3% respectively in the first

quarter of 2026.

It is worth noting that China's sawnwood imports from

Viet Nam and Myanmar increased by 295% and 165%

respectively in the first quarter of 2026.

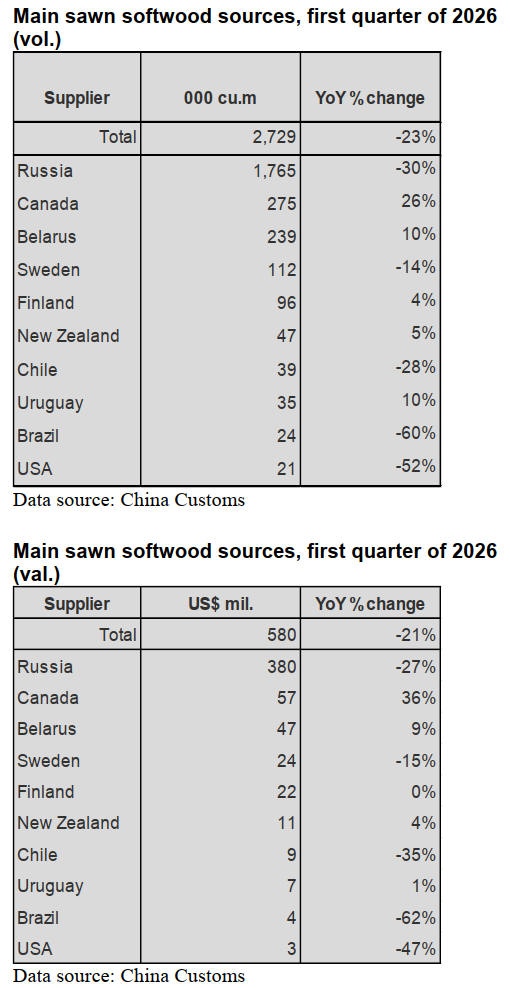

Main sawn softwood sources, first quarter of 2026

Russia was the largest supplier for China’s sawn softwood

imports. 65% of China’s sawn softwood is imported from

Russia but imports from Russia fell 30% to 1.765 million

cubic metres in the first quarter of 2026.

In addition, China’s sawn softwood imports from Sweden,

Chile, Brazil and USA decreased 28%, 60% and 52%

respectively in the first quarter of 2026.

In contrast, China’s sawn softwood imports from Canada,

Belarus, Finland, New Zealand and Uruguay rose 26%,

10%, 4%, 5% and 10% respectively in the first quarter of

2026.

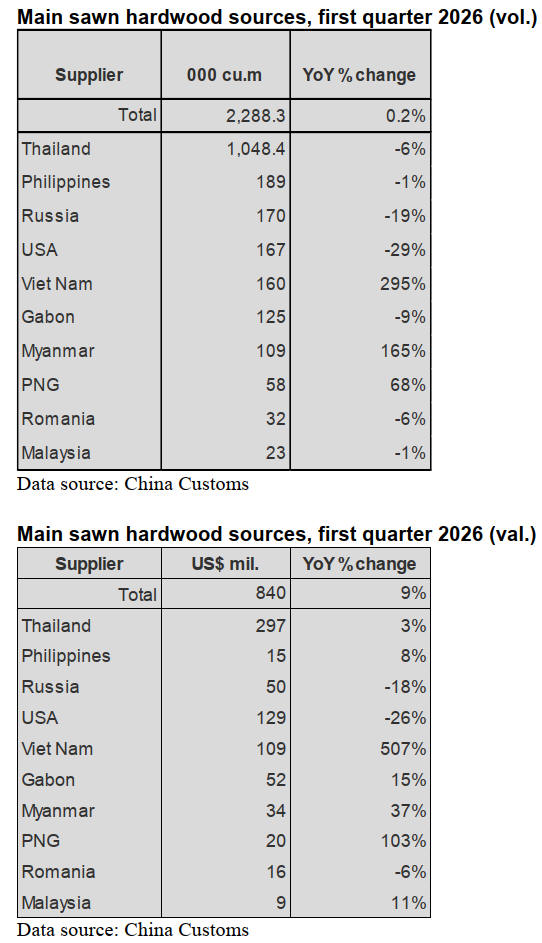

Surge in sawn hardwood imports from Viet Nam

According to China Customs, China’s sawn hardwood

imports from Viet Nam surged 295% to 160,000 cubic

metres in the first quarter of 2026. In addition, China’s

sawn hardwood imports from Myanmar surged 165% to

109,000 cubic metres in the first quarter of 2026.

Thailand was the largest supplier of China’s sawn

hardwood imports. 46% of China’s sawn hardwood

imports are imported from Thailand. China’s sawn

hardwood imports from Thailand fell 6% to 1.048 million

cubic metres in the first quarter of 2026.

In addition, China’s sawn hardwood imports from the

Philippines, Russia, USA, Gabon, Romania and Malaysia

dropped 1%, 19%, 29%, 9%, 6% and 1% respectively in

the first quarter of 2026.

In contrast, China’s sawn hardwood imports from PNG

grew 68% in the first quarter of 2026.

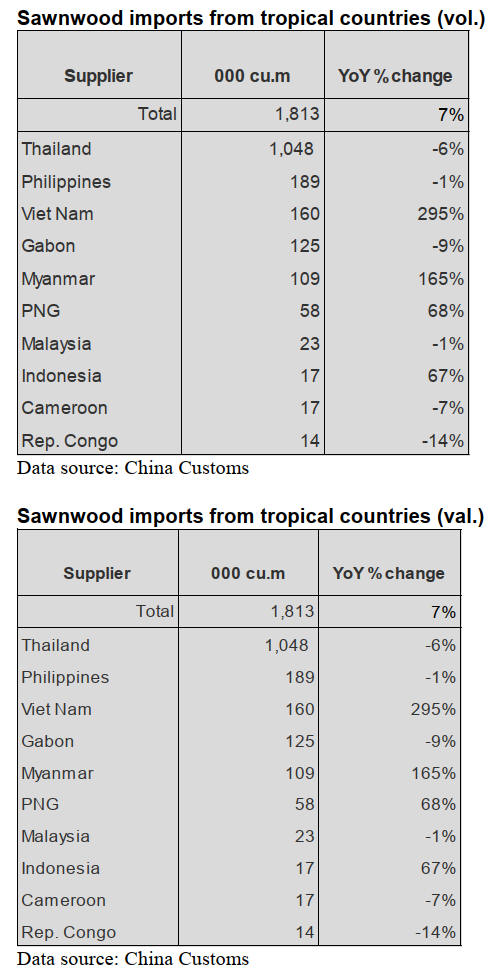

Rise in sawnwood imports from tropical countries

China’s sawnwood imports from tropical countries rose

7% to 1.813 million cubic metres in the first quarter of

2026. The top three tropical suppliers of China’s

hardwood sawnwood imports were Thailand (58%), the

Philippines (10%) and Viet Nam (15%). 84% of China’s

tropical sawnwood imports were from these three

countries in the first quarter of 2026.

China’s sawnwood imports from Viet Nam surged 295%

in the first quarter of 2026, which directly resulted in the

increase of the national total tropical sawnwood imports in

the first quarter of 2026.

China imported ash, oak and other North America

hhardwoods from Viet Nam. China also imported some

cherry, Chinese redwood, maple, poplar and beech

sawnwood for the first time in the first quarter of 2026.

It worth noting that China’s tropical sawnwood imports

from Myanmar, PNG and Indonesia also rose 165%, 68%

and 67% respectively in the first quarter of 2026.

The main reason for the significant increase in China's

imports of tropical sawnwood from Myanmar was the

large volume of imported teak sawnwood. In contrast,

China’s tropical sawnwood imports from Thailand, the

Philippines, Gabon, Malaysia, Cameroon and the Republic

of Congo dropped 6%, 1%, 9%, 1%, 7% and 14%

respectively in the first quarter of 2026.

April GGSC report

Customs data show that in the first quarter of 2026,

China’s total log imports reached 7.164 million cubic

metres, down 11% year-on-year, while the average import

price edged down 3% from the same period last year.

Sawnwood imports totaled 5.017 million cubic metres, a

decrease of 14% year-on-year, though the average price

rose almost 10%.

Entering the second quarter, infrastructure and housing

construction projects across various regions had resumed

intensive work and coupled with the execution of

previously accumulated orders the timber market was

showing signs of a pickup.

Recently, many Chinese

provinces released their lists of

key provincial-level projects for 2026, with the number of

timber industry-related projects reaching an all-time high

which may inject new momentum into the industry.

Looking ahead to the full year, a report jointly released on

April 29 by the Chinese Academy of Social Sciences and

the Social Sciences Academic Press projects that China’s

national land greening targets will be largely met in 2026.

The report also forecasts that the country’s forest product

exports may see stability, while wood product prices are

expected to rise.

In April 2026, the GTI-China index registered 53.5%, a

decrease of 7.6 percentage points from the previous month

and above the critical value (50%) for two consecutive

months, indicating that the business prosperity of the

timber enterprises represented by the GTI-China index

expanded from the previous month.

Regarding the twelve sub-indexes, ten indices (production,

new orders, export orders, existing orders, inventory of

finished products, purchase quantity, purchase price,

employees, delivery time and market expectation) were

above the 50% critical value while the remaining two

indices (imports and inventory of main raw materials)

were below the critical value. Compared to the previous

month, all the 12 sub-indices decreased with declines

ranging from 2.2 to 11.0 percentage points.

See: chrome-

extension://efaidnbmnnnibpcajpcglclefindmkaj/https://www.itto-

ggsc.org/static/upload/file/20260515/1778810654194472.pdf

|