US Dollar Exchange Rates of

10th

June

2026

China Yuan 6.78

Report from China

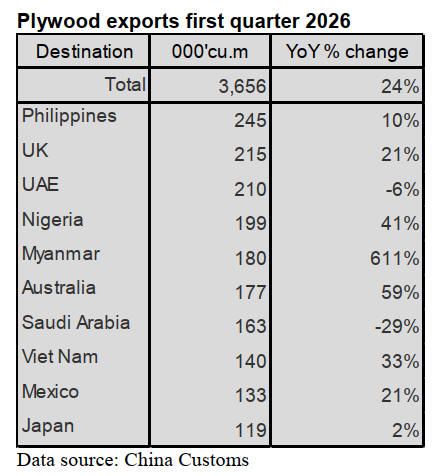

Plywood exports increased in the first quarter

According to China Customs, plywood exports in the first

quarter of 2026 totalled 3.656 million cubic metres, up

24% over the same period of 2025.

The Philippines and the UK were the first and second

largest destinations for China’s plywood exports. China’s

plywood exports to these two countries rose 10% and 21%

respectively in the first quarter of 2026.

China’s plywood exports to the third largest destination

country, the UAE, declined 6% in the first quarter of 2026.

The countries and regions for China’s plywood exports are

numerous and the proportion of China’s plywood exports

to the top 10 destination countries in the first quarter of

2026 accounted for just 50% of the national total in the

first quarter of 2026.

China’s plywood exports to Nigeria, Australia, Viet Nam

and Japan grew 41%, 59%, 33% and 2% in the first

quarter of 2026.

In contrast, the volume of China’s plywood exports to

Saudi Arabia fell 29% among the top destination countries

in the first quarter of 2026.

The key factors behind the rise in exports were the price

advantage, the shift in demand and support from

government policies and the high production capacity.

Indonesia's plywood exports plummeted to 622,000 cubic

metres, down 26% year-on-year in the first quarter of

2026, with exports to the US dropping by 60%, resulting

in the loss of market share in the United States, the Middle

East and Southeast Asia.

The average price of China’s plywood exports in the first

quarter was US$$343 per cubic metre, a year-on-year

decrease of 6%, which is approximately 40% lower than

that in Indonesia. Given the scale of production and

automation of the processes there was a strong capacity for

rapid delivery, high container loading rate and low

logistics costs.

The production capacity in China is large and the sector

benefits from the Regional Comprehensive Economic

Partnership (RCEP) and export tax rebates.

. Cluster production of plywood in Shandong Province and

Guangxi Zhuang Autonomous Region. has been expanded

and the supply of fast-growing timber such as eucalyptus

is stable.

The RCEP origin verification process has been accelerated

and export tax rebates are stable and subsidies for non-

formaldehyde glue support product upgrades are provided.

The proportion of E0/ENF grade formaldehyde-free

plywood has increased meeting the formaldehyde

emission requirements in Europe and the United States.

Surge in plywood exports to Myanmar

According to China Customs, plywood exports to

Myanmar surged over 600% in the first quarter of 2026.

This was the result of a combination of four factors,

China's production capacity advantage, the domestic

supply-demand gap in Myanmar, the convenient

geographical logistics and bilateral trade policies. This

growth of exports is expected to continue throughout the

year since China has become the main source for

Myanmar's plywood imports.

The total volume of wood panel trade along the China-

Myanmar border has seen a significant increase and

plywood has become the core growth driver of the export

trade.

The main reasons for the surging China’s plywood exports

to Myanmar are said to be:

The Chinese plywood industry is mature and of a large-

scale production with a high degree of automation. It has

the capacity to supply plywood products of various

specifications and grades fully meeting the diverse

demands of Myanmar.

Chinese plywood has a significant advantage in terms of

cost performance. Compared with locally produced

plywood in Myanmar and imported plywood from other

Southeast Asian countries, it has extremely strong price

competitiveness.

The product range is comprehensive covering both

ordinary building materials and specialised plywood for

furniture production. Chinese products are fully available

and of stable quality enabling precise alignment with

various purchasing demands in the Myanmar market.

Reduced costs and enhanced efficiency in logistics

delivers export advantages.

Because direct

transportation via multiple border crossings

between China and Myanmar is possible there is no need

for ocean shipping. The transportation route is short and

highly flexible. The charges for plywood shipped to

Myanmar is 30% to 40% cheaper than to other ASEAN

destinations and delivery times are only 7-10 days.

The China-Myanmar Economic Corridor continues to

make steady progress. The Customs clearance procedures

at the border have been simplified and the inspection

efficiency has been enhanced. The widespread use of

direct RMB cross-border settlement has effectively

reduced exchange rate losses and trade handling costs,

significantly improving the efficiency of China's exports.

The gap between supply and demand of plywood in

Myanmar continues to widen.

The industrial

foundation in Myanmar is weak and there is

no capacity for large-scale processing of plywood.

Domestic production of plywood in Myanmar is of limited

variety which cannot meet the demands in the domestic

market.

In the first quarter of 2026, the infrastructure construction,

furniture manufacturing and house renovation sectors in

Myanmar experienced a rapid recovery. The demand for

building materials was high further widening the gap

between local production capacity and demand. Many

sectors are highly dependent on imported building

materials.

Due to sanctions imposed by Europe and the United States

and the restricted foreign trade channels, Myanmar has

difficulty importing high-quality and cost-effective

building materials from Europe and the United States as

well as from Southeast Asian countries. Therefore,

Chinese building materials such as plywood have become

the preferred alternative category for its imports.

The bilateral trade environment continues to be favorable

for exports. China and Myanmar have been continuously

implementing preferential policies for the border trade.

Plywood exporters enjoy Customs clearance convenience

and tax and fee reductions which significantly lowers the

plywood export costs for Chinese enterprises to Myanmar.

Myanmar will reportedly relax restrictions on the import

of building materials, lower tariffs on wood panels and

simplify the import registration process. This will be

beneficial for large-scale imports of plywood from China

into the Myanmar market.The pattern of processing and

border trade cooperation zone along the China-Myanmar

border has matured.

Relying on the synergy of border industries, the system for

plywood transfer, packaging and local distribution is well-

established, further facilitating the large-scale export of

Chinese plywood to various markets in Myanmar.

China's advantage in plywood production capacity, the

strong demand gap in Myanmar, the geographical logistics

benefits and the favorable policies will continue. The high

growth trend of China's plywood exports to Myanmar will

also continue and the bilateral plywood trade volume is

expected to further expand.

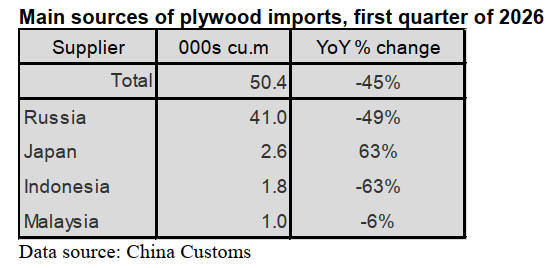

Decline in plywood imports from Russia

Russia still is the largest supplier of China’s plywood

imports accounting for 82% of the national total plywood

imports however, in the first quarter of 2026, China’s

plywood imports from Russia dropped 49% over the same

period of 2025 directly resulting in the large decline of the

national plywood imports in the first quarter of 2026.

In the first quarter of 2026, import volumes of plywood in

China dropped significantly. The main reason was the

combined effect of four factors, namely the collapse of

domestic demand, the strengthening of domestic

substitution, the increase in international costs and trade

and seasonal disturbances.

In the first quarter the area of new construction started was

down by 203% year-on-year and the area of completed

construction was down by 25%. The demand for

buildings, decoration materials and furniture also shrank.

The output of wooden furniture only increased by 0.15%,

export orders weakened, manufacturers reduced

production and inventory and they reduced imports.

Factories were shut down in February 2026 during Spring

Festival. The timber trade volume in that month decreased

by 31% compared with the previous month, dragging

down the overall imports in the first quarter of 2026.

Domestic substitution accelerated and import demand was

squeezed. High-yield planted forests of fast-growing

species such as poplar and eucalyptus have reached the

peak of rotation period.

New production lines have been added in regions like

Shandong province and Guangxi Zhuang Autonomous

Region. The middle and low-end plywood markets are

basically self-sufficient, reducing reliance on imports from

Southeast Asia and Russia.

The increase in international supply and landed prices

have led to a decline in the cost-effectiveness of imports.

Major producing countries such as Indonesia and Malaysia

raised plywood prices and experienced reduced production

during the rainy season, leading to an increase in export

prices. Russia supplies were affected by the strengthening

ruble and rising energy costs and thus saw a year-on-year

decrease of 49% in its exports of plywood to China.

The tense situation in the Strait of Hormuz led to some

routes changing to the Cape of Good Hope, causing freight

rates to rise by 30%-50%, further pushing up the landed

prices.

Exchange rate fluctuations. The depreciation of the RMB

against the US dollar has led to an increase in import

costs, weakening plywood purchasing.

Trade barriers and policy disturbances have impacted

exports. The spillover effect of high tariffs in the United

States through the 267% comprehensive tariff on Chinese

plywood forces domestic production capacity to shift

towards domestic sales, thereby squeezing out import

space.

Higher quarantine standards have led to difficulties in the

clearance of some low-quality plywood from Southeast

Asia due to issues such as formaldehyde and insect

damage, resulting in restricted plywood import volumes.

In the first quarter of 2026 China’s plywood imports

totalled 50,000 cubic metres, down 45% over the same

period of 2025.

Malaysia and Indonesia used to be the main suppliers of

plywood to China in the past, but China’s plywood

imports from Indonesia and Malaysia declined 63% and

6% respectively in the first quarter of 2026 their status in

China further decline.

In contrast, China’s plywood imports from Japan rose

63%.

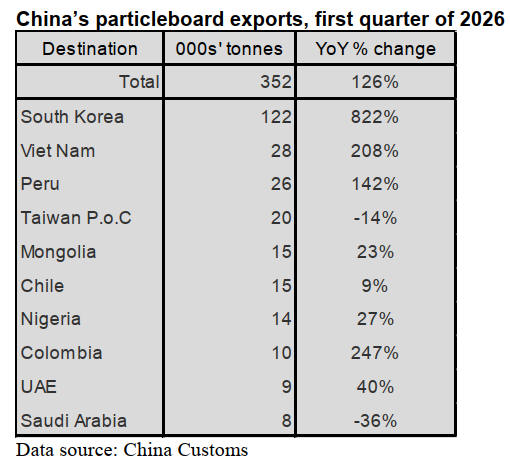

Surge in particleboard exports

According to China Customs, particleboard exports in the

first quarter of 2026 totalled 352,000 tonnes valued at

US$110 million, surging 126% in volume and 40% in

value over the same period of 2025.

China’s particleboard exports to the top three destinations,

namely South Korea, Viet Nam and Peru surged over

800%, 200% and 140% respectively over the same period

of 2025. In addition, China’s particleboard exports to

Colombia also surged over 240% in the first quarter of

2026.

Taiwan P.o.C was the fourth largest destination for

China’s particleboard exports in the first quarter of 2026

but down 14% over the same period of 2025. China’s

particleboard exports to Saudi Arabia fell 36% in the first

quarter of 2026.

The main reasons for the significant increase in China's

particleboard exports are as follows.

Expansion of ASEAN furniture assembly businesses and

the furniture production capacity in Viet Nam and

Indonesia has significantly increased. There is a shortage

of flooring materials in the Chinese domestic market so

emergency replenishment of Chinese ENF grade

formaldehyde-free particleboard has been implemented in

the first quarter of 2026.

California and other regions in the US have implemented

mandatory standards for formaldehyde-free particleboard.

Chinese E0/ENF grade particleboard products have

replaced the production capacity gaps in Europe and North

America.

Realisation of RCEP tariff benefits. The agreement tariffs

on particleboard were further reduced in the first quarter of

2026 along with the optimisation of the rules of origin.

The particleboard export costs to ASEAN and the Middle

East have significantly declined.

There has been a significant improvement in the

competitiveness of domestic particleboard industries

especially in terms of environmental protection and

compliance. The proportion of E0/ENF grade

particleboard products exceeds 52% and formaldehyde-

free particleboard has become mainstream.

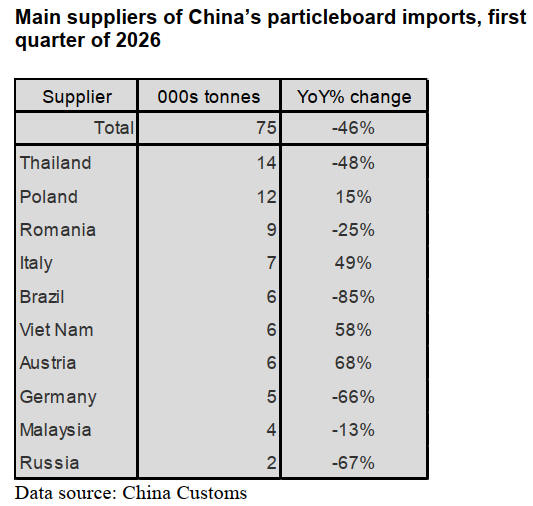

Significant decline in particleboard imports from

Thailand

According to China Customs, particleboard imports from

Thailand dropped 48% in the first quarter of 2026.

Thailand was the largest supplier for China’s particleboard

imports so that China's overall imports of particleboard

sharply declined in the first quarter of 2026. China’s

particleboard imports in the first quarter of 2026 totalled

75,000 tonnes, down 46% over the same period of 2025.

In the first quarter of 2026, China's imports of

particleboard from Thailand sharply decreased. The main

reason for the decrease in imports from Thailand are said

to be.

Chinese particleboard capacity has expanded. New

particleboard production capacity will exceed 12 million

cubic metres by the end of 2026 with ENF grade

formaldehyde-free particleboard accounting for 52% or

more.

The cost of Chinese ENF grade particleboard is from

US$220 to US$240 per cubic metre, while the cost of

particleboard imported from Thailand is around US$280

per cubic metre. The cost of European particleboard is

even higher such that the cost advantage of China’s

particleboard is overwhelming.

Leading custom furniture enterprises such as OPPEIN and

Suofeiya have reduced import purchases and prioritised

domestic F4-star/ENF grade particleboard. The import

dependency of particleboard has dropped to 9%.

In the first quarter of 2026, the completed area of

residential buildings in China decreased by 26% year-on-

year. The construction of finished houses slowed down,

and the demand for high-end imported decorative panels

declined.

Weakness in furniture and home decoration sector remains

a factor. Consumption of particleboard has been weak and

enterprises have been reducing inventory and controlling

costs. Further, the willingness to purchase high-priced

imported particleboard dropped significantly.

|