|

1.

CENTRAL AND WEST AFRICA

Modest price increases observed

FOB prices throughout the region have begun to trend

slightly higher as producers try to pass on some of the

increased operating costs including increased taxation,

rising fuel prices and higher logistics expenses. While the

increases remain relatively limited producers are under

pressure to recover additional costs throughout the supply

chain.

One of the most positive developments recently has been

the return of Chinese buying activity. Demand for both

Okoumé and various redwood species has improved

bringing new orders to producers in Gabon, Cameroon and

Congo.

This renewed demand has helped stabilise the market and

is supporting the recent firming of prices. While increased

demand remains moderate the overall market sentiment is

firmer than earlier in the year.

Industries in the region are beginning to shift production

into the traditional summer holidays mode. There is

always reduced business activity during July, August and

to some extent, September. Buyers in Europe and North

America are expected to remain cautious and carefully

manage landed stocks as the annual vacation period

approaches.

Weather conditions across the region

Weather conditions remain mixed. Gabon has entered its

dry season with comfortable temperatures between 26°C

and 28°C while Cameroon continues to experience heavy

rainfall. Northern Congo remains wet, while Southern

Congo has entered a drier period. The Central African

Republic continues to experience seasonal rains. These

weather patterns continue to influence harvesting

operations, road conditions and timber transportation.

Freight rates continue to move higher

Shipping rates from Cameroon, Congo and Gabon to

Antwerp have reportedly increased by approximately €20

per cubic metre, particularly on services operated by major

European shipping lines. Other carriers are also

experiencing cost pressures, resulting in additional upward

pressure on logistics costs. Container freight charges to

China and the Middle East have also recorded slight

increases.

Middle East - outlook remains uncertain

The timber trade to the Middle East remains stable but

cautious. Market participants are closely monitoring

geopolitical developments in the region. There is optimism

that improved stability around the Gulf region and the

Strait of Hormuz could support renewed construction

activity and stimulate timber demand from Iraq, Iran and

neighbouring countries. Any increase in regional building

activity would likely provide additional opportunities for

African hardwood exports.

The overall market remains relatively quiet but stable.

The return of Chinese demand is providing important

support for producers while modest price increases are

helping partially offset higher production and transport

costs. Prospects for the coming months will largely depend

on post-summer demand in Europe, continued Chinese

purchasing activity and developments in Middle Eastern

markets. If these factors remain favourable the sector

could see a gradual improvement during the second half of

2026.

Gabon

Gabon has now entered the dry season, with temperatures

ranging between 26°C and 28°C and virtually no rainfall

in the interior regions. Improved weather conditions are

supporting harvesting operations and transport logistics

with activity expected to remain favourable through

September.

China has returned to the market with renewed demand for

Okoumé and selected hardwood species, providing an

important boost to producers and processors across the

country.

Production levels are gradually increasing as market

demand improves. Key harvested species remain Okoumé,

Okan, Azobé and various redwood species.

Azobé supply remains tight

It has been reported that Azobé log supplies remains

critically low due to the lingering impact of poor forest

road conditions following previous rainy seasons. Some

concessions in the Okondja region have reportedly been

attempting to move logs to mills for more than five

months.

As a result, buyers are increasingly evaluating substitute

species such as Okan, Mukulungu and Obonga. The

willingness of European end-users, particularly in the

Dutch market, to adopt alternative species remains an

important factor for future trade flows.

Domestic market demand firm

The domestic market continues to show stable demand.

Sawn Okoumé is currently selling at approximately

FCFA150,000–160,000 per cubic metre in local markets

while Dabema is trading between FCFA180,000 and

200,000 per cubic metre.

Transport and Infrastructure

Road conditions have improved significantly with the

arrival of the dry season and ongoing maintenance works.

Transport times from the eastern and southern production

regions to Owendo Port have been reduced to

approximately two days under normal conditions. Laterite

roads are undergoing repairs, improving access from key

timber-producing areas such as Makokou and Okondja.

Gabon continues to pursue ambitious infrastructure

projects linked to the mining sector. Studies are underway

for a second railway corridor connecting the Belinga iron

ore project to the future deep-water ports of Kobe-Kobe

and Mayumba.

The proposed development would include approximately

600 kilometres of railway and 550 kilometres of road

infrastructure. According to project representatives, first

exports through the future Kobe-Kobe port are targeted for

April 2029.

Despite these plans, funding remains a challenge. Several

infrastructure projects continue to face delays due to

limited financing.

Power and water supply critical challenges

Power supply remains one of Gabon's most significant

operational challenges. Electricity outages continue daily

with two to three interruptions lasting several hours each.

The national utility company, SEEG, acknowledges that

the electricity network is outdated. Discussions continue

with French utility specialist Suez although no tangible

improvements have yet been observed.

Water shortages remain equally problematic. Many

households and businesses rely on water collection points,

storage tanks or private boreholes.

Demand and export trends

European demand remains relatively subdued although

some improvement has been reported as inventories

continue to be consumed. Azobé exports to the

Netherlands remain steady at approximately 1,500–2,000

cu.m per month. Emerging demand continues from

Bangladesh and Pakistan for both Azobé and Okan.

Chinese demand remains selective but continues to

support exports of Okoumé and specialty products.

Interest in Azobé table tops remains particularly strong

with reported FOB prices around €680 per cubic metre.

Port operations at Owendo remain stable, with no

significant disruptions reported. Container availability

remains adequate and transport between production areas

and port facilities is functioning normally.

Regulatory environment

CITES-listed species, including Padouk, Khaya, Doussié

and Kevazingo, continue to face tighter regulatory

controls. However, permit processing times in Europe

have reportedly improved, with approvals now generally

taking no longer than two weeks.

The supposed proposed future expansion of CITES listings

remains a concern for producers throughout the region and

continues to be closely monitored.

Tax increases to affect competitiveness

The export duty increases introduced on 1 January 2026

remain a major challenge for Gabon's timber industry.

These charges have increased costs and placed Gabonese

exporters at a disadvantage relative to neighbouring

countries. In response to the new duty rates, prices for

most major sawn timber species have risen by

approximately €20 per cubic metre, with costs being

shared between producers and buyers where possible.

AGOA reinstatement opens opportunities

A positive development for Gabon was the restoration of

eligibility under the African Growth and Opportunity Act

(AGOA). After previously being excluded, Gabon has

once again been included among the participating African

countries benefiting from preferential access to the U.S.

market.

Some observers view the decision as part of broader

geopolitical efforts by the United States to maintain

economic influence in Africa amid growing Chinese

involvement across the continent.

Outlook

The overall market outlook is cautiously positive. Dry-

season conditions are supporting production and transport,

while renewed Chinese demand is helping stabilise orders

and prices. However, electricity shortages, infrastructure

constraints, tax increases and regulatory pressures

continue to weigh on the sector.

The key themes to watch during the second half of 2026

remain Chinese demand, the development of major

infrastructure projects, the evolution of CITES regulations

and the industry's ability to adapt to tighter fiscal and

environmental requirements.

Cameroon

Cameroon has entered its main rainy season which is

expected to continue from late June through early

December. As a result, harvesting activity has begun to

slow, particularly in areas where weather conditions are

affecting access and transportation.

Trucking operations continue under generally normal

conditions although some laterite roads are being closed

once again during periods of heavy rainfall. Rail transport

remains operational without major disruption.

An important recent development is the rehabilitation of

the road linking northern Congo to Sangmelima. This

route is strategically important for forestry operators in

northern Congo who use it to transport to the Port of Kribi.

Containerised timber shipments are increasingly routed

through Kribi while conventional sawn timber and logs

continue to move through the Port of Douala.

Plans are progressing for the expansion of Kribi Port,

including the development of additional log storage areas

and sawn timber facilities to reduce pressure on Douala's

increasingly congested operations.

County by country demand remains mixed

Middle East demand for redwood species remains stable.

Ayous demand remains weak in Italy and the Netherlands.

Demand in the Philippines remains subdued. Viet Nam

continues to show strong demand for species such as Tali

and other hardwoods. European demand remains slow,

particularly for Padouk.

Government inspections and increased controls by forestry

and finance authorities continue to influence production

decisions and operational planning.

Several mills have ceased operations or relocated outside

the Douala area, while many remaining sawmills are

operating on a single-shift basis with forward order books

of only around one to two months.

A notable regulatory feature remains the government's

quota system for log exports. Export allocations are linked

to each company's sawn timber production performance,

tax compliance and adherence to forestry regulations.

While intended to encourage domestic processing many

operators view the system as complex and inconsistent

with allocations varying significantly between companies.

Operators continue to face permit requirements for

CITES-listed species, but processing times have improved

considerably. Both Cameroon and European authorities

are now generally issuing CITES approvals within

approximately two weeks, reducing one of the major

bottlenecks previously affecting international trade.

Outlook

The combination of seasonal rains and cautious

international demand is likely to limit production growth

during the coming months. However, improving Chinese

demand, stable Middle Eastern markets and efficient

transport links through both Douala and Kribi continue to

provide support for the sector.

Republic of the Congo

Weather conditions remain mixed across the Republic of

the Congo. Northern regions have returned to rainy-season

conditions while southern areas have entered a drier period

that is expected to continue for several months.

These differing weather patterns continue to influence

harvesting and transport operations across the country,

with northern concessions facing more challenging

operating conditions than those in the south.

Transport infrastructure remains generally functional.

Maintenance and repairs continue on key laterite road

networks, helping to maintain access to production areas

despite seasonal weather conditions. Northern operators

continue to utilise transport corridors through Cameroon,

including routes to Douala and Kribi ports, while southern

producers remain focused on Pointe-Noire.

The Port of Pointe-Noire continues to operate normally

and remains one of Central Africa’s most important deep-

water ports. The port functions as a major logistics hub for

regional exports and continues to support Congo’s timber

sector efficiently. Development and expansion projects

remain under consideration as authorities seek to

strengthen the port's regional role and accommodate future

trade growth.

No significant disruptions to port operations or cargo

handling were reported during the period.

Log inventories at sawmills are said to be adequate with

operators generally holding two to three months of stock.

Northern Congo continues to be dominated by species

such as Sapelli, Sipo and other redwood species which

remain important export products for both European and

Asian markets.

Forestry administration remains strict

The forestry administration continues to maintain a strong

reputation for oversight and control of forest operations

and exports. No major regulatory changes were reported

during the period, although compliance requirements

remain closely monitored by authorities. Export

documentation and operational controls continue to be

enforced rigorously.

Outlook

The outlook for the second half of 2026 remains

cautiously positive. Stable operations, adequate timber

stocks, efficient port infrastructure and continued demand

from Asian markets provide support for the sector.

Key issues include seasonal weather conditions in northern

production areas, evolving international demand, potential

developments in carbon-credit programmes and future

regulatory discussions concerning individual species.

Through the eyes of industry

The latest GTI report lists the challenges identified by the

private sector in the Republic of Congo and Gabon.

See: https://www.itto-

ggsc.org/static/upload/file/20260615/1781506386105682.pdf

2.

GHANA

AGI partners Danish industries to enhance

sustainability principles

The Association of Ghana Industries (AGI), in partnership

with the Confederation of Danish Industries, has launched

a ‘Sustainable African Value Chain Initiative’ (SAVI).

This aims to build business capacity to embed

sustainability principles across operations and value chains

through capacity building, technical assistance, peer

learning, stakeholder engagement and implementation

support.

Speaking at the launch, AGI President Dr. Kofi Nsiah-

Poku said, SAVI will help firms identify sustainability

risks and opportunities and translate them into actions to

boost performance and competitiveness.

He noted that sustainability is the new global driver for

businesses where stakeholders prioritise strong

environmental and social and governance (ESG)

credentials, consumers demand supply chain transparency.

New regulations in international markets are requiring

stricter action on climate issues, responsible sourcing and

sustainability reporting.

Dr. Nsiah-Poku enumerated the positive aspects from

embracing sustainability to include efficient delivery,

access to wider market, stronger investor confidence,

reduced operational risks and long-term profitability. The

initiative aligns with AGI’s mission to foster a globally

competitive industrial sector that supports its ongoing

work on resource efficiency, climate resilience,

responsible conduct and decarbonisation.

The AGI President linked SAVI to Ghana’s ambition to

become a manufacturing hub under AfCFTA and to its

Paris Agreement commitments on emissions reduction and

climate resilience. Denmark’s Ambassador, Jakob Linulf,

urged African producers to meet EU sustainability

standards to increase exports of high-quality goods to

Europe which would drive job creation and economic

development.

Ambassador Linulf said SAVI reflects Denmark’s Africa

Strategy and commitment to mutually beneficial

partnerships, fostering stronger business ties and

promoting sustainable production and trade between

Ghanaian and Danish firms.

See: https://www.myjoyonline.com/agi-partners-danish-

industries-to-advance-value-chain-sustainability/

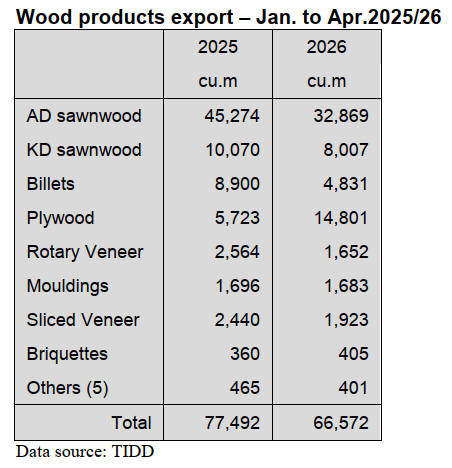

Four out of 16 wood products accounted for 90% of

exports

Ghana exported a total of 66,572 cu.m of wood products

during the period January to April 2026 earning Eur29.34

million, according to the Timber Industry Development

Division (TIDD) of the Forestry Commission source.

Sixteen wood products contributed to the total export

volume in the first four months of 2026, of which air and

kiln-dried sawnwood, billet and plywood (overseas and

regional) accounted for 91% of the total wood products

shipped. For the same period in the previous year these

four products accounted for 90% of the export volume.

All the leading wood products registered declining

volumes in 2026 when compared to the same period last

year, except plywood which recorded a rise in export

volume.

The major markets for Ghana’s wood products during

January to April 2026 were the Asia (38,084 cu.m,),

Europe (13,841 cu.m), Africa (9,510 cu.m), N.America

(4,521 cu.m) and the Middle East (617 cu.m)

The African regional market registered increases of 35%%

in value and 38% in volume against the same period in

2025, Eur2.96 million from 6,901 cu.m of wood products

exported.

Major destinations in Africa included Egypt, Morocco and

South Africa with the ECOWAS sub-region contributing

Eur3.17 million from 8,173 cu.m of the total African wood

products exported compared to Eur2.29 million from

5,765 cu.m for the same period in 2025.

Leading species processed in terms of volume during the

period included teak, denya/okan, dahoma, wawa, cedrela,

eucalyptus and gmelina.

EU supports Ghana restoration of degraded forests

The European Union (EU) is funding an initiative where

an estimated 14,000 hectares of degraded forests across

Ghana’s High Forest and Savanna zones are to be restored.

The Initiative known as the Ghana Forest Restoration

Grant (GFRGS) is expected to build capacity amongst

20,000 farmers and rural residents to support

government’s “Tree for Life” initiative led by the Ministry

of Lands and Natural Resources and the Forestry

Commission.

The EU recently held an event for the GFRGS at the Subri

River Forest Reserve, a key target area. The event brought

together government officials, traditional leaders,

residents, environmental partners and grant recipients. The

event highlighted early successes in Ghana’s flagship

restoration efforts reinforcing the country’s dedication to

rehabilitating degraded forests and enhancing rural

livelihoods.The €6 million project is being implemented

by the European Forest Institute under the EU Sustainable

Forest and Cocoa Programme which works with

communities through agroforestry, natural regeneration

and tree planting.

The Head of the EU Cooperation in Ghana, Ms. Silvia

Severi, said support will promote deforestation-free cocoa,

sustainable land use and climate resilience and said

community-led restoration is key to transforming

landscapes and lives.

The Western Regional Minister, Mr. Joseph Nelson noted

the projects would deliver environmental and socio-

economic benefits by creating livelihoods and

strengthening local capacity.

It is estimated that from late 2025 to 2027 four projects

will receive funding from Proforest, World Vision, Nature

and Development Foundation and Goshen Global Vision

and will be implemented with communities-led partners.

See: https://efi.int/collection/eu-sustainable-forest-and-cocoa-

programme

and

https://thebftonline.com/2026/06/17/ghana-forest-restoration-

grant-scheme-to-restore-14000-degraded-forests/

Through the eyes of industry

The latest GTI report lists the challenges identified by the

private sector in Ghana.

See: https://www.itto-

ggsc.org/static/upload/file/20260615/1781506386105682.pdf

3. MALAYSIA

15% increase in wood product exports targeted

The Ministry of Investment, Trade and Industry (MITI) is

targeting a 15% increase in the value of wood product

exports this year following the encouraging performance

last year when export earnings topped RM14 billion.

The MITI Deputy Minister, Sim Tze Tzin, said Malaysia’s

wood-based industry has diversified to more than 160

international markets thanks to its reputation for high-

quality.

He said the “Made by Malaysia” approach would continue

to be strengthened to increase the competitiveness of the

industry which is now an important contributor to the

country’s exports and GDP.

Malaysian-made furniture continues to be in high demand

in the international market with the US being the largest

export accounting for around 49% of the sector’s total

exports, followed by Singapore at 9.5%.

He added that other major markets include Japan and

Australia accounted for about 5% of exports last year.

See:

https://theborneopost.pressreader.com/article/282162182908112

Wood and bio-composite product development

The Malaysian Timber Industry Board (MTIB) through

the Bio-composite and Fiber Centre (FIDEC) organised a

Consultation and Industry Engagement Session for the

Development of Sustainable Wood and Bio-composite

Products.

The programme aims to strengthen synergy between the

government and industry players in driving the

sustainability of the country's timber sector.

This session focused on several items related to

sustainable wood and bio-composite product development

projects, including:

• Increasing industry understanding of the implementation

of plantation wood and biomass-based projects.

• Delivering programmes on technology adaptation to

improve the efficiency of the production processes and

management of raw materials from plantation wood and

biomass such as oil palm trunk.

• Emphasising the importance of Life Cycle Assessment

(LCA) and Eco-label Certification to meet international

sustainability standards.

Calls for suspension of foreign labour fee increase

The Sarawak Timber Association (STA) is calling on the

Sarawak government to immediately suspend the increase

in foreign worker renewal fees under the Foreign Workers

Transformation Approach (FWTA) system. It also called

on the government to clarify the status of the announced

FWTA fee review and engage affected stakeholders.

The STA pointed out that Sarawak’s growing economy

was expected to require more than 300,000 foreign

workers in the near future and at the proposed renewal fee

of RM1,854 per worker, industries in the State could face

an estimated annual cost of RM556 million.

“Constructive consultation is necessary to ensure that

policy objectives are achieved without placing

unnecessary burdens on businesses that continue to

contribute significantly to Sarawak’s economic

development,” said the STA.

In related news, the continual strong demand for foreign

workers has highlighted a paradox in the Malaysian labour

market. Malaysian Employers Federation (MEF)

president, Dr. Syed Hussain Syed Husman, said the

Statistics Department reports Malaysia’s unemployment

rate is 2.9% of which youth unemployment is 10.1% other

statistics indicate there are 3.47 million manufacturing

vacancies but only 326,407 manufacturing applicants.

The MEF president said the issue was not just job

availability but whether they matched the skills, desire and

expectations of Malaysian jobseekers. He said an

abundance of vacancies remains in the manufacturing,

construction, agriculture and hospitality sectors but these

were often not the preferred choices of young Malaysians.

Syed Hussain said young workers today placed greater

emphasis on career progression, meaningful work,

flexibility and work-life balance compared with previous

generations. He said there was also a growing gap between

what jobseekers expect to be paid and what employers

could realistically offer.

The president of Federation of Malaysian Manufacturers

(FMM) Lee Chor Kok, said the challenge extended

beyond wages. The barriers to local recruitment in

manufacturing go well beyond pay, he said. One of the

most underestimated barriers he said, was the perception

that manufacturing work was low-status, physically

demanding and had limited career prospects.

See: https://www.mtib.gov.my/en/activity/sesi-konsultasi-dan-

libat-urus-industri-bagi-pembangunan-produk-kayu-dan-

biokomposit-lestari.html

and

https://www.thestar.com.my/news/nation/2026/06/22/employers-

say-labour-mismatch-must-be-addressed

Certified forests in Malaysia

Latest statistics from the Malaysian Timber Certification

Council show a total of 5.92 million hectares of certified

forests in Malaysia under the MTCC/PEFC Scheme. There

are 25 MTCS/PEFC Certified Natural Forest (FMU) and

11 MTCS/PEFC Certified Forest Plantations (FPMU).

There are 363 companies holding the MTCS/PEFC Chain

of Custody certificates.

See:www.mtcc.com.my

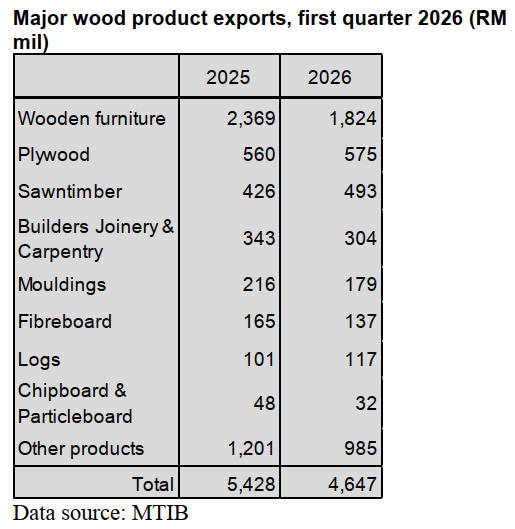

Wood product exports, first quarter 2026

Malaysia’s first quarter 2026 wood product exports faced

headwinds, with regional timber exports, such as those

from Sarawak, dropping 10% year-on-year to RM564

million. This decline reflected broader global market

softness, though value-added segments like wood pellets

showed a 3.3% increase

Through the eyes of industry

The latest GTI report lists the challenges identified by the

private sector in Malaysia.

See: https://www.itto-

ggsc.org/static/upload/file/20260615/1781506386105682.pdf

4.

INDONESIA

Strengthening forestry law to keep pace

with evolving

challenges

Deputy Minister of Forestry, Rohmat Marzuki, said there

is a need to strengthen Indonesia’s Forestry Law to keep

pace with evolving legal, policy and sustainability

challenges. He said revisions are necessary to provide

greater legal certainty in forest governance while ensuring

a balance between economic, social and environmental

functions. The proposed reforms would also reinforce the

recognition and protection of indigenous peoples and

communities living in and around forest areas.

Marzuki highlighted unresolved tenure conflicts as one of

the forestry sector’s most pressing issues, citing

overlapping claims involving forest lands, community

areas, indigenous territories and permits from other

sectors.

A revised Forestry Bill is expected to strengthen legal

certainty, accelerate conflict resolution, support carbon

market development and promote sustainable forest

management that benefits both the environment and local

communities.

See: https://www.antaranews.com/berita/5602392/wamenhut-

penguatan-uu-kehutanan-demi-pengelolaan-hutan-berkelanjutan

Data-Driven forest governance

The Minister of Forestry, Raja Juli Antoni, has launched

the ‘Jaga Rimba Decision Support System’ (DSS), a

digital platform aimed at strengthening data-driven forest

governance and improving decision-making across the

forestry sector. The initiative is part of the ministry’s

broader digital transformation agenda designed to provide

faster, more accurate and transparent information.

The ‘Jaga Rimba’ DSS integrates geospatial information

from across the Ministry of Forestry and its nine

directorates general providing a basis for policymaking

and forest management.

See: https://gorontalo.antaranews.com/berita/409413/menhut-

luncurkan-dss-jaga-rimba-permudah-tata-kelola-hutan

Refining the Multi-Business forestry concept

The Ministry of Forestry is refining the Multi-Business

Forestry (MUK) concept through revisions to Ministerial

Regulation No. 8 of 2021 on forest governance planning

and the utilisation of protected and production forests. The

update is intended to strengthen the implementation of

MUK after five years, ensuring it better meets its intended

goals in managing forest use and governance.

Director General of Sustainable Forest Management,

Laksmi Wijayanti, said the revision will address key issues

such as forest boundary clarity, land-use overlaps,

community benefit distribution, licensing, investment

facilitation, business operations and market dynamics.

Beyond technical adjustments the revision aims to align

forest use with ecosystem restoration while transforming

governance into a more simplified, digital and trust-based

system involving government, communities and permit

holders.

See: https://m.antaranews.com/amp/berita/5615019/kemenhut-

pertajam-konsep-muk-melalui-revisi-regulasi-p8

and

https://mediaindonesia.com/humaniora/902327/regulasi-

multiusaha-kehutanan-direvisi-demi-dorong-manfaat-ekonomi-

hutan

Review of Business Permit compliance

The Ministry of Forestry is strengthening law enforcement

efforts by reviewing companies’ compliance with permit

requirements to support soil and water conservation and

prevent environmental degradation. Director General of

Forestry Law Enforcement, Dwi Januanto Nugroho, said

the ministry continues to assess licensing compliance in

regions such as Sumatra and Aceh as part of broader

disaster mitigation measures.

In addition, the ministry is enhancing its complaint-

handling system to monitor businesses’ fulfillment of

forestry obligations, while ensuring that administrative,

civil and criminal sanctions can be applied concurrently

when violations are identified.

See: https://www.antaranews.com/berita/5602196/kemenhut-

evaluasi-kepatuhan-izin-usaha-utamakan-konservasi-tanah-air

Strict action against land clearing by burning

Forestry Minister, Raja Juli Antoni, has called on

communities and private companies to immediately stop

using fire as a land-clearing method, warning that law

enforcement authorities, including the police and the

Attorney General’s Office, will take strict action against

violators.

Speaking at the 2026 Special Coordination Meeting on

Forest and Land Fire Mitigation, he highlighted the

seriousness of Indonesia’s wildfire situation, noting that

approximately 81,000 hectares of land had burned by May

2026 due to El Niño conditions which are expected to

peak in July. To address the growing risk, the central and

regional governments have strengthened coordination on

mitigation measures, including weather modification

operations and canal-blocking efforts to reduce the

likelihood and spread of forest and land fires.

In related news, Indonesia has reactivated the Forest and

Land Fire (Karhutla) Coordination Desk to strengthen

inter-agency coordination in anticipation of increased

wildfire risks linked to the El Niño phenomenon in 2026

and 2027.

Coordinating Minister for Political and Security Affairs,

Djamari Chaniago, said the move is part of the

government’s preparedness efforts ahead of the dry

season, as El Niño is expected to heighten drought

conditions, reduce rainfall, increase hotspots and raise the

likelihood of forest and land fires.

The government has identified six high-risk provinces:

Riau, Jambi, South Sumatra, West Kalimantan, Central

Kalimantan and South Kalimantan.

The reactivated coordination desk is intended to improve

inter-agency collaboration, avoid overlapping

responsibilities and enhance operational readiness through

optimised standby posts, integrated patrols, stronger early

warning systems and better-prepared personnel and

equipment.

See: https://en.antaranews.com/news/419624/minister-urges-

strict-action-against-land-clearing-by-burning

and

https://en.antaranews.com/news/419673/indonesia-reactivates-

forest-fire-desk-to-face-el-nino-threat

Indonesia, Norway assess forest rehabilitation under

FOLU 2030

Indonesia’s Environmental Fund Management Agency

(BPDLH) and Norway’s Project Management Unit for the

Norway Contribution (PMU-NC) jointly assessed forest

and land rehabilitation progress under the FOLU Net Sink

2030 programme in Hulu Sungai Tengah, South

Kalimantan. The monitoring covered 82 hectares of

restored land across two villages to evaluate plant growth,

vegetation development and overall site conditions.

See: https://en.antaranews.com/news/419861/indonesia-norway-

assess-forest-rehab-under-folu-2030

Germany urged to support finalisation of the Economic

Partnership Agreement

President Prabowo Subianto has urged Germany to

support the rapid finalisation of the Indonesia–European

Union Comprehensive Economic Partnership Agreement

(IEU-CEPA), stressing that the deal would bring tangible

benefits to businesses for both regions. The IEU-CEPA,

which is targeted for ratification in the second half of 2026

and entry into force in 2027, aims to eliminate tariffs on

more than 98% of traded goods and expand cooperation in

trade, services and investment.

See: https://en.antaranews.com/amp/news/419243/prabowo-

urges-germany-to-support-ieu-cepa-finalization

Through the eyes of industry

The latest GTI report lists the challenges identified by the

private sector in Indonesia.

See: https://www.itto-

ggsc.org/static/upload/file/20260615/1781506386105682.pdf

5.

MYANMAR

6.

INDIA

New series of price indices

The Office of Economic Adviser has announced it will

release revised series for wholesale price indicies with a

base year of 2022-23. The new series will replace the

existing series of WPI with base year 2011-12.

In addition, the Office is also releasing a new series of

Output Producer Price Index (OPPI), Trial Input Producer

Price Index (IPPI) and Service Producer Price Index

(Service PPI). The transition from WPI to PPI is in line

with international best practices adopted by advanced

economies and the recommendations of the International

Monetary Fund (IMF).

The all India Wholesale Price Index (WPI) inflation for

May 2026 was 9.68% on a year-on-year basis compared to

8.26% in April 2026. The index for All Commodities for

May 2026 stood at 109.9 (108.8 in April 2026). Year on

year inflation for Primary Articles, Fuel and Power and

Manufactured Products was 4.99%

See:https://eaindustry.nic.in/press_release/press_release_202606.

pdf

Manufacturing accelerated in May

India's manufacturing sector activity growth accelerated to

a three-month high in May, driven by demand strength,

infrastructure projects and new business gains, even amid

inflationary pressures. According to the HSBC India

Manufacturing Purchasing Managers' Index (PMI), this

was above the April reading of 54.7, indicating the

strongest improvement in sector in three months.

Pranjul Bhandari, Chief India Economist at HSBC, said

“India's final manufacturing PMI points to another month

of possible precautionary stockpiling as the Middle East

conflict remains unresolved. Output growth accelerated,

while purchasing activity and stocks of finished goods

rose at a faster pace."

See: https://www.ipsos.com/en-in/india-tops-global-consumer-

confidence-rankings-may-lseg-ipsos-pcsi

Disconnect between housing policy and economic

realities

The Confederation of Real Estate Developers'

Associations of India (CREDAI) represented India’s real

estate sector at the World Urban Forum held in May 2026.

The CREDAI President, Shekhar G. Patel, said, “de-

risking housing finance requires affordable housing

policies that remain aligned with economic realities and

evolving urban costs.

Private capital will participate at scale only when housing

projects remain viable for developers, financially

accessible for buyers and sustainable from a lending

perspective. Housing finance frameworks must therefore

evolve in a way that balances affordability, project

viability and long-term investment confidence.”

He suggested India’s affordable housing challenge is

increasingly becoming a policy-definition and project-

viability issue rather than a demand issue. He noted that

while demand for 60-90 square metre homes remains

strong, many such homes no longer qualify as affordable

housing because of the Rs. 45 lakh price cap.

The definition of affordable, framed around 8 years ago,

has remained unchanged despite inflation averaging nearly

6% annually and housing prices in several cities rising by

8-10% annually.

Further, excessive taxation and approval-related costs,

including GST, stamp duty, infrastructure charges and

approval premiums can account for nearly 35% to 50% of

the final sale value in many cases impacting affordable

housing viability and creating a growing disconnect

between housing policy definitions and economic realities.

See: https://credai.org/media/view-details/?file_no=105

In support of export competitiveness

The Indian rupee has been among Asia's weakest-

performing currencies in recent months. But despite the

sustained pressure on the currency, the Reserve Bank of

India (RBI) has refrained from deploying aggressive

measures which, say experts, could be a strategic move.

While the rupee has fallen more than 11% against the US

dollar over the last 14 months its weakness appears even

sharper when viewed against other major currencies. The

picture becomes particularly significant in comparison

with China.

According to ArunaGiri N, Founder, CEO and Fund

Manager at TrustLine Holdings, the Chinese yuan has

appreciated by nearly 5% during the same period. As a

result, the rupee has effectively depreciated by more than

19% against the yuan. That shift, experts say, could help

India maintain export competitiveness at a time when

Chinese manufacturers continue to succeed in global

markets through aggressive pricing.

See: https://www.ndtv.com/business-news/indian-rupee-fall-

currency-depreciation-rbi-2013-crisis-us-dollar-china-yuan-

india-exports-11590304

Price hike for Nepali plywood

Rising chemical prices have driven up production costs for

Nepal based plywood manufacturers. It is reported that

companies in Nepal have increased prices for plywood by

as much as 15%. Plywood Importers in India have

reported that they are purchasing Nepalese plywood at

higher prices since the start of geopolitical tensions in

West Asia.

Manufactureres in Nepal have obtained BIS licences over

the last few months and have become an exporter of

commercial plywood with the majority of exports directed

to India.

The influx of affordable Nepali plywood, which can be

priced lower than comparable India made products, has

earlier also impacted the domestic Indian manufacturers,

particularly in states bordering Nepal such as Uttar

Pradesh and in Delhi, Rajasthan, Gujarat and Maharashtra.

See: https://www.facebook.com/plyreporter/posts/plywood-from-

nepal-30-costlier-compared-to-2023-nepal-based-plywood-

industry-is-/1110377097758446/Date: 10/04/2026

Rainfall deficit as monsoon progress stalls

Central India faces 63% rainfall deficit as monsoon’s first

round loses momentum and the government has direct

contingency plans to protect crops in 200 districts. The

shortfall in rainfall is concentrated in the regions

the monsoon has failed yet to cover; Maharashtra, the

Konkan coast and the adjoining regions of central India.

The India Meteorological Department (IMD) statistics

show that, apart from northwest India, which has received

5% more rain than normal for this time of the year, all

other regions are in the red, including east and northeast

India (43%), central India (63%) and the southern

peninsula (14%).

Chairing a review of kharif (period for monsoon crop

growning and harvest) preparations Union Agriculture

Minister, Shivraj Singh Chouhan, directed States to

identify districts facing low or uneven rainfall and to draw

up crop-wise contingency plans so that affected farmers

could be “immediately provided with alternatives, advice

and assistance.” Analysts have pointed out that serious

farm disruption could add to retail food inflation, a risk

that the Reserve Bank of India has flagged.

See: https://www.thehindu.com/sci-tech/energy-and-

environment/india-stares-at-35-monsoon-

deficit/article71109891.ece

7.

VIETNAM

Wood and wood product (W&WP) trade

highlights

According to statistics from the Viet Nam Customs

Department, W&WP exports in May 2026 reached US$1.4

billion, down 9% compared to April 2026 but up 1%

compared to May 2025. Of this total, WP exports

amounted to US$927.5 million, down 8% from April 2026

and down 8% from May 2025.

In the first five months of 2026, W&WP exports totalled

US$7.1 billion, up 3% year-on-year. Exports of wood

products reached US$4.5 billion, down 4% compared to

the same period in 2025.

Viet Nam’s W&WP exports to Japan reached US$172

million in May 2026, up 1% compared to May 2025.

During the first five months of 2026, W&WP exports to

Japan totaled US$904.8 million, an increase of 5%

compared to the same period in 2025.

Viet Nam’s exports of kitchen furniture amounted to

US$106 million in May 2026, down 20% compared to

May 2025. Cumulatively, in the first five months of 2026,

exports of kitchen furniture reached US$476 million, a

decline of 15% year-on-year.

W&WP imports into Viet Nam reached US$339.8 million

in May 2026, up 5% compared to April 2026 and up 13%

compared to May 2025. In the first five months of 2026,

W&WP imports totaled US$1.45 billion, representing an

increase of 20% compared to the same period in 2025.

Viet Nam’s imports of wood raw materials in May 2026

reached 689,800 cubic metres, valued at US$241.8

million, up 8.0% in volume and 11.2% in value compared

to April 2026 and up 2.6% in volume and 14.2% in value

compared to May 2025.

In the first five months of 2026, imports of wood raw

materials totaled 2.93 million cubic metres, valued at

US$1 billion, up 10.7% in volume and 20.8% in value

year-on-year.

Viet Nam’s imports of pine wood reached 140,000 cubic

metres in May 2026 valued at US$27 million, up 16% in

volume and 14% in value compared to April 2026 and up

36% in volume and 26% in value compared to May 2025.

In the first five months of 2026 imports of pine are

estimated at 523,700 cubic metres valued at US$100.7

million, up 35% in volume and 26% in value compared to

the same period in 2025.

Viet Nam’s NTFP exports reached US$80.91 million in

May 2026, up 1% from the previous month and up 1%

compared to May 2025. During the first five months of

2026, NTFP exports totaled US$399.96 million, an

increase of 9% year-on-year. This positive growth

momentum indicates a recovery in demand across major

markets for handicrafts, furniture and decorative products

made from natural materials.

Wood product exports

The domestic wood and timber industry maintained

positive export growth in the first five months of 2026

despite global economic uncertainties and increasingly

stringent sustainability requirements from major markets,

according to industry insiders.

Ngô Sỹ Hoài,, Secretary General of the Viet Nam

Timber

and Forest Products Association (Viforest), said exports of

wood and wood products reached US$7.1 billion during

the January-May period, up 4% compared with the same

period in 2025. Of which processed wood products,

mainly value-added indoor and outdoor furniture,

accounted for approximately US$4.5 billion.

The US remained Viet Nam's largest export

destination

with sales estimated at around US$3.5 billion, representing

nearly half of the industry's total exports. Other key

markets included China, Japan, the European Union (EU)

and South Korea, with shipments to China and the EU

recording notable growth.

According to business leaders many export orders had

been secured through the end of the second quarter, with

some companies already receiving contracts for the third

quarter.

The positive performance comes despite persistent

challenges stemming from trade defense measures, rising

logistics costs and increasingly demanding requirements

related to legal timber sourcing, carbon reduction and anti-

deforestation standards.

To achieve the sector's export target of around

US$19

billion this year enterprises are continuing to diversify

markets, accelerate green transformation and increase the

share of deeply processed products while taking advantage

of free trade agreements.

Developments in the Middle East have also become a

key

factor closely monitored by exporters. Recent positive

signals from negotiations between the US and Iran have

eased concerns over disruptions to global energy supplies

and contributed to lower oil prices. A decline in energy

prices could help reduce fuel and international shipping

costs, providing support for the wood sector, where

logistics expenses account for a significant portion of

export costs.

Huỳnh Quang Thanh, General Director of Hiep Long

Woodworking, said geopolitical tensions in the Middle

East had created difficulties for exporters in the first

months of 2026 but the industry still recorded year-on-

year growth.

He noted that ocean freight rates surged following

the

conflict in the Middle East. Shipping a 40-foot container

to the US previously cost around US$1,800-1,900, but

since March rates had at times risen to US$4,300-4,500

per container.

A director of another wood enterprise also shared

similar

expectations, saying that stabilisation in the Middle East

could facilitate the movement of shipments that had

previously been disrupted. He added that reconstruction

demand for infrastructure and housing in the region after

the conflict could create new opportunities for Viet

Namese wood exporters.

Apart from the US, India was also being viewed as a

promising market thanks to its large population and rising

demand for premium furniture products. An increasing

number of Indian buyers had approached Vietnamese

companies to negotiate orders for high-end product lines.

See: https://vietnamnews.vn/economy/1783921/wood-exports-

maintain-growth-momentum-as-firms-eye-middle-east-

rebound.html

EUDR, export enterprises must fully digitise

European Union (EU) has just announced the latest update

to the Anti-Deforestation Regulation (EUDR) effective

May 4, 2026, with a series of notable changes related to

product scope, accountability mechanisms and information

technology systems.

Notably, while EU continues to emphasise goal of

reducing administrative burden on businesses, core

requirements for traceability, supply chain transparency

and control of deforestation risks are becoming

increasingly stringent. According to the latest update,

EUDR simplifies accountability declaration process for

micro and small businesses in initial production stage.

EU has also expanded scope of applicable products,

adding instant coffee and palm oil derivatives – products

assessed as posing a risk of deforestation in some regions

of the world.

At EU Regulations Update Conference on Non-

Deforestation Products (EUDR), following official

announcement of updated regulations on 4 May, Mr. Cyril

Loisel, First Secretary of EU Delegation to Viet Nam,

stated that the changes could help businesses reduce their

administrative burden by approximately 75%. In

particular, Viet Nam's assessment as a country with a low

rate of deforestation will create favorable conditions for

businesses to implement a simpler accountability

mechanism.

However, it is noteworthy that "simplification" does

not

mean losing standards. In fact, recently issued third

version of the EUDR guidelines continues to tighten

requirements for traceability and data transparency. This is

the most difficult part for many Vietnamese agricultural

export businesses today.

According to the regulation, the EU requires

traceability

down to each geographical coordinate (geolocation),

meaning each shipment must have its exact source

location identified using GPS data, digitised maps and

satellite imagery.

This is a landmark change. Previously, businesses

primarily relied on paper documents or certifications of

growing areas for verification; now, control mechanism

has shifted to verification using digital data and satellite

technology. In other words, EUDR is transforming

traceability from a "recommended" requirement into a

mandatory condition for accessing the EU market.

See:

https://asemconnectvietnam.gov.vn/default.aspx?ID1=2&ID8=14

9230&ZID1=8&utm_source=chatgpt.com

Wood exports maintain growth but challenges persist

Viet Nam’s wood product exports maintained their growth

momentum in the early months of 2026, bolstered by a

strong performance in Asian markets, particularly China.

However, the industry is simultaneously grappling

with

significant challenges, ranging from trade defense

measures and increasingly rigorous EU "greening"

requirements to the urgent need for digital and green

transformation to maintain competitiveness.

According to the Ministry of Agriculture and

Environment, exports of wood and wood products in May

2026 arnd around US$1.55 billion. Despite the overall

growth, there is a clear divergence across export markets.

In the first five months of 2026 exports to the US

declined

by 6.5% year-on-year. In contrast, exports to China surged

by 48%, while the Japanese market saw a 6% increase.

Among the 15 largest export markets, the Netherlands

recorded the highest growth, with export values increasing

2.3 times, whereas South Korea experienced the sharpest

decline at 19%.

In addition to competitive pressure, the industry is facing a

rise in trade defense measures. On 11 March 2026 the

Office of the United States Trade Representative (USTR)

initiated a Section 301 investigation into imported wooden

furniture, including products from Viet Nam, regarding

allegations related to trade surpluses and currency

manipulation.

The Viet Nam Timber and Forest Product Association

(VIFOREST) noted that the industry stands at a crossroads

as importing markets tighten environmental standards,

carbon emission regulations and raw material traceability

requirements.

The EU is currently leading the global green

consumption

trend, making criteria for sustainability, transparency, and

environmental responsibility mandatory for imported

wood products. Although the EU accounts for only about

5% of Viet Nam’s total wood exports it remains the

market that defines the highest standards. Businesses must

meet these benchmarks to maintain their global standing.

Beyond external factors, domestic wood enterprises

are

also struggling with internal regulations. Most notably,

obstacles persist regarding the management of Value

Added Tax (VAT) for ordinary semi-processed wood

products, adding further strain to the industry’s operations.

See: https://en.vcci.com.vn/economic-news/wood-exports-

maintain-growth-but-industry-still-faces-dual-pressure-118114

High-quality carbon credits create new opportunities

for Viet Nam

Dr. Nguyễn Sỹ Linh, Head of the Climate Change

Division at the Institute of Strategy and Policy on

Agriculture and Environment under the Ministry of

Agriculture and Environment has said Viet Nam’s

emissions trading system was recognised by the World

Bank for the first time in its State and Trends of Carbon

Pricing 2026 report. Under the current roadmap, Viet Nam

plans to pilot the system starting with around 110 major

firms in the thermal power, steel and cement industries.

The global carbon market is undergoing a significant

shift

from prioritising volume to emphasising the quality of

carbon credits which is widely expected to create new

opportunities for Viet Nam in developing forest carbon

credits.

According to Linh, the World Bank’s State and Trends

of

Carbon Pricing 2026 report shows that the global carbon

market has expanded significantly over the past decade. In

2015, only 58 countries and territories had made use of

compliance carbon pricing instruments. That number has

now increased to 87. The number of emissions trading

systems (ETS) worldwide has risen from 19 to 40, while

carbon crediting mechanisms have increased from 21 to

47.

The World Bank noted that the global carbon market

is

entering a new stage of development, with focus shifting

away from increasing the volume of credits issued and

toward enhancing credit quality and environmental

integrity.

A clear example of this shift is the growing share of

credits generated from forestry and land-use activities,

which now account for about 36%t of the market.

Meanwhile, credits from renewable energy projects have

declined by around 38 % from previous periods.

This trend reflects increasing demand for

high-quality

carbon credits, particularly those generated through

nature-based solutions.

Although the carbon market is taking shape, demand

will

not emerge automatically requiring project developers to

proactively prepare. Quality will also be the primary factor

determining the future value of carbon credits.

Meanwhile, the market is shifting from credit

trading to

investment in credit-generating projects, with greater

attention to carbon rights, land-use rights, benefit-sharing

mechanisms and project governance transparency.

As Viet Nam continues to finalise its regulatory

framework and plans to fully operationalise its carbon

market by 2029, these trends are expected to serve as

important references for policymakers, businesses and

project developers in formulating market participation

strategies, particularly in the forest carbon credit sector.

The Ministry of Agriculture and Environment expects

to

submit applications for the issuance of forest carbon

credits covering the 2023–25 period in the third quarter of

2026.

See: https://vietnamnews.vn/environment/1782655/high-quality-

carbon-credits-create-new-opportunities-for-viet-nam-s-carbon-

market.html?utm_source=chatgpt.com

Land restoration efforts stepped up as degradation

affects 11.8 million hectares

Viet Nam’s forest cover has risen to 42% but officials

warn that policies and technical solutions alone cannot

reverse land degradation without wider social

participation.

More than a third of Viet Nam's land surface, or

nearly

11.8 million hectares, has been degraded, officials said at a

national tree-planting campaign to mark the World Day to

Combat Desertification and Drought. The problem plays

out differently across the country's varied terrain. In the

northern highlands, erosion carves away hillsides, while

along the central coast, chronic drought bakes the land.

In the Mekong Delta, saltwater intrusion from the

sea and

accelerating land subsidence are compounding one

another, creating forms of degradation that are

increasingly difficult to manage. The northern midlands

and mountains bear the heaviest overall burden, with more

than 4.4 million hectares affected.

Viet Nam has made measurable progress on forest

recovery. National forest cover climbed from around 37%

in 2005 to 42% in 2025, above the global average of

roughly 31%.

A national programme launched in 2021 with a target

of

planting one billion trees over five years was completed

ahead of schedule, contributing to reduced soil erosion and

improved water retention across forested watersheds.

But officials cautioned that technical fixes and policy

frameworks alone cannot reverse land degradation. "This

requires the participation of all of society," he said.

Six priority actions for 2026 have been identified:

accelerating surveys and risk mapping for desertification-

prone areas; integrating land restoration goals into national

development planning; rehabilitating natural and

protective forests; deploying digital tools, including

remote sensing, GIS and artificial intelligence to monitor

land resources; securing livelihoods for communities most

exposed to degradation; and expanding international

cooperation while encouraging public-private partnerships

in sustainable forestry.

See: https://vietnamnews.vn/society/1783608/land-restoration-

efforts-stepped-up-as-degradation-affects-11-8-million-

hectares.html?utm_source=chatgpt.com

8. BRAZIL

Amazon Fund celebrates record expansion

The Amazon Fund marked its 18th year of operation with

record results with 153 approved projects with a

cumulative value of BRL5.3 billion. Since 2023 the annual

value of approvals has quadrupled, increasing from

approximately BRL300 million to BRL1.3 billion per

year. The initiative currently supports, directly or

indirectly, more than 650 organisations with activities

spanning 169 Indigenous lands, 192 Protected Areas and

benefiting an estimated 260,000 people throughout the

Amazon region.

During the 36th meeting of the Amazon Fund Steering

Committee (COFA), the Brazilian Development Bank

(BNDES) highlighted the Fund’s expanding international

cooperation network which currently includes nine donors.

New contributions from the European Union, the United

Kingdom and Ireland were also announced totalling

approximately BRL600 million.

The meeting also emphasised the strategic importance of

the partnership with the Brazilian Trade and Investment

Promotion Agency (ApexBrasil) to expand the

international market access for Amazonian bio-economy

products and strengthen Brazil’s image as a global

reference in sustainable development, the bioeconomy and

the green economy.

According to ApexBrasil, cooperatives supported by the

Amazon Fund have already accessed international markets

while trade promotion initiatives have helped to connect

international buyers with production models compatible

with forest conservation. BNDES highlighted prospects

for expanding investments in bio-economy, innovation and

sustainable value chains, reinforcing the Amazon Fund’s

role as a strategic instrument for advancing Brazil’s

climate, environmental and social commitments.

See: https://maisfloresta.com.br/fundo-amazonia-celebra-

aprovacao-anual-de-r-13-bilhao-em-projetos-e-parceria-com-a-

apexbrasil/

Mato Grosso agreement to expand planted forests

The State of Mato Grosso has signed an Environmental

Commitment Agreement (Termo de Compromisso

Ambiental – TCA) with the State Public Prosecutor’s

Office to promote the expansion of planted forests and

progressively reduce the use of raw materials sourced

from authorised conversion of native vegetation by 2034.

This measure responds to a growing imbalance between

supply and demand for forest raw materials in the State

where consumption more than doubled between 2021 and

2024, increasing from 3.4 million to 7.4 million cubic

metres, a 114% increase. In contrast, planted forest areas

of eucalyptus plantations declined from 218,883 hectares

to 211,238 hectares (a 3.5% decrease) during the same

period.

The TCA establishes a plan for large biomass consumers

setting progressive limits on the use of material sourced

from native vegetation under Sustainable Supply Plans

(Planos de Suprimento Sustentável PSS): up to 50% by

2030, 40% in 2031, 30% in 2032, 10% in 2033 and full

elimination by 2034. From that point onward raw

materials must come exclusively from planted forests,

sustainably managed(private) forest or other legally

authorised renewable sources.

New industrial projects or capacity expansions will be

required to demonstrate full supply from renewable and

sustainable sources from the outset.

The agreement also supports the Mato Grosso State Forest

Development Plan which aims to expand planted forest

area and reach at least 700,000 hectares of planted forests

and 6.5 million hectares under sustainable forest

management by 2040, reinforcing a long-term transition

toward a more sustainable and secure forest-based

production chain.

See: https://maisfloresta.com.br/mato-grosso-firma-acordo-com-

ministerio-publico-para-expandir-florestas-plantadas-e-reduzir-

uso-de-vegetacao-nativa-ate-2034/

IBAMA Non-Detriment indings (NDF) for Ipê and

Cumaru

The Brazilian Institute of Environment and Renewable

Natural Resources (IBAMA) has published Non-

Detriment Findings (NDFs) for ipê (Handroanthus spp.

and Tabebuia spp.) and cumaru (Dipteryx spp.), species

listed in Appendix II of the Convention on International

Trade in Endangered Species of Wild Fauna and Flora

(CITES).

The documents consolidate technical and scientific

information on geographic distribution, conservation

status, population dynamics, forest management practices

and trade-related impacts associated with these species

providing the technical basis required for the issuance of

export permits. In practice, the NDF supports the issuance

of export licenses by Brazil’s CITES Management

Authority by ensuring that the harvesting and export of

these species are conducted sustainably and do not

jeopardise their long-term survival in natural ecosystems.

The publication represents an important step by IBAMA

in implementing mechanisms aimed at conserving Brazil’s

native flora while promoting the sustainable use

commercially valuable timber species. The initiative seeks

to balance environmental protection, responsible forest

management and legal certainty for international trade.

The findings were prepared by IBAMA with contributions

from specialists, research institutions, academia and

government agencies. The NDFs will now form part of the

technical references used to evaluate the sustainability of

international trade in ipê and cumaru.

See: https://www.gov.br/ibama/pt-

br/assuntos/notas/2026/ibama-publica-parecer-tecnico-que-

embasa-exploracao-sustentavel-de-ipe-e-cumaru

Export update

Brazilian wood product exports slowed in May 2026

interrupting the recovery trend observed in previous

months. Export values declined by 10% compared to April

while export volumes fell by 17%, reflecting seasonal

factors, the appreciation of the Brazilian real against the

U.S. dollar and uncertainties in the international market.

Despite the monthly decline the sector´s performance

remained relatively stable compared to May 2025 with

export value increasing by 2% and export volume

decreasing by only 2% on a year on year basis.

The decline was led by pine sawnwood and pine plywood

exports which fell by 14% and 10% respectively compared

to the previous month. The expiration of import quotas for

pine plywood in the European Union and the United

Kingdom also contributed to lower shipments to European

markets.

In addition to these market-related factors, the sector is

closely monitoring the potential implementation of an

additional 25% tariff by the United States on certain

Brazilian products following the conclusion of the Section

301 investigation. Although the measure has not yet taken

effect the prospect of new trade barriers has increased

uncertainty among exporters and may affect contracts,

investments and logistics planning.

Brazilian companies are pursuing strategies focused on

market diversification, expanding higher value-added

product offerings, improving operational efficiency and

reducing dependence on specific export destinations.

Despite short-term challenges, the medium- and long-term

outlook for the sector remains positive, supported by

growing global demand for renewable products and

Brazil’s strategic position as one of the world’s leading

suppliers of plantation-grown timber and wood products.

See: https://www.portaldoagronegocio.com.br/florestal/mercado-

florestal/noticias/exportacoes-de-madeira-recuam-em-maio-apos-

recuperacao-e-setor-monitora-impacto-do-cambio-e-das-tensoes-

comerciais#f56e4e1d-c70a-4d6a-bf8f-184718d5c612

In May 2026 Brazilian exports of wood-based products

(except pulp and paper) decreased 3.5% in value compared

to May 2025, from US$295.0 million to US$284.8

million.

Pine sawnwood exports increased 14% in value between

May 2025 (US$ 55.7 million) and May 2026 (US$63.6

million). In volume, exports increased 17% over the same

period, from 236,000 cu.m to 275,100 cu.m.

Tropical sawnwood exports decreased 9.5% in volume,

from 33,700 cu.m in May 2025 to 30,500 cu.m in May

2026. In value, exports increased 4% from US$13.8

million to US$14.4 million over the same period.

Pine plywood exports decreased 6% in value in May 2026

compared to May 2025, from US$66.4 million to US$62.4

million. In volume, exports decreased 6% over the same

period, from 209,800 cu.m to 196,300 cu.m.

Tropical plywood exports increased 18% in volume, from

2,800 cu.m in May 2025 to 3,300 cu.m in May 2026. In

value, exports increased 12% from US$1.7 million in May

2025 to US$1.9 million in May 2026.

As for wooden furniture, exports declined 10% in value,

from US$55.1 million in May 2025 to US$49.7 million in

May 2026.

Export prices

Average FOB prices Belém/PA, Paranaguá/PR,

Navegantes/SC and Itajaí/SC Ports.

Through the eyes of industry

The latest GTI report lists the challenges identified by the

private sector in Brazil.

See: https://www.itto-

ggsc.org/static/upload/file/20260615/1781506386105682.pdf

9. PERU

April 2026 exports 11% higher than in 2025

In April 2026, wood product exports reached a FOB value

of US$23.4 million, an increase compared to the US$21.1

million achieved in the same period of 2025. This increase

represented a positive upward trend of 11%, according to

the Center for Research on Global Economics and

Business of the Association of Exporters (CIEN-ADEX).

According to CIEN-ADEX, shipments included products

such as semi-finished goods (US$9.7 million), sawnwood

(US$8.1 million), firewood and charcoal (US$1.7 million),

furniture and furniture parts (US$1.4 million) and

construction products (US$1.1 million).

The leading destination was France, with exports totalling

US$4.9 million. The Dominican Republic followed with

US$3.2 million, the United States with US$3.1 million,

then China with US$2.8 million and finally Vietnam with

US$2.0 million, completing the top five markets.

Exports of semi-manufactured products increased

According to information provided by the Services and

Extractive Industries Management of the Association of

Exporters (ADEX), during April 2026 exports of semi-

manufactured products reached a value of US$9.7 million

FOB, representing a positive variation of 137% compared

to the same period of the previous year.

France was the main export destination for this subsector,

accounting for 46% of the market share, up over 200%

compared to the same period in 2025. Denmark ranked

second with a 15% share, showing a times 4 positive

growth compared to the same period of the previous year.

Belgium was third with an 8.6% share, registering a

positive percentage change of 80% in relation to the same

period in 2025. The United States occupied fourth position

with an 8% share and a positive increase of 87%. China

closed out the list in fifth position with a 4% share of

semi-manufactured product exports and an increase of

40% compared to the previous year.

Strengthening shihuahuaco monitoring and

conservation

The Supervisory Agency for Forest Resources and

Wildlife (OSINFOR) and the University of Sheffield in

the United Kingdom presented ARBOR, an artificial

intelligence plugin that expands traditional forest

monitoring, moving from logging detection to the

identification and evaluation of specific tree species.

In its first stage, ARBOR has been programmed to

recognise shihuahuaco (Dipteryx micrantha), one of the

most emblematic timber species of the Peruvian Amazon

currently listed in Appendix II of the Convention on

International Trade in Endangered Species of Wild Fauna

and Flora (CITES).

The tool uses artificial intelligence algorithms to segment,

identify and geo-reference tree species from images

obtained by drones. For its programming a geospatial

database from OSINFOR was used consisting of 176

ortho-mosaics obtained from supervised forest

management areas, which include records of 1,883 trees

among them more than 700 shihuahuacos.

The implementation of ARBOR will strengthen the

capacity for monitoring the harvesting of shihuahuacos,

allowing for the generation of more precise information on

the distribution, abundance and condition of this species in

the forest. This will support large-scale forest censuses and

contribute to more efficient decision-making for the

sustainable management and conservation of this resource.

See: https://www.gob.pe/institucion/osinfor/noticias/1410811-

arbor-la-ia-que-llega-al-peru-para-fortalecer-la-supervision-y-

conservacion-del-shihuahuaco

|