Fastmarkets has just released published the European sawn timber

price assessments and market story.

Market overview

European sawn timber markets opened 2026 with cautious sentiment

while Nordic exporters navigated a complex landscape shaped by

persistent demand weakness, evolving supply dynamics following

Storm Johannes and cautiously optimistic projections for

potential improvement by the end of the first quarter. The

January assessment period reflected a market still characterized

by structural headwinds, though with some industry participants

expressing measured hope that the worst of the downturn might be

stabilizing.

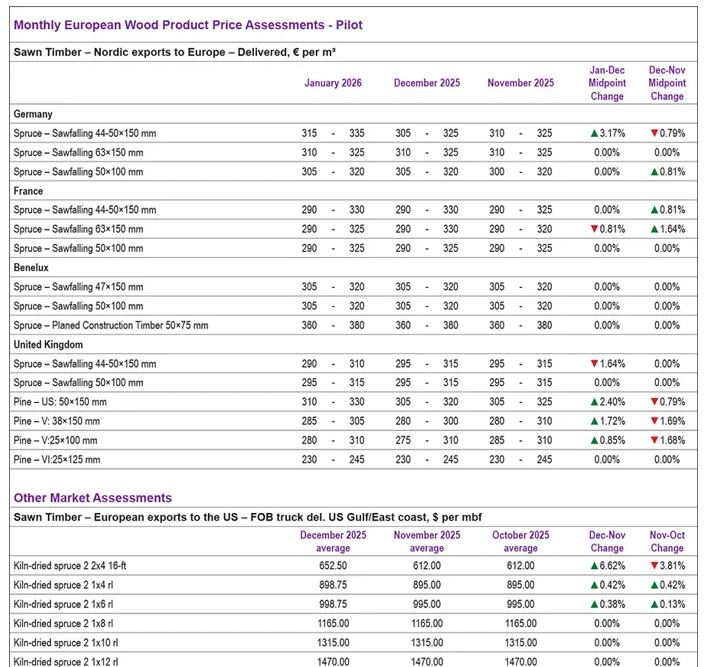

Prices across key European markets were broadly stable in

January 2026, though modest shifts were recorded in select

grades and destinations. Germany saw the most notable movement,

with spruce sawfalling 44-50×150 mm edging up by 3.17% against

December’s midpoint, on account of a rise in the lower limit of

the range. But the other grades held flat in the German market.

The UK displayed a mixed picture: spruce 44-50×150 mm slipped by

1.64%, while pine grades generally increased, with US 50×150 mm

up by 2.40% and V-grade 38×150 mm gaining by 1.72%. France and

the Benelux region were the quietest markets, with virtually all

grades unchanged month on month, the sole exception being spruce

63×150 mm, which edged down by 0.81%. Overall, the data points

to a market in a holding pattern, with no broad directional move

in either prices or sentiment while buyers continued to manage

inventories conservatively heading into the new year.

Market outlook and structural considerations

The Nordic sawn timber sector entered 2026 facing a complex

interplay of persistent structural challenges and tentative

optimism about potential stabilization, according to sources.

While the catastrophic demand collapse of 2022-2023 had

moderated, meaningful recovery remained elusive while European

construction activity continued to lag historical norms due to

elevated financing costs, weakened consumer confidence and

sluggish commercial building pipelines.

January market activity started slower than some participants

anticipated, with importers appearing to have learned cautionary

lessons from 2025’s spring buying surge that left some holders

overextended when summer demand failed to materialize. This

conservative positioning reflected rational inventory management

in an environment of continued macroeconomic uncertainty rather

than fundamental pessimism about longer-term prospects.

Sources expressed cautiously optimistic views that market

conditions could show improvement by the end of the first

quarter of 2026, though such projections remained highly

conditional on broader economic developments and construction

sector recovery. The combination of Storm Johannes supply

uncertainties, evolving species availability dynamics and

persistent cost pressures suggested that Nordic producers would

continue navigating challenging conditions through at least the

first half of the year.

The ongoing industry restructuring across the Nordic region,

characterized by capacity adjustments, operational

consolidations and strategic repositioning, continued to shape

sector dynamics. Producers focused on aligning production with

subdued demand levels while preserving financial flexibility to

respond when market conditions eventually improve. The sector’s

ability to maintain operational readiness while managing through

an extended period of weak fundamentals would prove critical to

positioning for eventual recovery when European construction

markets regain momentum.

European market outlook – WFFC2026 workshop

A dedicated workshop on European markets held at WFFC 2026 in

Helsinki painted a picture of stabilization rather than recovery

across five key destination markets reviewed – Germany and

Austria, France, the UK, Estonia and the Netherlands. Housing

remained the principal demand brake in all markets, partly

offset by steadier activity in renovation, non-residential and

civil engineering segments. Supply chains reshaped by the 2022

loss of Russian and Belarusian timber have hardened into a new

normal, with Finland emerging as a significantly enlarged

supplier in several markets, notably Estonia where it now holds

around two-thirds of import volumes.

Buyers across markets are tightening specifications, requiring

sustainability documentation such as environmental product

declarations (EPDs) and life cycle assessments (LCAs), and

moving toward leaner, more frequent replenishment models –

trends most sharply visible in the UK, where hand-to-mouth

purchasing with 24–48-hour replenishment windows has become

standard. The Netherlands highlighted a persistent shortage of

6-metre lengths and growing demand for C24 rough-sawn timber as

specific product opportunities. France and the DACH region

pointed to engineered wood – CLT, glulam and I-beams – as the

steadiest growth segment, underpinned by low-carbon building

policy.

The overarching conclusion from the WFFC2026 workshop was that

2026 will reward precision over volume: suppliers able to meet

tighter technical, documentation and logistical requirements are

better positioned than those competing on price alone.

Source:

fastmarkets.com