Germany is Europe's largest furniture market, making

developments in the country an important signal for the broader

European sector. After the strong demand surge during the

pandemic period, the market has entered a weaker phase as

consumer spending and housing activity slowed. This analysis

reviews several indicators related to German furniture demand,

including retail turnover, online search behaviour, housing

market activity and consumer confidence, to provide a broader

perspective on how the market has evolved and where it may be

heading.

Furniture retail turnover

German furniture retail turnover has weakened in recent years

following the demand surge during the pandemic period. Sales

volumes increased strongly in 2020 and early 2021 as households

spent more on home improvement and furnishings, but this was

followed by a clear correction as inflation, higher interest

rates and weaker consumer spending reduced demand for durable

goods.

Recent data suggest that the decline has moderated but has not

yet reversed. Furniture retail turnover in Germany fell –1.6%

year-on-year over the last 12 months and –1.4% over the last six

months, indicating that the market remains slightly below the

levels seen in previous years, with demand stabilising but still

subdued.

Furniture search demand improves

Online search behaviour suggests that consumer interest in

furniture products in Germany has strengthened again in recent

years. After declining between 2021 and 2023, the product search

index began to recover and has gradually moved upward through

2024 and 2025. Recent values are among the highest in the

series, indicating that consumers are increasingly searching for

furniture-related products again after a period of weaker

interest. This improvement suggests that early-stage demand

signals for furniture may be recovering even though realised

retail sales remain subdued.

At the same time, searches for furniture retailers have remained

comparatively weaker, creating a divergence between product and

retailer search trends. This may indicate that consumers

increasingly start their purchase journey with product searches

rather than retailer brands.

Early signs of recovery in German housing

Housing activity is closely linked to furniture demand, as home

purchases, relocations and new construction typically trigger

furniture spending. Changes in the housing cycle therefore often

translate into shifts in furniture market activity.

After a sharp downturn between 2022 and 2024, the German housing

cycle is showing early signs of recovery. Both mortgage lending

and residential building permits declined significantly during

the period of rising interest rates, with permits falling

particularly strongly. More recently, however, mortgage volumes

have begun to increase again and building permits appear to have

stabilised after the steep decline, suggesting that the housing

market may be gradually bottoming out.

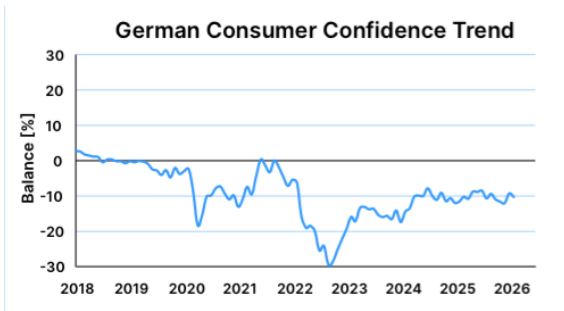

German consumer confidence remains subdued

Consumer sentiment plays an important role in furniture demand,

as furniture purchases are typically discretionary and linked to

households' willingness to make larger expenditures. Changes in

consumer confidence therefore often translate into shifts in

spending on durable goods.

In Germany, consumer confidence dropped sharply during the

inflation shock of 2022, reaching the lowest levels in the

series. Since then sentiment has recovered somewhat, but the

indicator has remained consistently negative over the past two

years. While the worst of the decline appears to be over,

confidence remains below pre-2020 levels, suggesting that

households are still relatively cautious in their spending

outlook.

Conclusion

Taken together, the indicators suggest that the German furniture

market may be approaching the end of its recent downturn, but a

clear recovery has not yet emerged. Retail turnover remains

slightly below recent years, indicating that realised demand is

still weak even though the rate of decline has moderated.

At the same time, several forward-looking signals are becoming

more positive. Furniture product searches have strengthened

again and housing indicators show early signs of stabilisation

after a sharp contraction. However, the continued weakness in

consumer confidence suggests that households remain cautious

about discretionary spending. Overall, the data point to a

market that is stabilising with tentative early demand signals,

but where a sustained recovery will likely depend on further

improvement in housing activity and consumer sentiment.

Source:

furnilytics.com