Fastmarkets is pleased to publish the following European sawn

timber price assessments and market story. The price table below

is in pilot phase, and we are continuing to recruit price

contributors.

Market overview

European sawn timber markets moved into February 2026 in a

broadly cautious mood, with price stability across most grades

and destinations masking a more anxious undercurrent driven by

the eruption of the Iran conflict and its mounting consequences

for global freight markets. The geopolitical shock arrived at an

already delicate juncture for Nordic exporters navigating

elevated log costs, sluggish European construction demand and

the residual uncertainties of Storm Johannes.

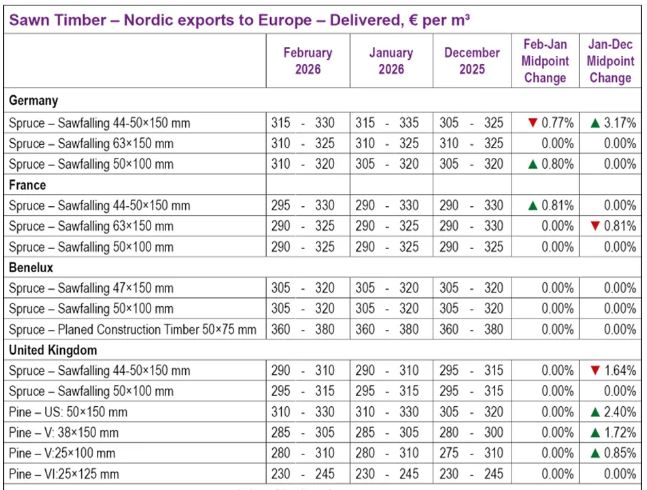

Price movements in February were narrow. In Germany, spruce

44-50×150 mm edged down 0.77% against January’s midpoint, while

spruce 50×100 mm moved in the opposite direction, rising 0.80%

on a firmer lower limit; other German grades held flat. France

showed quiet firmness, with spruce 44-50×150 mm nudging up 0.81%

on a lifted lower limit; other French grades were unchanged.

Benelux and the UK were the quietest markets, with all assessed

grades flat across the board. The overall picture is one of a

market in a holding pattern, with buyers managing inventories

conservatively and no broad directional impulse in either

direction.

The Middle East conflict: freight costs and the MENA shadow

The conflict in Iran has sent shockwaves through global shipping

markets, with direct consequences for Nordic sawn timber

exporters. As of mid-March, war surcharges on container

shipments to the Middle East and North Africa had jumped by

approximately $3,000 per container, about $60-plus per cubic

meter, or around €55 per cubic meter, on a standard 40-foot

container carrying 45-47 cubic metres of timber.

Against a baseline sea freight cost of approximately €50 per

cubic meter, the surcharge effectively more than doubles the

shipping component of the delivered price, which translates to a

20-25% increase in total cost that neither buyers nor sellers

can readily absorb. Sources active in MENA markets described the

surcharges as too high to pass on, with a significant number of

shipments cancelled as a result.

The Middle East and North Africa had been among the more

resilient demand destinations for Nordic exporters through an

otherwise difficult 2025. Egypt alone was receiving an estimated

€240 million worth of EU sawn softwood in the first half of

2025, and the broader MENA region had been projected to grow at

a compound annual rate of around 9% through 2032, driven by Gulf

infrastructure programmes and persistent North African housing

deficits.

Major carriers including Maersk, MSC and Hapag-Lloyd have

suspended Hormuz crossings until further notice, with vessels

rerouted around the Cape of Good Hope, adding weeks to transit

times and compounding cost pressures. The Houthis, whose Red Sea

campaign had only recently wound down following a ceasefire, had

threatened to escalate again, which would layer additional

disruption on top of the Hormuz closure.

The freight shock compounds existing cost pressures at the

production level. Fastmarkets senior economist Dustin Jalbert

flagged the compounding effect on logging operations. Surging

diesel costs, especially in Central Europe, are adding to log

procurement pressures that are already almost impossible to pass

on downstream, according to Jalbert. Jalbert said a potential

stagflationary effect on the broader European wood products

complex, which is a scenario in which energy cost spikes hit

pulp and paper operations, could threaten sawmill residual

revenues when other income streams are under strain.

Producer conditions and competitive dynamics

Swedish sawmill operators continued to navigate a difficult

margin environment in February, with persistently elevated

sawlog costs pressing against flat or modestly declining sales

prices in key markets. Sources noted that sawlog prices remain

materially higher than sawn timber prices for both pine

(redwood) and spruce (whitewood). The conditions that made the

fourth quarter of 2025 exceptionally hard for Swedish producers

had not materially improved at the start of the new year, though

some participants expressed tentative hope that the first

quarter of 2026 might mark a turning point. Some decrease in

sawlog prices has become visible in recent procurement, which

would offer modest relief if the trend holds.

The pine-spruce species imbalance that characterized late-2025

markets remained a live issue in February. Spruce continued to

command a premium over pine in most markets, and while the

possibility of substituting whitewood with redwood has been

discussed, sources indicated that uptake in key European markets

remains limited. Planing mills are effectively unable to use

pine as a substitute; in construction timber applications such

as KVH and lamellas, pine can work for some products, but

tradition and client expectations–including the expectation that

redwood be priced lower than whitewood–continue to inhibit

broader switching, even in non-visible applications.

Second quarter negotiations are ongoing and sources told

Fastmarkets that the market appears to be moving after an

extended period of stasis.

Production curtailments in Sweden and among other Nordic

producers dampened their appetite to push hard in

January-February, with a degree of mutual wait-and-see evident

as participants watched moves of larger players closely, before

committing to their own moves.

In the Dutch market, particularly on SLS (Scandinavian Lumber

Standard) in broader sizes and long lengths, conditions were

described as tight.

Certification continued to attract commercial attention: PEFC

remains acceptable for the majority of buyers, but some major

clients, particularly in the Benelux region, are requiring FSC

in response to governmental procurement requirements.

Market outlook

The outlook for March and the broader first half of 2026 is

materially more uncertain than it appeared at the start of

February, principally because of the freight cost shock

generated by the Middle East conflict. European construction

demand continues to offer few positive signals, with residential

building remaining the principal brake across all major

destination markets and renovation and non-residential segments

providing only partial offset. Some Nordic producers said they

were counting on MENA demand to help absorb production volumes;

the degree to which that outlet remains viable will depend on

how quickly or slowly the geopolitical situation resolves.

For the European destination markets assessed in this pilot,

sources indicated that the immediate implication is continued

price stability underpinned by cautious buyer positioning rather

than any fundamental improvement in end-use demand. Sources

continue to monitor whether the hesitant optimism around a first

quarter inflection point will survive contact with the freight

and geopolitical risks weighing on the sector.

Source:

fastmarkets.com