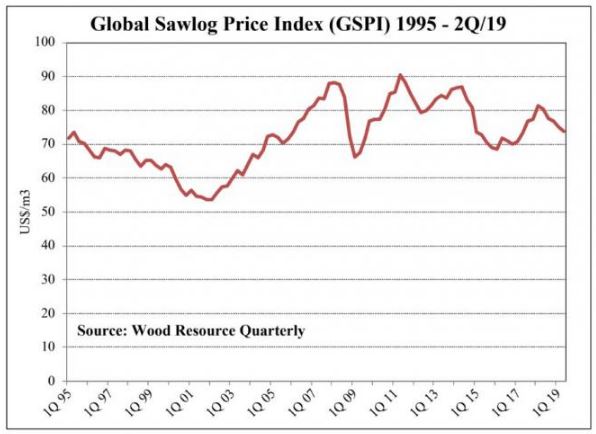

In the 2Q 2019, the European Sawlog Price Index (ESPI)

fell to a nine-year low, reported Wood Resources International in

its Wood Resource Quarterly. In Euro terms, average sawlog prices in

Austria and Germany have fallen almost 20% over the past two years,

thus improving the competitiveness of the two countries sawmilling

industry. US softwood log shipments to China have fallen by $124

million in value since the trade war started May 2018.

Global Pulpwood Prices

Prices for softwood pulplogs and wood chips fell in practically all

markets around the world in the 2Q/19 because of a combination of

factors. These factors varied by region, but included reduced fiber

demand, lower pulp prices, insect-damaged forests, and favorable

logging conditions.

In the 2Q 2019, the Softwood Fiber Price Index (SFPI) fell by 1.5%

from the previous quarter.

The Hardwood Fiber Price Index (HFPI) was down 0.5%

quarter-over-quarter in the 2Q 2019. Hardwood pulplog prices fell

the most in Indonesia, Germany, the US Northwest and Brazil, while

prices increased in Russia, Japan and Australia.

Global Pulp Markets

Pulp mills around the world have had to tackle both weak demand and

high inventories of pulp during the second quarter of 2019. The

prices for NBSK and BHKP market pulp in July were down as much as

26% and 18% respectively, from October of last year.

Global Lumber Markets

With unchanged or slightly higher log costs and lower lumber prices

in the 2Q, sawmills in North America saw their profit margins

decline again after the short-lived improvements seen in the 1Q

2019.

Demand for lumber in China, the UK, Egypt and the Netherlands

increased this year despite a slowdown in the global economy.

Lumber production in Canada from January to May 2019 was 9% lower

than it was during the same period in 2018. Most of the decline were

in British Columbia, where production was down 16.5% year-over-year.

China imported almost eight million m3 of softwood lumber in the 2Q,

a new quarterly high. Russian deliveries reached five million m3, a

39% increase from the 1Q 2019.

The increased lumber demand in the MENA region continued in the 1Q

2019 when the two major markets, Egypt and Saudi Arabia, increased

their importation by over 50% from the 1Q 2018.

Global Biomass Markets

In 2015, only 80,000 tons were exported to Japan, while an estimated

600,000 tons (24% of all exports) are expected to be shipped to this

relatively new market in 2019.

Wood fiber costs for US pellet manufacturers fell in the 2Q, while

Canadian pellet producers experienced higher costs due to reduced

supply of sawmill residues.

Source: Wood Resources International