|

Report

from

Europe

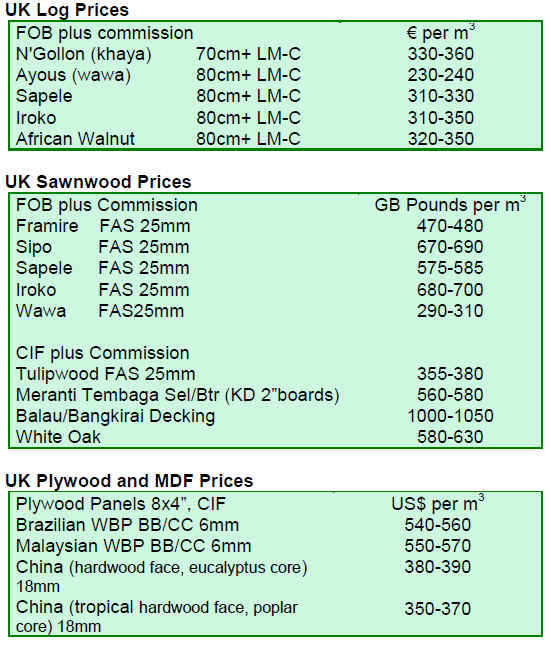

Extended European delivery times for African hardwood

EUWID reports that German wood importers are having difficulty placing new orders in Africa. Although African sawmill��s supply capability varies depending on the producer, species and specification, the problem in procurement appears to be increasing rather than declining.

EUWID notes that supplies of all major commercial redwood species such as sapele, sipo and iroko are very tight with delivery periods for new orders now extending to the end of the year in some cases. Deliveries of whitewood species such as wawa / ayous �C which had hitherto been more readily available �C are also now subject to longer delays.

No upswing in European demand for African lumber

EUWID reports that there has been no significant upswing in European demand for African lumber in recent weeks. In the case of sapele and sipo, the low level of consumption can still largely be supplied from existing landed stocks.

While some efforts are being made by European importers to push through price increases for onward sales of these stocks to manufacturers and distributors, in many cases prices still fall short of replacement levels.

However, stocks of iroko in Europe are more limited and, in the absence of potential substitutes, importers have been better placed to force through price increases for this species.

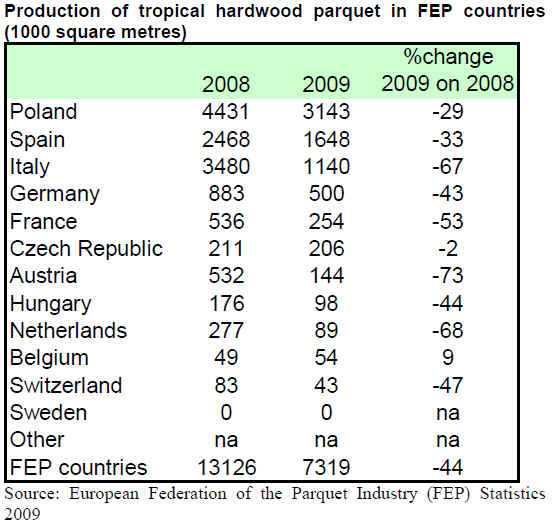

European parquet flooring production slipped 20% in 2009

Statistics issued by the European Parquet Flooring Federation FEP on the occasion of their 54th General Assembly in Rome in May confirm FEP��s preliminary estimates of a 20% reduction in European parquet flooring production last year to a volume of 67.5 million square metres. Particularly steep declines in production were recorded in Italy, the Nordic countries, Poland and Spain during 2009. However, all countries covered by the FEP membership were affected to some extent.

The leading producers in the FEP region in 2009 were Poland (17.5% of total production), Germany (14.8%), Sweden (13.8%), Austria (10.7%), Spain (9.8%), and France (9.4%).

In 2009, multi-layer parquet increased its share of production in FEP countries by 1% and now accounts for 78% of total parquet production. After several years of stabilisation, the share of solid wood parquet in European production slipped 16% last year. The remainder of production comprises mosaic and lamparquet, each with a 3% share.

Meanwhile, consumption of parquet flooring in the FEP area fell by 15.31% in 2009 to 86 million square metres. Consumption of parquet flooring dropped across the FEP region, although particularly large reductions were recorded in Hungary, Italy, Scandinavia, Spain and Poland.

Tropical wood losing ground to oak in the European flooring sector

The FEP statistics are particularly interesting for the hardwood industry as those are the only numbers regularly compiled for an European end-use sector, providing an insight into usage rates of different wood species. The 2009 figures tend to reinforce earlier reports that oak has been consolidating its dominant market position in European finishing sectors during the time of recession. Oak��s share of total parquet flooring production in the FEP region grew from around 56% in 2008 to nearly 63% in 2009.

The major loser in this continuing shift to oak has been tropical hardwoods, which saw their share of usage rates dropping from around 15% in 2008 to only around 10% in 2009. While production of tropical parquet flooring fell in all the FEP countries during 2009, the decline was particularly sharp in Italy, France and Austria (see table). This is partly explained by mounting supply problems for tropical hardwoods at a time when manufacturers were increasingly looking to order wood on a just-in-time basis. Another factor was increased concern for environmental issues which led some manufacturers, notably in Austria, to boycott the use of tropical wood last year.

AEIM��s commitment to legal and certified tropical hardwood

AEIM, the Spanish timber trade federation, has signed an agreement with the environmental non-governmental organisation WWF requiring that all wood imported by members from West and Central Africa must at minimum be legally verified and preferably FSC certified. In support of the agreement, WWF intends to publish a list of Spanish companies that offer FSC certified tropical timber products.

The agreement came after a tour of Spanish timber importers to Cameroon in March 2010 supported by the Spanish development agency AECID. The Spanish companies visited FSC-certified timber suppliers during the tour. The agreement also follows on from a recent non-binding recommendation of the Spanish Council of Ministers that public authorities should purchase only FSC or PEFC certified wood products.

Cameroon signs Voluntary Partnership Agreement with the EU

On 6 May 2010, Mr. Raul Mateus Paula, the Ambassador representing the European Union in Cameroon and Mr. Elvis Ngolle Ngolle, Minister for Forests and Wildlife representing Cameroon concluded negotiations of a Voluntary Partnership Agreement (VPA) on Forest Law Enforcement Governance and Trade (FLEGT) in forest products to the EU. The VPA expresses a strong mutual commitment to respond to the problem of illegal logging, by linking good forest governance in Cameroon with a trade agreement and leverage offered by the EU��s internal market.

This brings to a close a negotiation process that has spanned several years. The two parties have agreed on the key elements of a FLEGT licensing scheme. These include: (a) a clear description of legal requirements (legality definition); (b) systematic verification of legal compliance; (c) timber tracking through the supply chain; (d) licensing procedures; and (e) independent auditing.

The Agreement also lends support to elaborate policy and legal reforms that will foster good governance,transparency and accountability in the forest sector of Cameroon. Cameroon intends to build a national system to assure legality which will apply to all exports no matter the final market destination and to timber produced for the domestic market as well. The EU for its part will guarantee free and unrestricted access to its entire market of all FLEGT licensed timber products coming from Cameroon and will seek to increase visibility of FLEGT licensed products in the EU. The EU and its Member States are also contributing to the needed sector reforms and providing support to development and upgrading of regulatory systems framed in the VPA. It is expected that the first FLEGT licenses from Cameroon will be issued by the end of 2011.

The conclusion of these negotiations follows closely on the heels of VPA agreements with Ghana and the Republic of Congo (Brazzaville). Negotiations are on-going with Liberia and Central African Republic as well as Indonesia and Malaysia with many other countries showing interest to enter into dialogue too.

According to the European Commission's press release issued on the occasion of the signing of the agreement: "with increasing expectation in the European market for independently verified proof of legality of timber products, the VPA should help Cameroon to consolidate and improve its European market access".

For further information, contact:

Minist��re des For��ts et de la Faune (http://www.minfof.gov.cm/)

Mr. Koulagna Koutou Denis: koulagnakkd@yahoo.fr

D��l��gation de l'Union Europ��enne au Cameroun (http://www.delcmr.ec.europa.eu/)

Mr. Carl Frosio: Carl.frosio@ec.europa.eu

Related News:

��

|