| Home: Global Wood | Industry News & Markets |

��

| Home: Global Wood | Industry News & Markets |

|

| ||||||||||||||||||||||||||||||

|

Report from Europe

Hardwood plywood makes gains �C other market sectors remain

fragile

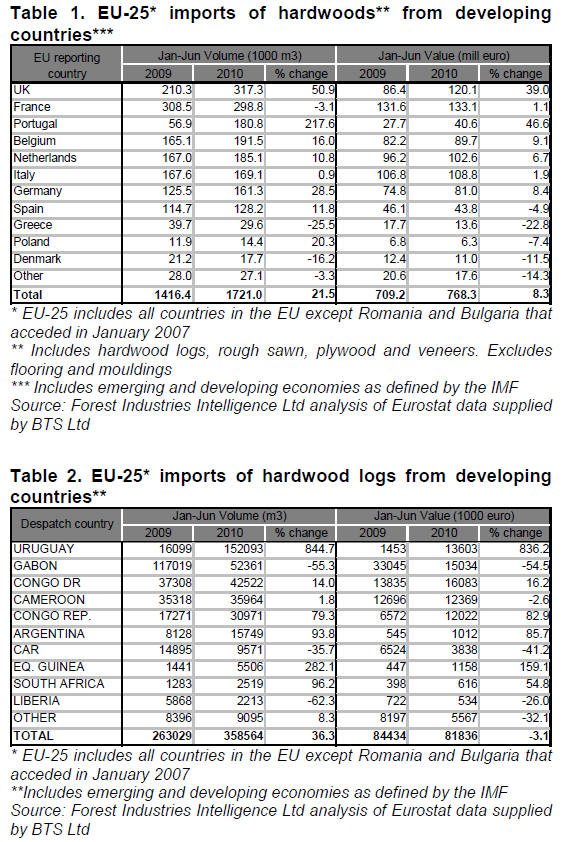

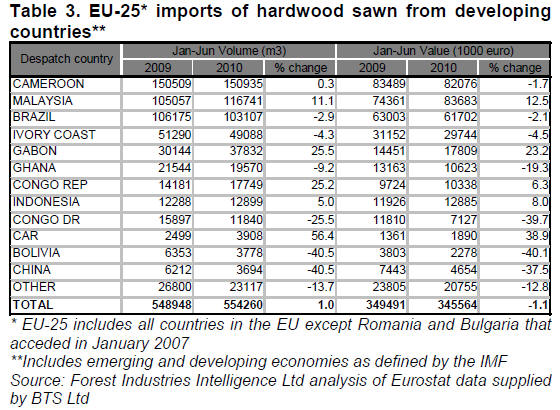

The trade data confirms anecdotal reports that the anticipated recovery in European tropical sawn lumber market was very slow and patchy during the first half of 2010. Table 3 shows that EU-25 imports of hardwood sawn from developing countries during the first half of 2010 were almost equivalent to imports during the same period in 2009. Gains in EU imports of hardwood sawn lumber from Malaysia, Gabon and the Congo Republic were offset by continuing declines in imports from Brazil, Ivory Coast, Ghana and the Democratic Republic of Congo.

There were, however, much clearer signs of recovery in the European market for hardwood plywood during the first half of 2010 (Table 4). Overall imports of hardwood plywood from developing countries increased almost 40% during the six month period compared to the same period in 2009. There was particularly strong growth in European imports of hardwood plywood from China, confirming anecdotal reports that China has been gaining market share in this sector during the recession, largely owing to its continuing ability to offer product at highly competitive prices. However sales of Malaysian and Indonesian plywood also made significant gains. Chinese and tropical hardwood plywood have benefited during 2010 from rising prices for Russian birch plywood as a result of the forest fires that raged through Russia this summer. Another notable trend this year is the emergence of Uruguay as a more significant supplier of hardwood plywood to the EU following intense marketing of products derived from plantation-grown eucalyptus as an environmentally-friendly alternative to tropical hardwood plywood.

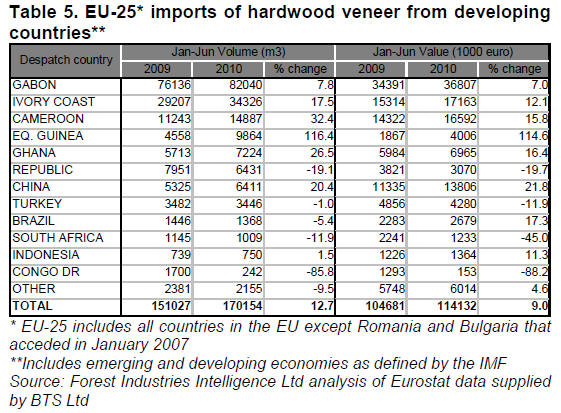

The ban on log exports from Gabon is just beginning to reveal itself in

the form of increased European imports of rotary veneers for plywood

manufacture (Table 5). Overall EU veneer imports during the first half

of 2010 were up nearly 13% on the same period the previous year. An

increase in European veneer imports from several countries more engaged

in the sliced veneer business, as opposed to the rotary veneer business,

also suggests some improved buying by the European decorative panel and

furniture sectors. During the first half of 2010, EU veneer imports

increased from Gabon, Ivory Coast, Cameroon, Equatorial Guinea, and

Ghana. There were also small increases in European imports from China

which - despite a huge veneer manufacturing sector - has yet to emerge

as a large exporter of this commodity.

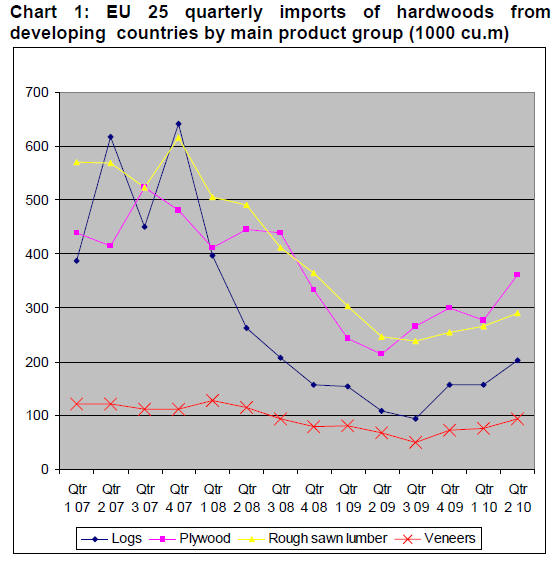

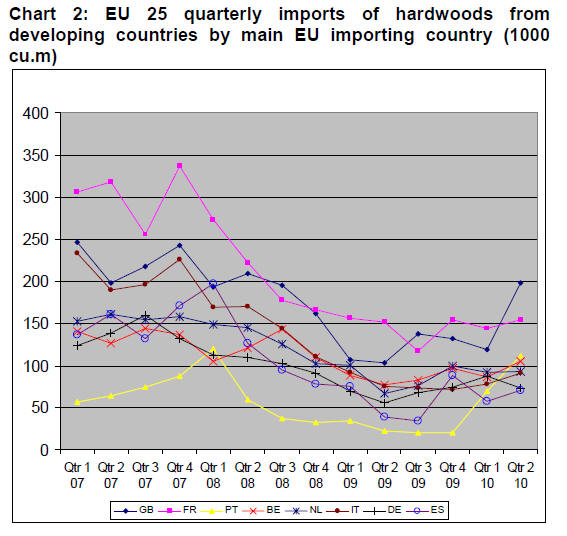

Chart 2 shows that imports of hardwood products from developing countries by the UK and Portugal made significant gains in the second quarter of 2010, due respectively to spikes in imports of plywood and eucalyptus logs. Imports into Belgium and Italy continued to improve slowly during the second quarter of 2010, while imports into Spain showed a slight improvement on the desperately low levels recorded in the first quarter of 2010. However, the recovery in German imports stalled during the second quarter of 2010, particularly disappointing after three consecutive quarters of growth between June 2009 and March 2010.

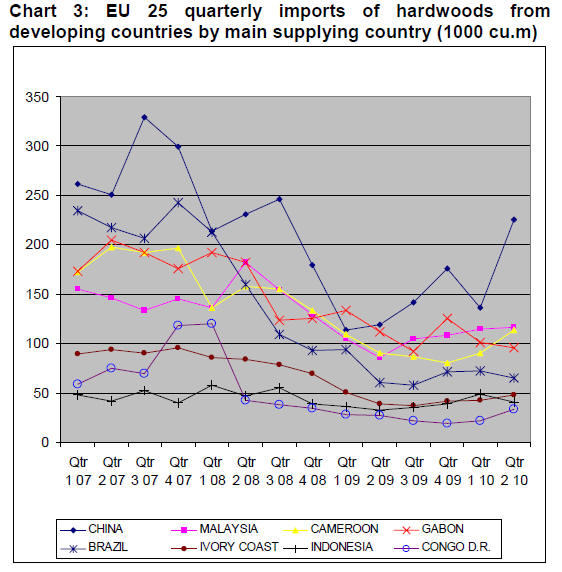

Chart 3 shows that China was the major beneficiary of the tentative market

recovery in Europe during the second quarter of 2010, mainly a result of

rising demand for hardwood plywood in the UK. European imports of

hardwood products from Cameroon and the Democratic Republic of the Congo

have also shown fairly consistent growth this year. European imports

from Brazil and Indonesia slowed again in the second quarter after

showing signs of improvement in the opening months of the year. Imports

from Malaysia and Ivory Coast remained stable at historically low levels

between the first and second quarters of 2010.

�� | ||||||||||||||||||||||||||||||

|

Abbreviations

| ||||||||||||||||||||||||||||||

|

Source: ITTO' Tropical Timber Market Report |

CopyRight (C) Global Wood Trade Network. All

rights reserved.

��