|

Report

from

Europe

European domestic hardwood production rebounds

Data from the UNECE Timber Committee indicates that

hardwood production across the European sub-region

rebounded during 2010 (the UNECE European sub-region

includes all countries within the continent of Europe plus

Turkey but excluding Russia).

Following an 18% decline in hardwood saw and veneer

log production in the region between 2007 and 2009 to

29.7 million cu.m, production rebounded by 12% to 33.2

million cu.m in 2010.

Significant increases in hardwood log production were

recorded in Romania, Germany, Turkey, and Latvia during

2010. 26.2 million cu.m (78%) of total European

hardwood log production during 2010 was in EU

countries.

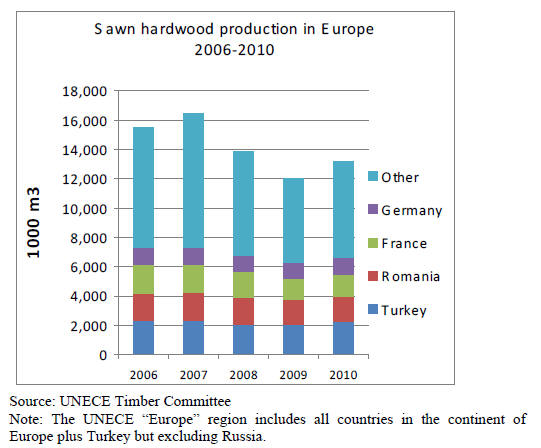

Turkey was the largest producer of sawn hardwood in Europe

European production of sawn hardwood followed the same

general trend. A 26% fall in production between 2007 and

2009 was followed by a robust 9% rebound during 2010

(Chart 2). Significant gains in production were in Turkey

(8.8%), Germany (6.6%) and Croatia (5.6%).

Turkey was the largest producer of sawn hardwood in

Europe in 2010. However most sawn hardwood in Turkey

is produced from low-grade domestic timber, as well as

small-dimension plantation logs and is destined for the

pallet and packaging industry with only a small proportion

earmarked for export.

Germany, France and Romania remain by far the dominant

producers of higher grades of European sawn hardwood.

The rising log harvest in 2010, combined with an

underlying lack of consumption, has meant that there have

been no major hardwood log shortages in Europe in recent

times. Supplies of beech logs have generally been

adequate.

Short-term concerns have occasionally arisen over

supplies of oak logs, particularly with rising demand in

export markets, notably from China, and following severe

winter weather in both 2009 and 2010 which briefly

curtailed harvesting levels.

However oak log supply problems had eased greatly by

the end of the first quarter of 2011 as weather conditions

improved and log exporters were less active at French and

German auction sales.

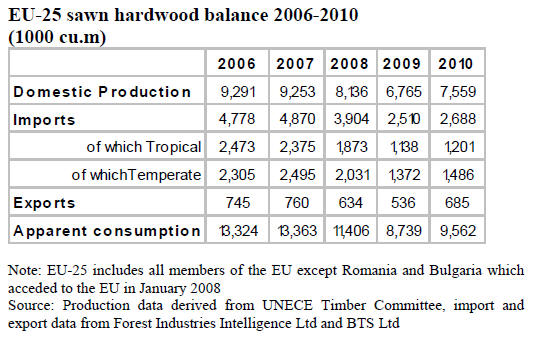

European domestic production more dominant

Within the EU-25 group of countries, apparent

consumption of sawn hardwood increased by 9.4% during

2010, from 8.7 to 9.6 million cu.m.

While a significant gain, consumption levels were still

well down on levels of over 13 million cu.m which

prevailed prior to the economic crises. The overall figure

also hides important changes in sources of supply and

demand.

Domestic industry weathered the crisis better than external suppliers

While all wood suppliers into the EU market suffered

severely during the recession, the signs are that the

domestic industry weathered the storm better than most

external suppliers. During the period 2006 to 2010, the

share of domestic hardwood sawn lumber in overall

supply to the EU-25 group of countries increased from

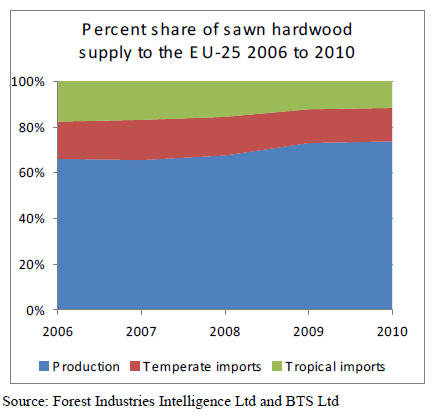

66% to 74%.

The share of non-EU temperate hardwood suppliers

declined from 16% to 15%. However the major loser in

this process has been tropical hardwood which saw share

of European sawn hardwood supply fall from 18% to 12%

in the four year period.

While all major tropical supply countries experienced

some slippage in European market share for sawn

hardwood, the trend was particularly pronounced for

Brazil (share of EU supply falling from 4.1% to 2.9%)

Ivory Coast (share falling from 2% to 1%), and Ghana

(share falling from 0.8% to 0.4%).

Major shift in EU sawn hardwood supply

A number of factors have played a role in this major shift

in European sawn hardwood supply including:

• increased diversion of global hardwood supply

away from Europe to China and emerging

markets;

• a move to smaller stock-holdings and just-in-time

ordering during the credit crunch which has

tended to favour more readily available products

with shorter lead times;

• the willingness of European domestic suppliers to

deliver to the precise specifications of European

manufacturers;

• the willingness of the European state forest sector

to continue to harvest hardwood logs during the

recession despite relatively low log prices;

• the continuing strong fashion for European oak in

the region;

• the development of an expanding range of

treatment techniques allowing use of European

hardwoods for a much wider range of looks and

applications;

and

• environmental concerns which have benefited

FSC and PEFC certified hardwoods, the majority

of which derive from Europe.

Low hardwood demand from cabinet, furniture and

parquet industries

On the demand side, European consumption of sawn

hardwood recovered quite strongly in France, Germany,

and Sweden during 2010 and early 2011. However

consumption has remained at historically low levels in

many European markets, notably Spain, Portugal, and

Italy due to continuing low demand in the cabinet,

furniture and parquet industries.

The strong euro has meant that Europe’s important

furniture sector is coming under particularly intense

pressure from competitors in Asia.

Exports of EU hardwoods recovering

Export markets for European sawn hardwood, particularly

oak and ash, in China and Vietnam have also been

recovering. Between 2009 and 2010, EU-25 sawn

hardwood exports to China increased from 115,000 cu.m

to 205,000 cu.m, while exports to Vietnam increased from

21,000 cu.m to 40,000 cu.m.

In contrast, European sawn hardwood exports to the

Middle East and North Africa have been declining. Recent

political upheaval in this region has resulted in declining

demand, particularly for beech in Egypt, Jordan, Syria,

and Tunisia.

Despite pockets of poor demand, according to the UNECE

Timber Committee, reports from the European hardwood

sawmilling sector have been generally positive in 2011

and there are expectations that overall sales this year may

be 15% to 20% higher than in 2010.

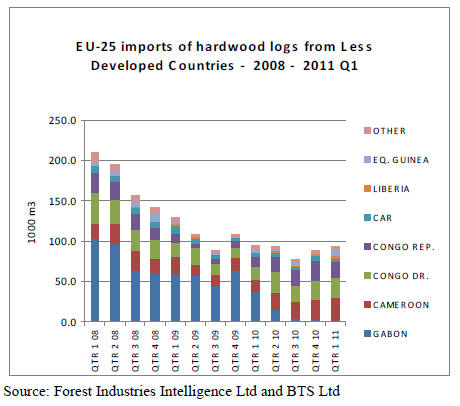

Tropical log imports still close to recession levels

The EU-25 imported 93,400 cu.m of tropical hardwood

logs during the first quarter of 2011, a 6% increase on the

previous quarter, but 1% down on the same quarter in

2010.

Following the dramatic decline in imports from over

200,000 cu.m in the first quarter of 2008 to a low of

88,000 cu.m in the third quarter of 2009, quarterly imports

have stabilised at this lower level.

In addition to the recession, a major factor driving the

recent decline in log imports was Gabon’s imposition of a

log export ban from May 2010 onwards. Rising log

imports from Cameroon, Democratic Republic of Congo,

Republic of Congo, Equatorial Guinea and Liberia have

only partially offset the decline in availability from Gabon.

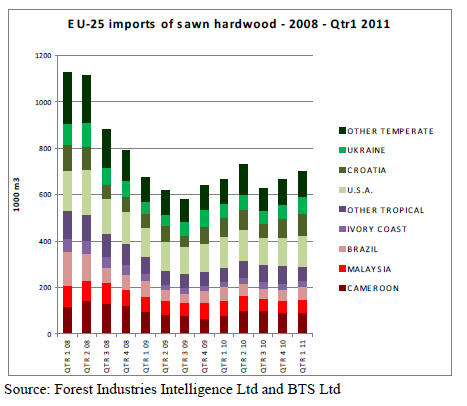

Rise in EU sawn hardwood imports driven by

temperate species

The EU-25 imported 702,000 cu.m of sawn hardwood

during the first quarter of 2011, a 5% increase on the

previous quarter and a 6% increase on the same quarter in

2010.

However tropical sawn hardwood imports of 293,000 cu.m

during the first quarter of 2011 were 1% down on the

previous quarter and only 2% up on the same quarter in

2010.

This compares to temperate hardwood sawn imports of

409,000 cu.m during the first quarter of 2011, up 10% on

the previous quarter and up 9% on the same quarter in

2011. Most recent gains in EU-25 imports of temperate

hardwoods have been made by Croatia and Ukraine.

Recent news is not all bad for tropical hardwoods.

Brazilian sawn hardwood has been regaining some of the

ground lost in the European market, particularly in France

and Belgium.

In the first quarter of 2011, EU-25 imports of sawn

hardwood from Brazil were 56,000 cu.m, up 22% on the

previous quarter. Meanwhile European imports from

Cameroon started 2011 much more strongly than the

previous year, with larger volumes arriving in Belgium,

Netherlands, UK, Ireland and Italy.

Total EU-25 imports of sawn hardwood from Cameroon

reached 92,000 cu.m in the first 3 months of 2011, up 14%

on the same period in 2010.

These gains helped offset relatively weak first quarter

imports of sawn hardwood from Malaysia (58,000 cu.m)

and Ivory Coast (24,000 cu.m).

EU hardwood veneer imports weaken again

The EU-25 imported 118,000 cu.m of hardwood veneer

during the first quarter of 2011, an 8% decline on the

previous quarter and a 4% decline on the same quarter in

2010 (Chart 6).

Tropical hardwood veneer imports of 69,000 cu.m during

the first quarter of 2011 were 10% down on the previous

quarter and 4% down on the same quarter in 2010. This

compares to temperate hardwood veneer imports of 60,000

cu.m during the first quarter of 2011, down 2% on the

previous quarter and 3% on the same quarter in 2011.

The continuing weakness of the European veneer trade is

particularly troubling considering the wide range of enduse

sectors for hardwood veneers, the resources committed

to boosting the share of real wood by large veneer

manufacturers, and the decline in Europe’s tropical

hardwood log imports.

European plywood manufacturers might reasonably have

been expected to have offset the decline in availability of

okoume logs by importing more rotary veneer from

Gabon.

However European imports of this commodity have

remained low as manufacturers have been struggling in the

face of tight margins and rising competition from a range

of lower-priced panels. European imports of thicker rotary

veneer for flooring are also depressed as European

flooring output is low due to weak construction growth

and competition from artificial surfaces.

The weak construction sector has also hit mainstream

markets for sliced veneer, including doors, panels and

furniture. The latter sector is struggling in the face of stiff

competition from Chinese manufacturers.

At the same time, real wood veneer has continued to lose

out to artificial surfaces. As demand for sliced veneer has

been increasingly marginalised in mainstream markets,

demand is now focusing more on higher value niche

markets -including high end interior fittings, yachts, and

the car industry - which generate more value but absorb

lower volumes.

Related News:

|