|

Report

from

Europe

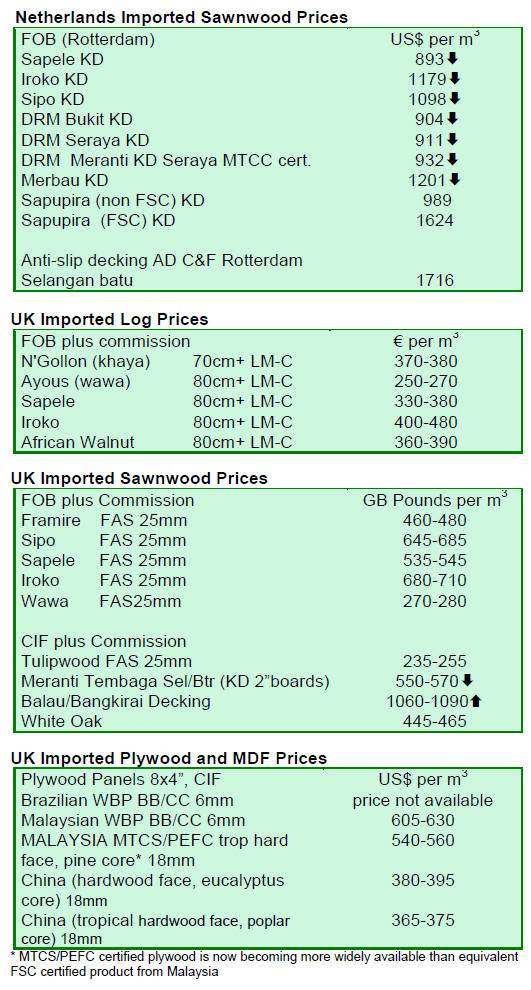

Slow buying of bangkarai decking in Europe

According to the latest issue of EUWID, the Germanybased

wood trade journal , central European importers

were holding relatively high stocks of bangkirai decking at

the end of the 2011 summer season and have therefore

been off-loading these at below replacement value.

This situation has arisen partly due to shipment delays

which led to significant volumes of bangkirai decking

scheduled for June arrival not reaching Europe until

October or even early November. Economic uncertainty

combined with the existing surplus has dampened interest

in new orders for the 2012 season.

EUWID also reports that CIF euro prices for Malaysian

meranti window scantlings have been rising throughout

2011 and are now 20-25% higher than the start of the year.

This is due to the rise in the dollar value against the euro

combined with limited supplies of roundwood in South

East Asia. Prices are now at such a level that European

manufacturers are actively looking for substitutes.

On the other hand, according to EUWID, the supply

situation is less tense for meranti lumber with currently

available supplies still higher than existing weak demand.

Falling freight rates and slightly lower FOB US$ prices

offered by Malaysian exporters have helped to offset the

impact of the weakening euro to keep CIF euro prices

relatively level for European importers.

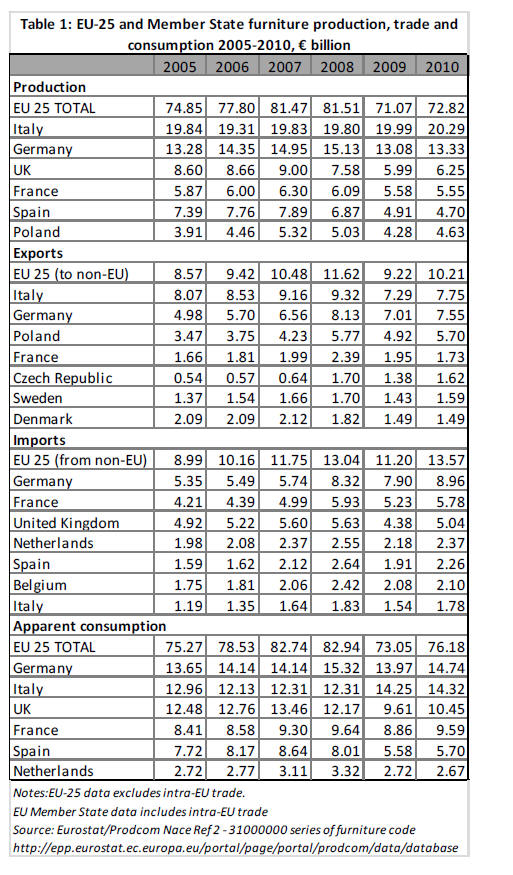

European furniture consumption weakening in 2011

after rising in 2010

Last year, the value of EU furniture consumption

increased 4% to €76.2 billion, supporting a 2% increase in

production and a 21% increase in imports from countries

outside the EU. However signs are that furniture

consumption is slipping back again during 2011 as

economic uncertainty has mounted.

European manufacturers and brands continue to dominate

the European furniture market. Last year, European

furniture production was valued at €72.82 billion and

domestic manufacturers accounted for well over 80% of

the value of products supplied to the EU.

This partly reflects strong consumer loyalty to European

brands in some EU countries, combined with strong

technical, design and marketing skills, particularly

prominent in the major German and Italian furniture

sectors. Together these two countries account for nearly

half of all furniture produced in the EU.

Another factor limiting market opportunities for furniture

suppliers outside the EU is fragmentation of retailing

activities in many European countries. This greatly

complicates the process of identifying buyers and

marketing products.

Domestic furniture manufacturers also benefit from their

natural proximity to consumers, a factor which, if

anything, has become more significant in these times of

tight stock control and just-in-time trading.

Proximity to the customer is particularly important in

Europe’s large contract furniture sector involving supply

of bespoke products and services, mainly to the hospitality

sector (hotels, restaurants and bars) but also to the office,

health, education, airport, and marine sectors.

The contract sector accounts for a very significant share of

all furniture demand in most European countries. In the

UK for example the contract sector is believed to account

for 30% of furniture sales.

Despite these obstacles, the value of furniture imports into

the EU from outside the region increased by 21% last year

to reach €13.57 billion, with particularly strong growth in

imports from China, Vietnam, Indonesia, and Malaysia.

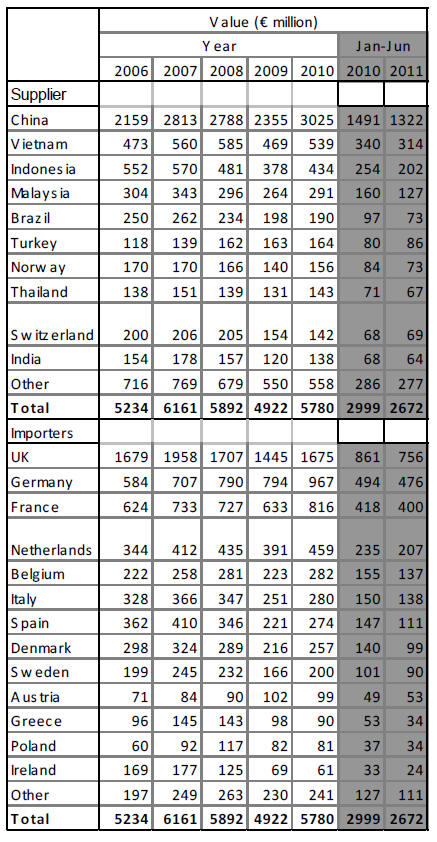

EU imports of wood furniture rebounded strongly in 2010

The following table provides more detailed information on

recent trends in EU imports of wood furniture from

outside the region.

It highlights that after the significant decline in the value

of imports in 2009, imports of wood furniture rebounded

strongly by 17% in 2010 to reach nearly €5.8 billion.

EU wood furniture imports rose strongly last year from

China (+28%), Vietnam (+15%), Indonesia (+15%),

Malaysia (+10%), Thailand (+10%) and India (+15%).

This strong rebound in imports was evident in all the

major EU consuming countries including the UK,

Germany, France, Netherlands, Belgium, Italy and Spain.

EU 25 Furniture Imports.

However, as austerity has begun to bite and other signs of

economic strain have emerged in Europe during 2011, EU

imports of wood furniture have weakened again in 2011.

In the first 6 months of the year, the value of imports fell

by 11%.

Imports were down from all the major supply countries

including China (-11%), Vietnam (-8%), Indonesia (-

20%), Malaysia (-21%) and Brazil (-24%). As with the

upturn, the downturn has been almost universal across all

EU Member States.

Unfortunately the trade data does not allow for any

reliable separation of furniture into exterior and interior

products. In the past, tropical countries have dominated

markets for weather-resistant exterior furniture products,

while temperate countries have dominated markets for

interior furniture products where diversity of look and

grain is more important.

This simple division has been breaking down rapidly.

Tropical countries like Vietnam, Indonesia and Malaysia

have increasingly diversified into interior furniture

products. This trend has been driven by a combination of

tightening supply and rising prices for tropical hardwoods

and the competitiveness of South East Asian countries

able to draw on relatively low labour costs and traditional

wood-working skills.

Originally, most interior products supplied to Europe by

South East Asian countries were based on local plantation

timbers, notably rubberwood. However, these countries

are now importing increasing volumes of temperate

hardwoods, from both Europe and the United States, for

manufacture and re-export of interior furniture.

Product innovation increases pressure on tropical

hardwood garden furniture

The growing expense and rarity of good quality tropical

hardwoods suitable for exterior furniture, combined with

the environmental concerns of European retailers and

innovations in other material sectors, has meant tropical

hardwoods have continued to lose share in the European

garden furniture sector.

This is well illustrated by a recent report on new trends in

European garden furniture contained in the latest issue of

World Furniture published by CSIL, the Italian furniture

research organisation

(http://www.worldfurnitureonline.com/).

There is no mention of tropical hardwood in the report

which instead focuses heavily on new High Density

Polyethylene (HDPE) fibres which allow manufacturers to

design furniture suitable for all weather use. This synthetic

rattan is typically woven onto a lightweight metal

structural frame and is available in a multitude of colours

and weaving patterns.

The article claims that HDPE is non-toxic and recyclable

and that it also offers high Grey Scale ratings (low rate of

colour loss due to weather exposure).

The article also highlights the development of new

products based on “recycled and recyclable” materials, for

example combining hemp fibre, specially treated against

UV radiation, with stainless steel tubing which is

“electrolytically polished” to remove surface ferrous

particles and ensure increased resistance to atmospheric

corrosion.

These products may be designed to ensure that all

components can be fully disassembled, thus simplifying

the recycling process and helping to reduce the

environmental impact.

While it may be little consolation to wood producers,

many of these products supplied into Europe are also now

manufactured in South East Asia.

Large retailers increasingly dominate the UK furniture sector

The latest edition of CSIL’s World Furniture magazine

provides commentary on other key trends impacting on

Europe’s furniture sector. A special article on the UK

furniture retailing sector highlights that major structural

changes are underway.

While the UK imports large volumes of furniture from

Germany, Italy and Poland, relatively high levels of

consolidation in the retail sector has been a major factor

behind the UK’s emergence as by far the largest importer

of furniture from countries outside the EU, particularly

China but also including Vietnam, Indonesia and

Malaysia.

World Furniture reports that UK imports from Germany

and Italy have generally been declining in recent years,

while imports from China, South East Asia and Poland

have tended to rise.

According to World Furniture, the UK market remains

tough with little or no growth this year. 2011 has seen

some significant bankruptcies in the furniture retailing

sector.

In May 2011, the Focus DIY group, with 178 stores and a

turnover of €524 million has been the largest retail

bankruptcy in the UK this year. It was closely followed in

June by national furniture retailer Habitat which operated

a network of 30 stores around the country.

Most recently, the Homeform Group has also gone into

administration, and is trying to sell its Moben and Dolphin

brands in an effort to save its Sharps and Kitchens Direct

businesses.

The structure of the UK furniture sector is now shifting,

says World Furniture. Smaller independent furniture

retailers have suffered the most during the recession, while

larger retailers have continued to increase their

dominance.

This includes department stores led by Home Retail

Group, Marks & Spencer and The John Lewis Partnership,

furniture retailer chains like IKEA and Furniture Village,

together with kitchen specialists like Magnet, Harvey

Jones and Moben, and upholstery specialists like DFS and

Reid Furniture. Buying groups are also becoming

increasingly important in the market.

Large DIY retailers like B&Q and Wickes, more

concentrated now following the collapse of Focus, are also

playing a more important role in the market, particularly at

the bottom end and in the garden furniture segment.

However, according to World Furniture, the fastest

growing segment is mail order business, much of which is

controlled by existing dominant retailer brands through

their new direct sales divisions.

German furniture demand remains buoyant

The latest edition of World Furniture also highlights that

Germany has been one of the few bright spots in Europe’s

furniture sector this year. Furniture production is expected

to be up 5% overall in Germany this year, with particularly

large increases in office furniture production (+22.8%) and

shop fitting (14.9%).

Most other sectors are forecast to record production

growth of between 4% and 6% this year, with only the

upholstered furniture sector giving any cause for concern.

German import and export flows are also expected to

remain positive for 2011 as a whole.

Interaction between European and Chinese furniture sectors

Today, no review of the furniture sector in any part of the

world would be complete without mentioning China. An

interesting dynamic is emerging between China, the

world’s largest furniture producer and exporter, and

Europe which still plays host to the world’s largest and

most innovative furniture design community and most

desirable furniture brands.

In the early days of China’s efforts to penetrate the

European furniture sector, manufacturers were seemingly

content to focus on a volume-driven rather than a productand-

design-driven industrial strategy.

The early emphasis was on contract manufacturing,

mainly at the lower end of the market, rather than on ownbrand

furniture manufacturing. However, there has been

growing recognition amongst Chinese manufacturers that

this will lead to progressive loss of competitiveness as the

barriers to entry in contract manufacturing are relatively

low and there will always be opportunities for

manufacturers in lower-cost locations to take market

share.

Therefore, as labour and other costs in China have been

gradually rising, the future growth of the Chinese furniture

industry is closely tied to its penetration of the middle

range. According to World Furniture, this is now

beginning to happen.

Many of China’s leading firms (Kuka for upholstered

furniture, Matsu for office furniture, Oppein for kitchens)

today use a combination of Chinese, Asian and European

designers for their own production. They are also

introducing first class technologies into all the major

furniture districts.

Another factor affecting the dynamic between European

and Chinese firms is the beginnings of a “reversal in

trade”. No longer is it just about Chinese furniture firms

increasing penetration of the European market. It is also

about European firms taking a share of the potentially vast

opportunities emerging in China’s domestic market.

The recent appreciation of the Remimbi (from a rate of 10

to the Euro, to the current 8.5) is beginning to make

Chinese exports more difficult and imports more

accessible. Rising income and emergence of a new middle

class of consumers means that China is becoming more

interesting for European furniture players.

According to World Furniture, German and Italian

producers of high-quality brand-name furniture are

becoming more engaged in selling to China. They now

face the difficult choice between exporting to China and

producing locally.

Some firms have failed in their attempt to produce locally

(e.g. Decoro) or have chosen to sell to third parties

(Faram). Others have been more successful, for example

Natuzzi has become one the best-selling brands in China,

while Colombini which specialises in children’s furniture

now has almost 100 sales outlets in China.

Russia to accede to the WTO in 2012

The World Trade Organization finalised terms for Russia's

membership in early November, which should enable it to

gain final approval from WTO trade ministers at a meeting

in December and to join the body early next year.

To gain admittance, Russia had to bring its own laws into

line with WTO rules and satisfy the 153 existing members

that it is committed to enforcing WTO standards.

The accession agreement states that the tariff ceiling for

imports of wood and paper products into Russia will be

reduced from the current level of 13.4% to 8%. In the

long term, this is expected to provide new opportunities

for suppliers in other countries to develop sales in Russia.

However, a more immediate and dramatic effect of WTO

accession may be to liberalise Russia’s log exports. Russia

was formerly a key source of raw logs, mainly softwood,

to the international market.

This changed when Russia increased its wood export

duties in 2006 from 2.5 euros ($3.3) per cubic meter,

reaching 15 euros in 2008.

Russia’s log exports fell from 51.1 million m3 in 2006 to

only 21.4 million m3 in 2010. Following Russia’s

accession to WTO, export tariffs are expected to be

progressively cut on birch and aspen logs by 75% and on

spruce and pine logs by 50%.

In the European market, this move is expected to have a

particularly dramatic effect on log supply to the pulp and

paper sector in Scandinavia. Scandinavian companies

imported around 12.3 million cubic meters of Russian logs

in 2008, but with imposition of the export tariffs these

imports halved the following year and stood at 7.3 million

cubic meters in 2010.

This had a particularly profound effect on the Finnish

industry which subsequently announced closures of 10

paper and pulp mills and reduced overall production by

nearly a fifth in 2007-10.

Russia's accession to the WTO will open the door once

again to EU log imports from Russia. However, due to the

closure of some Scandinavian mills previously dependent

on the supply, and the development of alternative sourcing

strategies by remaining mills, there is little expectation

that European imports will ever return to previous levels.

Related News:

|