|

Report

from

Europe

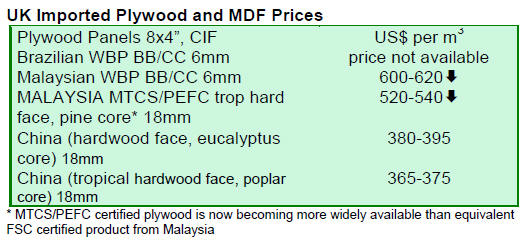

Challenging European market for tropical hardwood plywood

The European market for tropical hardwood plywood

faces numerous challenges. Prices for existing landed

stocks are under downward pressure as consumption is

slow in the winter season and, with the European

economic situation so fragile, few importers are expecting

a significant rise in sales next year.

However, rising production costs in SE Asia mean that

shippers either have to raise prices �C currently very

difficult in an unreceptive market - or to cut costs. Many

are choosing the latter course and this risks compromising

on quality.

Chinese manufacturers have been the major beneficiaries

of these trends. Their ability to offer low prices, combined

with the willingness of many importers to buy on price not

quality, has meant that China has continued to gain market

share in Europe this year.

European importers unconcerned about impact of

Chinese New Year on supplies as landed stocks are

adequate

Despite the anticipated slowing in supply of plywood from

mid-January during the Chinese New Year, orders for

Chinese hardwood plywood from China by European

buyers remain subdued.

Consumption of existing European inventories of this

commodity remains slow. With availability in China good

and relatively short turnaround times for new orders,

European importers seem little concerned about any

potential shortfall in supply.

According to Timber Trades Journal (TTJ), the UK��s

timber industry magazine, the sale of assets of UK-based

RKL Plywood which recently went into administration,

has led to increased availability of Chinese plywood on the

UK market.

This has further dampened prices on the ground in Europe

at a time when other issues of limited raw material supply

and rising production costs argue in favour of increased

prices.

With Chinese exporters also wanting to reduce

inventories, some are offering discounted prices in the

hope of stimulating sales. However there has been no

reduction in production costs in China.

FOB prices of better quality Chinese plywood have

remained stable or even tended to rise to accommodate

increased costs of labour and raw material in China.

This rise is being offset in the European market by

continuing decline in container freight rates from China.

Rates for a 40ft container on the China-Europe route have

fallen from around US$2000 in May this year to close to

US$1000 today.

Serious quality issues emerge in UK plywood market

According to the TTJ, quality issues are now emerging as

a very serious concern in the UK plywood market. One

UK plywood industry expert alleges that around 80% of

all Chinese plywood currently in the UK is ��MR with

dyed red glue to look like WBP��, with a large proportion

being ��under-thickness�� but marked as full thickness.

Furthermore, says the TTJ, a significant percentage of

Chinese plywood supplied to the UK is CE marked and

yet a number of suppliers ��appear not having their

plywood performance-tested on a regular basis to confirm

the structural performance��. If these allegations are true,

the long-term repercussions for the reputation of Chinese

hardwood plywood in the UK could be very severe.

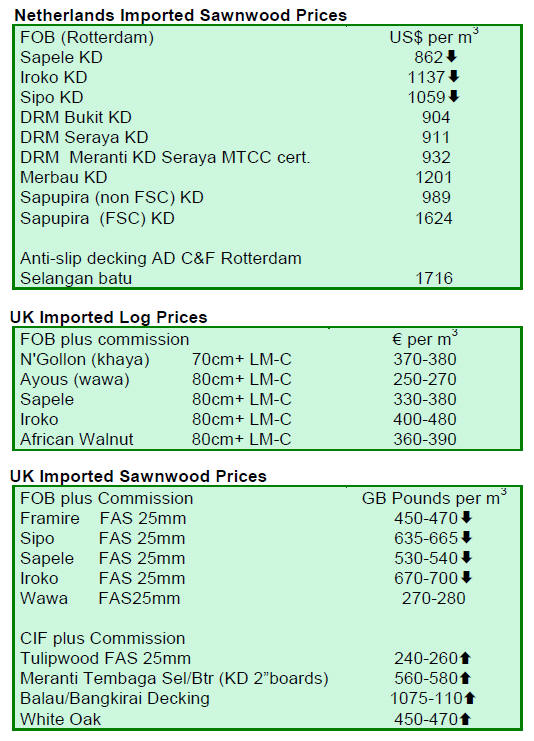

Slow sales of SE Asian plywood in Europe

Sales of Malaysian plywood in the European market have

remained slow in recent weeks. In the UK, Malaysia has

generally been losing share to Chinese products during

2011. Prices for Malaysian BB/CC WBP plywood,

composed of tropical hardwood throughout are currently

in the region of Indo96 +30%.

Significantly cheaper prices are available, although as with

Chinese plywood, compromises have been made on

quality. With price expectations now so low in Europe,

more Malaysian manufacturers have followed the Chinese

route of offering combi-plywood composed of a tropical

hardwood face and a poplar core.

Prices for the best quality Indonesian BB/CC WPB

plywood on offer in Europe have declined slightly from

levels achieved a couple of months ago, but are still

significantly higher than those for Malaysian plywood,

exceeding Indo96 +40%.

Very little Brazilian hardwood plywood is now imported

into Europe. Brazilian suppliers are generally unable to

compete with Malaysian plywood at the higher end and

against Chinese plywood at the low quality end of the

market.

Meanwhile European imports of plywood manufactured

from eucalyptus plantations in South America, while still

quite small, are rising following recent investments by

Weyerhauser in Uruguay.

EU and Vietnam move towards agreement on illegal wood trade

A report from Vietnamnet.vn suggests that Vietnam and

the EU have entered the final negotiation stage towards a

bilateral agreement to minimize the risk of illegal wood

trade between the two trading partners.

The so-called FLEGT Voluntary Partnership Agreement

(VPA) may be implemented prior to March 3, 2013, the

date when the EU Timber Regulation (EUTR) is due to

take effect.

Under the EUTR, all European importers will be obliged

to implement due diligence systems to minimize the risk

of any wood being derived from an illegal source.

They will also be liable to prosecution if found in

possession of wood extracted or traded in contravention of

the laws of any country.

However according to EUTR, any timber or timber

product licensed under the terms of a VPA �C such as that

likely to be agreed with Vietnam �C will be automatically

recognized as legal in the EU market. European importers

will be under no obligation to seek further safeguards

(such as certification) to demonstrate the legal origin of

VPA Licensed timber.

Vietnam and the EU successfully completed the second

negotiation round of the VPA agreement in early

December. The agreement is particularly significant for

the Vietnamese furniture manufacturing sector which is a

major supplier to the EU. In 2010, EU imports of wood

furniture from Vietnam had a total value €539 million.

Vietnam is currently the second largest external supplier

of wood furniture to the EU after China.

According to vietnamnet.vn, some Vietnamese furniture

manufacturers remain unconvinced about the benefits of a

FLEGT VPA, believing that the additional costs of VPA

Licensing will undermine competitiveness. However,

others are gradually coming round to the idea that the

FLEGT VPA process may be less of a trade barrier and

more of an opportunity to gain greater share of the

European market.

Related News:

|