By Madison's Lumber Reporter

Drama unfolded large in downtown Vancouver last week, where the Union of British Columbia Municipalities annual meeting was being held. Mayors and political leaders from across the province were greeted by a convoy of 230 unloaded logging trucks arriving Friday morning to large crowds of surprised, and cheering, onlookers. The issue of reduced timber supply is hitting rural areas especially hard, so log truck operators decided to make a statement directly in the faces of decision-makers. At the same time, the BC Ministry of Forests, Lands, Natural Resource Operations and Rural Development released the “State of British Columbia Forests 2018,” which provides full data update for the harvest, manufacture, and export of B.C. wood fibre resource: Economic State of B.C.’s Forest Sector 2018

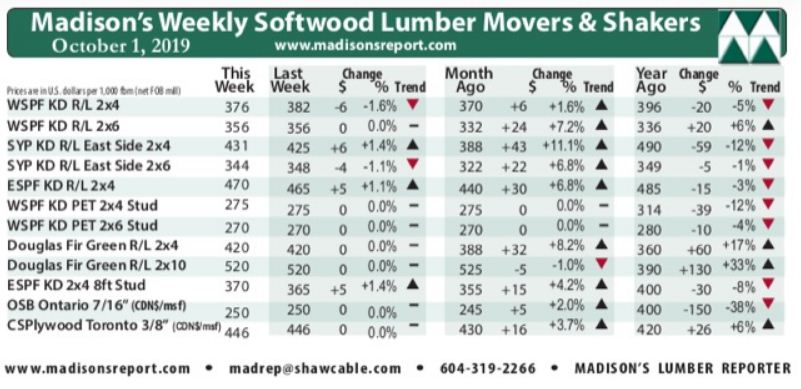

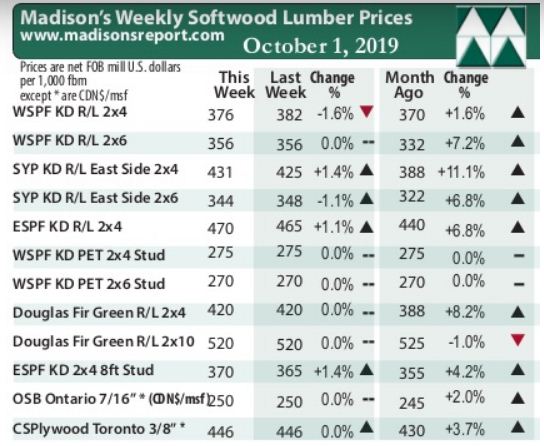

Lumber prices moderated down slightly on some construction framing items, but stayed flat on most solid wood commodities. Producers of lumber price benchmark item Western Spruce-Pine-Fir KD 2×4 #2&Btr, lowered their asking prices by six dollars to U.S. $376 mfbm. Canadian WSPF producers adamantly refused to take any more counter-offers on any item. Oct. 14 order files prevailed on nearly everything, with at least one sawmill mentioning a notable lack of 2×8 supply, saying they hadn’t had any all week. Wet weather continued to prevent a few sawmills in British Columbia and Alberta from getting enough logs, so much so that another facility was down for at least a week. Keep reading to find out more:

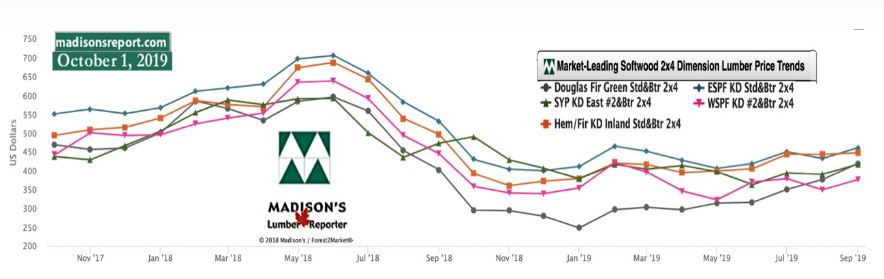

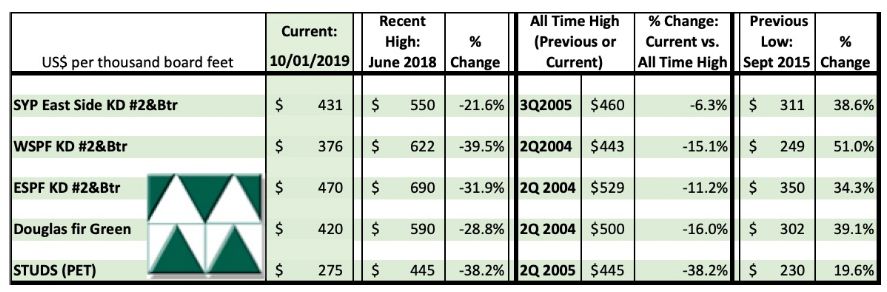

After increasing by six dollars the previous week, this week’s benchmark lumber commodity Western Spruce-Pine-Fir KD 2×4 #2&Btr price was U.S. $376 mfbm, down -$6, or -1.5%. This might be an indication that the latest sawmill curtailments have taken enough production offline to bring the supply-demand balance to an even keel. This price is up six dollars from one month ago, when it was U.S. $382 mfbm. Further narrowing the gap from 2018, compared to one year ago this price is down -$20, or -5%.

Drama unfolded large in downtown Vancouver last week, where the Union of British Columbia Municipalities annual meeting was being held. Mayors and political leaders from across the province were greeted by a convoy of 230 unloaded logging trucks arriving Friday morning to large crowds of surprised, and cheering, onlookers. The issue of reduced timber supply is hitting rural areas especially hard, so log truck operators decided to make a statement directly in the faces of decision-makers. At the same time, the BC Ministry of Forests, Lands, Natural Resource Operations and Rural Development released the “State of British Columbia Forests 2018,” which provides full data update for the harvest, manufacture, and export of B.C. wood fibre resource: Economic State of B.C.’s Forest Sector 2018

Lumber prices moderated down slightly on some construction framing items, but stayed flat on most solid wood commodities. Producers of lumber price benchmark item Western Spruce-Pine-Fir KD 2×4 #2&Btr, lowered their asking prices by six dollars to U.S. $376 mfbm. Canadian WSPF producers adamantly refused to take any more counter-offers on any item. Oct. 14 order files prevailed on nearly everything, with at least one sawmill mentioning a notable lack of 2×8 supply, saying they hadn’t had any all week. Wet weather continued to prevent a few sawmills in British Columbia and Alberta from getting enough logs, so much so that another facility was down for at least a week. Keep reading to find out more:

After increasing by six dollars the previous week, this week’s benchmark lumber commodity Western Spruce-Pine-Fir KD 2×4 #2&Btr price was U.S. $376 mfbm, down -$6, or -1.5%. This might be an indication that the latest sawmill curtailments have taken enough production offline to bring the supply-demand balance to an even keel. This price is up six dollars from one month ago, when it was U.S. $382 mfbm. Further narrowing the gap from 2018, compared to one year ago this price is down -$20, or -5%.