By Madison's Lumber Reporter

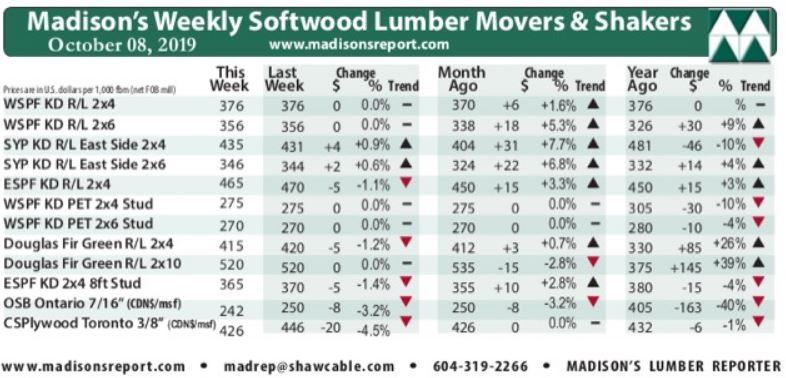

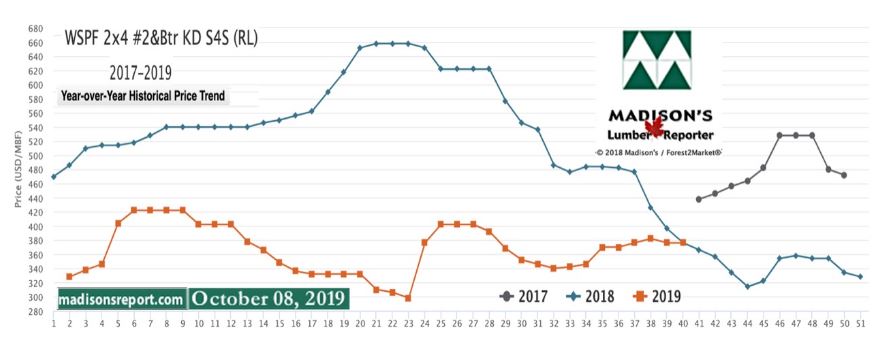

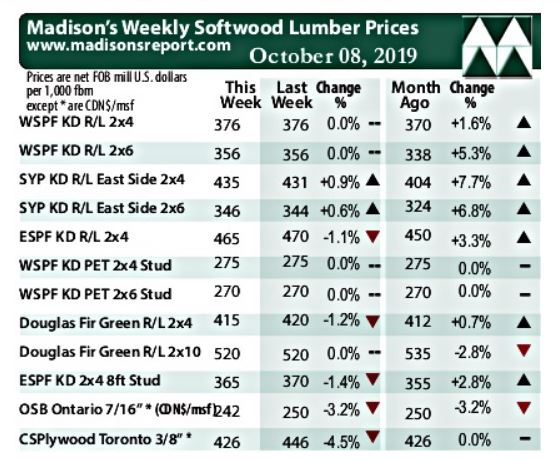

Most North American construction framing dimension softwood lumber commodities last week achieved price levels seen at this time in 2017, while benchmark item Western Spruce-Pine-Fir KD 2×4 #2&btr price now matches this week last year. After soaring to record-level highs during the 2018 U.S. home building season, softwood lumber prices slid inexorably downward well into this summer. The stringent and painful sawmill closures and curtailments during this year have done well to keep a healthy supply-demand balance. While customers are somewhat reluctant, ongoing weekly purchases are allowing Canadian and US sawmills to prop up prices. As U.S. Thanksgiving approaches — the usual slow-down for U.S. housing construction — demand will lessen into year-end.

Benchmark item Western Spruce-Pine-Fir KD 2×4 #2&Btr stayed flat last week, at U.S. $376 mfbm. Last week’s price is +$6, or +1.6%, more than it was one month ago. Compared to one year ago, this price is unchanged. Canadian producers of WSPF lumber noted that buyers were pretty quiet last week. Sawmills turned their attention to receiving incoming log loads and fulfilling their own previously-made sales. Sales volumes were adequate for most of last week, but were “nothing to write home about.” Log inventories at western Canadian sawmills were lower than optimal. While construction activity was apparently hale and hearty in many U.S. regions, buyers in the mountain states were winding down their inventories in advance of approaching inclement weather. Keep reading to find out more:

Most North American construction framing dimension softwood lumber commodities last week achieved price levels seen at this time in 2017, while benchmark item Western Spruce-Pine-Fir KD 2×4 #2&btr price now matches this week last year. After soaring to record-level highs during the 2018 U.S. home building season, softwood lumber prices slid inexorably downward well into this summer. The stringent and painful sawmill closures and curtailments during this year have done well to keep a healthy supply-demand balance. While customers are somewhat reluctant, ongoing weekly purchases are allowing Canadian and US sawmills to prop up prices. As U.S. Thanksgiving approaches — the usual slow-down for U.S. housing construction — demand will lessen into year-end.

Benchmark item Western Spruce-Pine-Fir KD 2×4 #2&Btr stayed flat last week, at U.S. $376 mfbm. Last week’s price is +$6, or +1.6%, more than it was one month ago. Compared to one year ago, this price is unchanged. Canadian producers of WSPF lumber noted that buyers were pretty quiet last week. Sawmills turned their attention to receiving incoming log loads and fulfilling their own previously-made sales. Sales volumes were adequate for most of last week, but were “nothing to write home about.” Log inventories at western Canadian sawmills were lower than optimal. While construction activity was apparently hale and hearty in many U.S. regions, buyers in the mountain states were winding down their inventories in advance of approaching inclement weather. Keep reading to find out more: