By Madison's Lumber Reporter

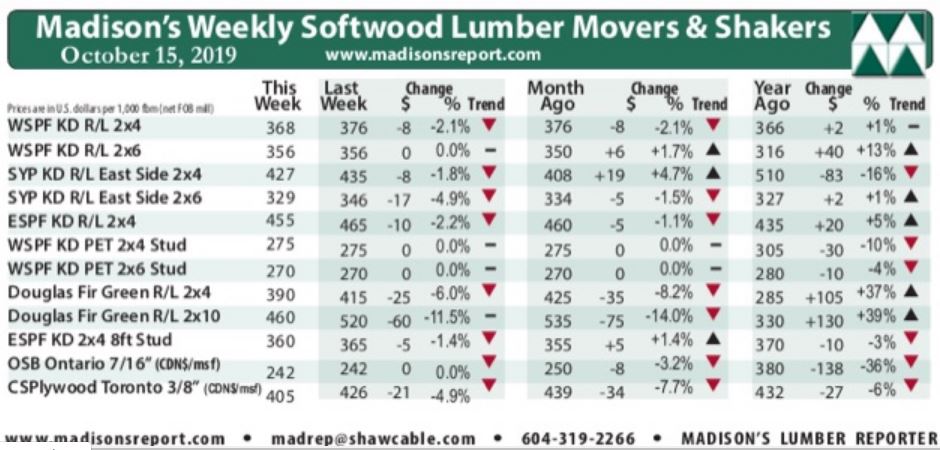

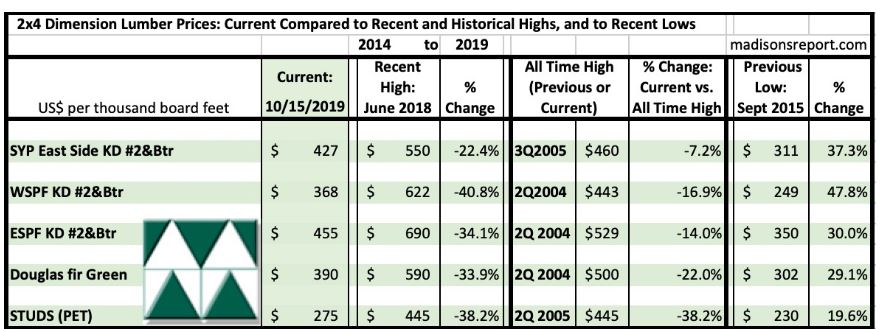

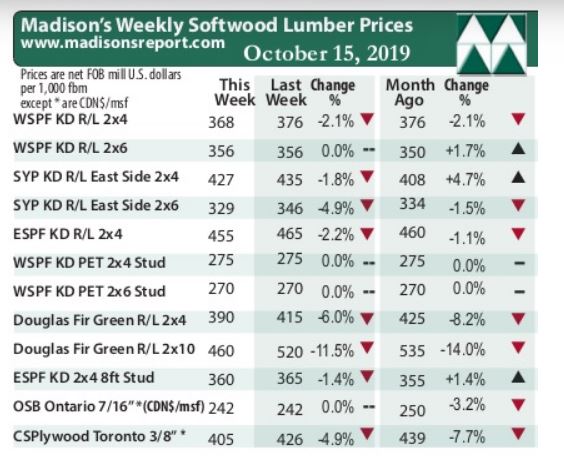

The price of benchmark construction framing dimension softwood lumber commodity Western Spruce-Pine-Fir KD 2×4 #2&Btr dropped another -$8 last week as customer reluctance to buy won over supplier stubbornness to keep prices higher. For their part, many specialty items like Douglas fir green, studs in Eastern Canada, and plywood dropped significantly as players were better able to assess the supply-demand balance. Having just been celebrated in Canada, the U.S. Thanksgiving long weekend looms into view. This date usually marks the beginning of real slow-down of construction activity in the U.S., thus is often the time of year when lumber prices are lowest. Of course, that depends on the severity and location of storms — and, for this year anyway — wildfires in California.

This week the annual North American Wholesale Lumbermen’s Association (NAWLA) will be held in San Antonio, Tex. Madison’s intrepid lumber market analyst, Earl Heath, will be there! Do look out for Madison’s at the sessions, networking, and on the trade show floor…we are always looking for more sources at the sawmills and for the latest scoop on lumber trading activity. Keep reading to find out more:

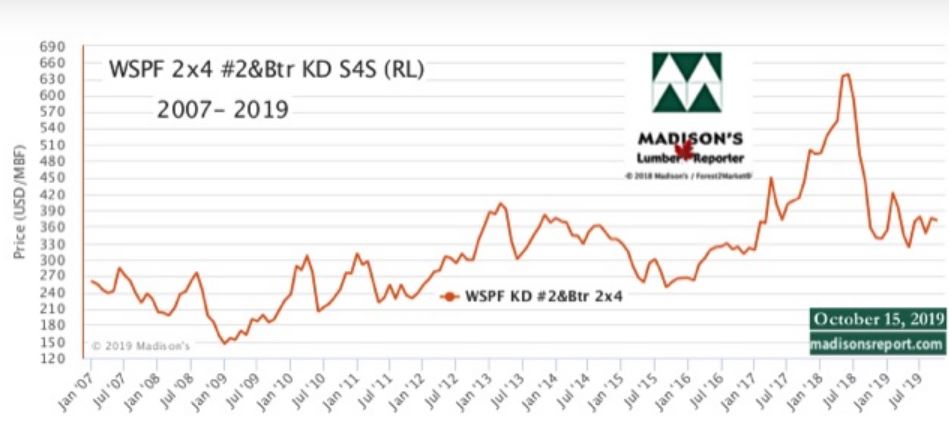

Last week Western Spruce-Pine-Fir KD 2×4 #2&Btr lost -$8, or -2%, to close at U.S. $368 mfbm. Last week’s price is also -$8 less than it was one month ago. Compared to one year ago, this price is up +$2.

The price of benchmark construction framing dimension softwood lumber commodity Western Spruce-Pine-Fir KD 2×4 #2&Btr dropped another -$8 last week as customer reluctance to buy won over supplier stubbornness to keep prices higher. For their part, many specialty items like Douglas fir green, studs in Eastern Canada, and plywood dropped significantly as players were better able to assess the supply-demand balance. Having just been celebrated in Canada, the U.S. Thanksgiving long weekend looms into view. This date usually marks the beginning of real slow-down of construction activity in the U.S., thus is often the time of year when lumber prices are lowest. Of course, that depends on the severity and location of storms — and, for this year anyway — wildfires in California.

This week the annual North American Wholesale Lumbermen’s Association (NAWLA) will be held in San Antonio, Tex. Madison’s intrepid lumber market analyst, Earl Heath, will be there! Do look out for Madison’s at the sessions, networking, and on the trade show floor…we are always looking for more sources at the sawmills and for the latest scoop on lumber trading activity. Keep reading to find out more:

Last week Western Spruce-Pine-Fir KD 2×4 #2&Btr lost -$8, or -2%, to close at U.S. $368 mfbm. Last week’s price is also -$8 less than it was one month ago. Compared to one year ago, this price is up +$2.