By Madison's Lumber Reporter

Dec. 10 is the deadline for retirement of two of the three remaining Appellate Judges at the World Trade Organization, where there are currently disputes revolving around North American softwood lumber. This WTO appellate panel, which usually has seven people, now only has the legal minimum of three, until Dec. 10. Following years of pent-up U.S. frustration over the behaviour of the WTO’s ultimate dispute-resolution body, the administration of President Donald Trump began blocking the appointment of new panellists. As a result, the group’s appellate body will stop functioning next month, plunging into uncertainty and casting a cloud over future ones.

The uncertainty stemming from the panel’s dissolution would touch every country with business before the WTO, including Canada.

Experts recently gathered at an event in Washington, D.C. where they discussed the consequences of the WTO becoming paralyzed.

Construction framing dimension softwood lumber prices in Canada and the U.S., meanwhile, stabilized last week to levels moderate when compared to one-year and two-years ago price levels. The latest U.S. housing starts and home sales data, out last week, showed continued strong building activity with this important customer for North American softwood lumber.

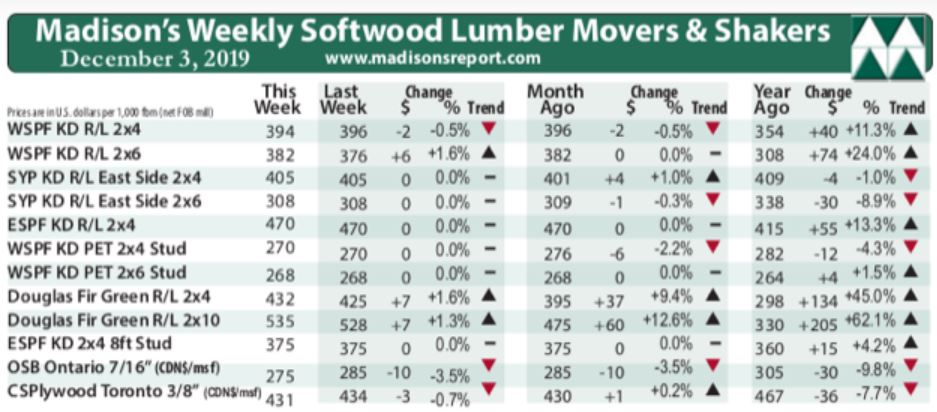

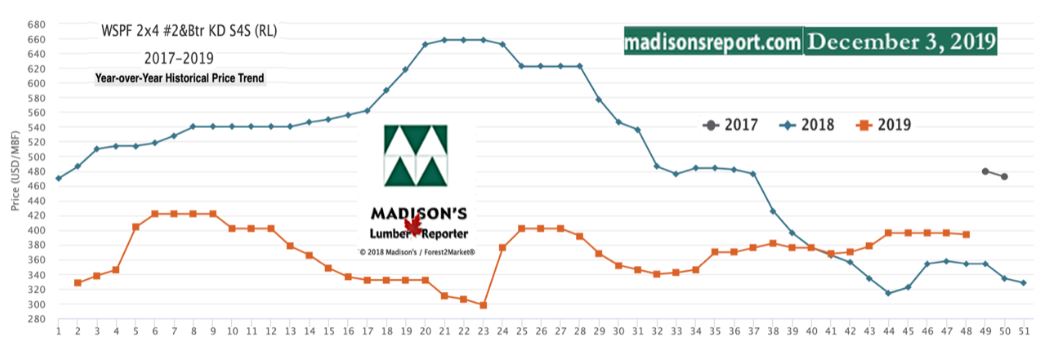

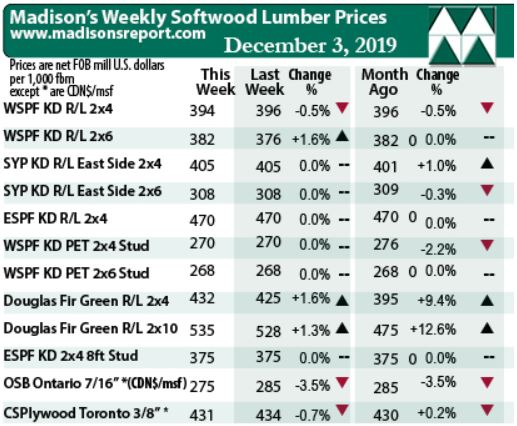

The price of benchmark lumber commodity Western Spruce-Pine-Fir KD 2×4 #2&Btr last week dropped -$2 to close Friday at US$394 mfbm (net FOB sawmill; cash price, or “print”). Recovering from drops in autumn, last week’s price is also -$2 less than it was one month ago. Continuing to gain ground after severe lows, compared to one year ago this price is up +$40 or +11%.

Dec. 10 is the deadline for retirement of two of the three remaining Appellate Judges at the World Trade Organization, where there are currently disputes revolving around North American softwood lumber. This WTO appellate panel, which usually has seven people, now only has the legal minimum of three, until Dec. 10. Following years of pent-up U.S. frustration over the behaviour of the WTO’s ultimate dispute-resolution body, the administration of President Donald Trump began blocking the appointment of new panellists. As a result, the group’s appellate body will stop functioning next month, plunging into uncertainty and casting a cloud over future ones.

The uncertainty stemming from the panel’s dissolution would touch every country with business before the WTO, including Canada.

Experts recently gathered at an event in Washington, D.C. where they discussed the consequences of the WTO becoming paralyzed.

Construction framing dimension softwood lumber prices in Canada and the U.S., meanwhile, stabilized last week to levels moderate when compared to one-year and two-years ago price levels. The latest U.S. housing starts and home sales data, out last week, showed continued strong building activity with this important customer for North American softwood lumber.

The price of benchmark lumber commodity Western Spruce-Pine-Fir KD 2×4 #2&Btr last week dropped -$2 to close Friday at US$394 mfbm (net FOB sawmill; cash price, or “print”). Recovering from drops in autumn, last week’s price is also -$2 less than it was one month ago. Continuing to gain ground after severe lows, compared to one year ago this price is up +$40 or +11%.