By Madison's Lumber Reporter

It was not a surprise to Madison’s Lumber

Reporter this morning when the latest U.S.

housing starts data showed continued

improvement. Such a strong end to what turned

out to be a pretty good year for North American

construction framing dimension softwood lumber

prices — after a terrifying start — bodes well

for 2020. This Friday will be the last update

for the year, and Madison’s is advising that

lumber sales will start out hot right at the

beginning of January 2020. At this moment,

Canadian and U.S. sawmills are reporting they

are holding off booking new sales until January,

just to maintain current price levels. If the

customer tries to counter-offer at a lower

price, they are quoted for January delivery.

U.S. housing starts data encouraging upward trend continues, which

admittedly surprised many analysts, beyond 3Q this year. Builders,

realtors, banks, and other experts noted last month that if U.S.

homebuilding activity improved again for November, that would carry

through to next year. Given the brutal end to last year and horrifying

drops in lumber prices to 1Q 2019, lumber producers have maintained

caution and not built up lumber inventory. Log supplies across the

continent, however, are literally bursting. This is the very best

combination for a sawmill’s year-end: lumber yard empty, log yard

jammed.

For their part, similarly, reloads, wholesalers, and secondary suppliers

have also not been building lumber inventory. Players remain cautious,

especially given the massive amount of sawmill closures over this year.

Sentiment among customers that prices might go down stubbornly persists.

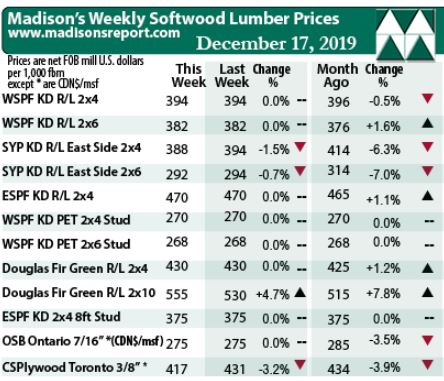

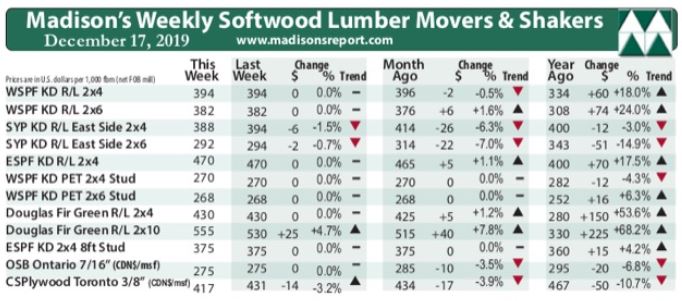

The price of benchmark lumber commodity Western Spruce-Pine-Fir KD 2×4

#2&Btr last week was unchanged from the week before, still at U.S. $394

mfbm (net FOB sawmill; cash price, or “print”). This price is -$2 less

than it was one month ago. Compared to one year ago, this price is up

+$60, or +18%.

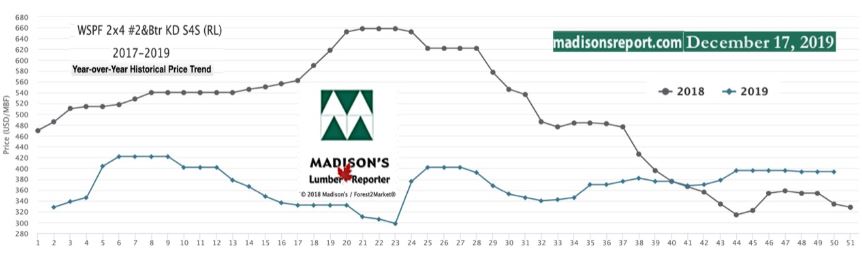

Compared to historical trends, last week’s WSPF 2×4 #2&Btr price

continued rising, up by another +$25, or +7%, relative to the one-year

rolling average price of U.S. $369 mfbm, and is down -$43, or -10%,

relative to the two-year rolling average price of U.S. $438 mfbm. Last

week’s price is up +$20, or +5% relative to the five-year rolling

average price of U.S. $374 mfbm.

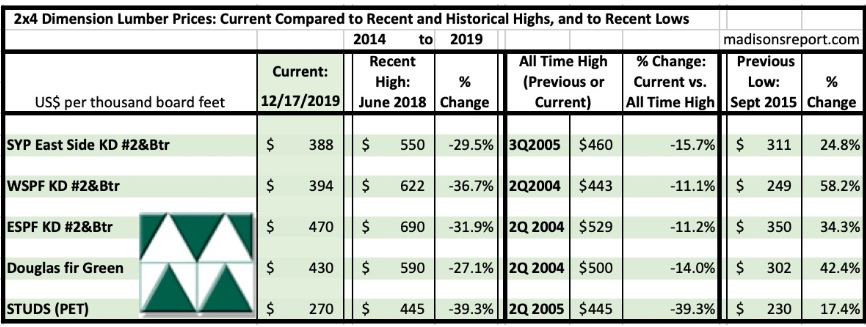

The below table is a comparison of recent highs, in June 2018, and

current Dec. 2019 benchmark dimension softwood lumber 2×4 prices

compared to historical highs of 2004/05 and compared to recent lows of

Sept. 2015:

Related News:

-

U.S. &

Canada softwood and panel markets - week 49, 2019 (December

3,

2019)

-

U.S. &

Canada softwood and panel markets - week 48, 2019 (December

3,

2019)

-

U.S. &

Canada softwood and panel markets - week 47, 2019 (November

26,

2019)

-

U.S. &

Canada softwood and panel markets - week 46, 2019 (November

19,

2019)

-

U.S. &

Canada softwood and panel markets - week 45, 2019 (November

12,

2019)

-

U.S. &

Canada softwood and panel markets - week 44, 2019 (November

5,

2019)

-

U.S. &

Canada softwood and panel markets - week 43, 2019 ( October

29,

2019)

-

U.S. &

Canada softwood and panel markets - week 42, 2019 ( October

22,

2019)

-

U.S. &

Canada softwood and panel markets - week 41, 2019 ( October

15,

2019)

-

U.S. &

Canada softwood and panel markets - week 40, 2019 ( October

8,

2019)

-

U.S. &

Canada softwood and panel markets - week 39, 2019 ( October

1,

2019)

-

U.S. &

Canada softwood and panel markets - week 38, 2019 ( September 24,

2019)

-

U.S. softwood and panel markets - week 37, 2019 ( September 17,

2019)

-

U.S. softwood and panel markets - week 36, 2019 ( September 10,

2019)

-

U.S. softwood and panel markets - week 35, 2019 ( September 3,

2019)

-

U.S. softwood and panel markets - week 34, 2019 ( August 23,

2019)

-

U.S. softwood and panel markets - week 33, 2019 ( August 16,

2019)

-

U.S. softwood and panel markets - week 32, 2019 ( August 09,

2019)

-

U.S. softwood and panel markets - week 31, 2019 ( August 02,

2019)

-

U.S. softwood and panel markets - week 30, 2019 ( July

26, 2019)

-

U.S. softwood and panel markets - week 29, 2019 ( July 19,

2019)

-

U.S. softwood and panel markets - week 28, 2019 ( July 12,

2019)

-

U.S. softwood and panel markets - week 27, 2019 ( July 03,

2019)

-

U.S. softwood and panel markets - week 26, 2019 ( June 28,

2019)

-

U.S. softwood and panel markets - week 25, 2019 ( June 21,

2019)

-

U.S. softwood and panel markets - week 24, 2019 ( June 14,

2019)

-

U.S. softwood and panel markets - week 23, 2019 ( June 07,

2019)

-

U.S. softwood and panel markets - week 22, 2019 ( May 31,

2019)

-

U.S. softwood and panel markets - week 21, 2019 ( May 24,

2019)

-

U.S. softwood and panel markets - week 20, 2019 ( May 17,

2019)

-

U.S. softwood and panel markets - week 19, 2019 ( May 10,

2019)

-

U.S. softwood and panel markets - week 18, 2019 ( May 03,

2019)

-

U.S. softwood and panel markets - week 17, 2019 ( April 26,

2019)

-

U.S. softwood and panel markets - week 16, 2019 ( April 19,

2019)

-

U.S. softwood and panel markets - week 15, 2019 ( April 12,

2019)

-

U.S. softwood and panel markets - week 14, 2019 ( April 05,

2019)

-

U.S. softwood and panel markets - week 13, 2019 ( March

29, 2019)

-

U.S. softwood and panel markets - week 12, 2019 ( March

22, 2019)

-

U.S. softwood and panel markets - week 11, 2019 ( March

15, 2019)

-

U.S. softwood and panel markets - week 10, 2019 ( March

08, 2019)

-

U.S. softwood and panel markets - week 9, 2019 ( March

01, 2019)

-

U.S. softwood and panel markets - week 8, 2019 ( February.

22, 2019)

-

U.S. softwood and panel markets - week 7, 2019 ( February.

15, 2019)

-

U.S. softwood and panel markets - week 6, 2019 ( February.

08, 2019)

-

U.S. softwood and panel markets - week 5, 2019 ( February.

01, 2019)

-

U.S. softwood and panel markets - week 4, 2019 (January. 25,

2019)

-

U.S. softwood and panel markets - week 3, 2019 (January. 18,

2019)

-

U.S. softwood and panel markets - week 2, 2019 (January. 11,

2019)

-

U.S. softwood and panel markets - week 1, 2019 (January. 04,

2019)

|