By Madison's Lumber Reporter

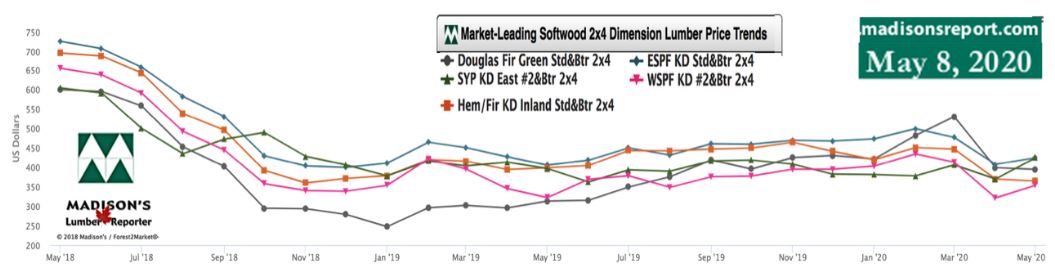

North American construction framing dimension

softwood lumber prices last week improved

greatly over those one-month-ago, even

surpassing what prices were in May 2019.

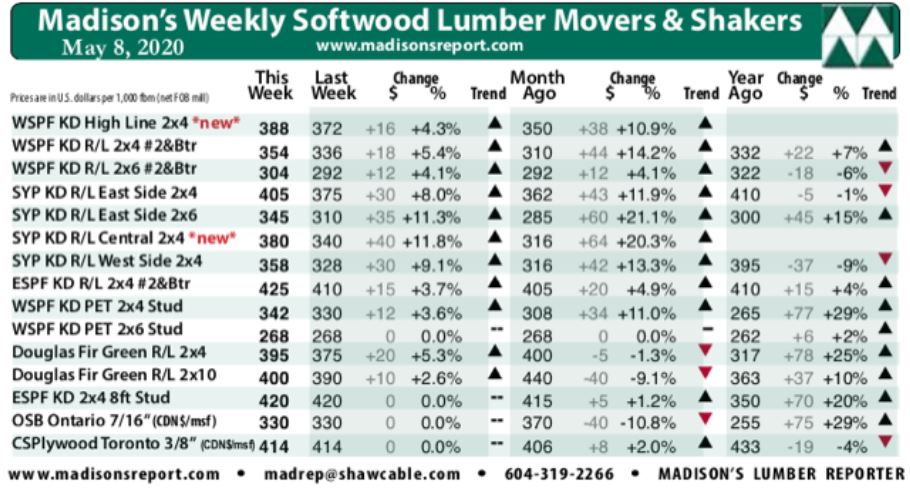

The wholesaler price of benchmark softwood

lumber commodity item Western Spruce-Pine-Fir KD

2×4 #2&Btr (RL) last week was US$354 mfbm (net

FOB sawmill), catapulting up +$22, or almost +7

per cent, compared to the same week in 2019.

Suppliers of Western SPF commodities in the

United States were cautiously optimistic to

start the month of May. Both primary and

secondary suppliers reported a positive tone to

the market. Producers extended the bulk of their

sawmill order files into late-May. Sales

activity of most commodities was solid, with 2×6

#2&Btr R/L the only item lagging behind slightly

in demand early in the week.

Rebounding completely from the lows of April,

for the week ending May 8, 2020, Western SPF 2×4

price was up +$26, or +8.4 per cent, from one

month ago when it was US$310 mfbm. Compared to

one year ago, this price is up +$22, or almost

+7 per cent.

"Demand for softwood lumber came from everywhere. Buyers in

Canada and the US urgently tried to replenish their sparse inventories,

while consistent orders for both #2&Btr and low grade came from China."

— Madison’s Lumber Reporter.

In Eastern Canada, sales activity took a couple days to get going again

last week, as producers were reluctant to sell far out on the limited

production volumes which became available. Due to throttled supply,

finding exact tallies among depleted sawmill inventories to cover

immediate needs was difficult. Buyers were forced to search around for

incomplete orders to furnish their own scant inventories. For Eastern

stocking wholesalers on the shores of New Jersey, the beginning of May

didn’t look much different than the gloom of April. As sawmill prices

advanced, vendors did their best to turn a profit on the limited

business they could find, but most ended up losing money on virtually

every transaction.

"Curtailed sawmills eased their order files

into the first week of June on most items, as buyers lamented scant

availability of both dimension and stud commodities." — Madison’s Lumber

Reporter

Continuing to make gains, last week’s Western S-P-F 2×4 price was down

-$21, or almost -6 per cent, relative to the 1-year rolling average

price of US$375 mfbm and was down -$56, or -14 per cent relative to the

2-year rolling average price of US$410 mfbm.

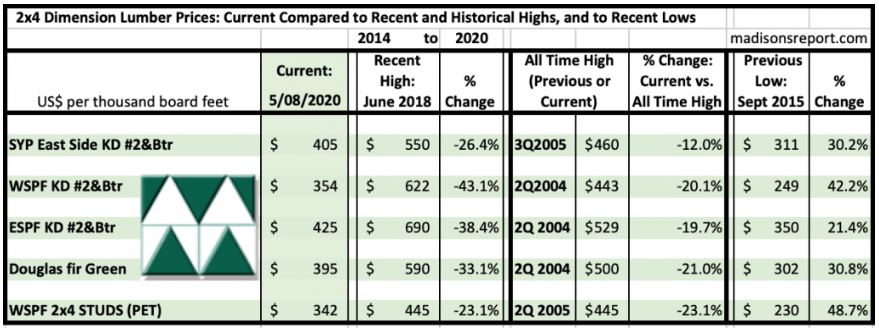

The below table is a comparison of recent highs, in June 2018, and

current May 2020 benchmark dimension softwood lumber 2×4 prices compared

to historical highs of 2004/05 and compared to recent lows of Sept 2015:

Related News:

-

U.S. &

Canada softwood and panel markets - week 17, 2020 (May 8,

2020)

-

U.S. &

Canada softwood and panel markets - week 16, 2020 (May 1,

2020)

-

U.S. &

Canada softwood and panel markets - week 15, 2020 (Apr

23,

2020)

-

U.S. &

Canada softwood and panel markets - week 14, 2020 (Apr

17,

2020)

-

U.S. &

Canada softwood and panel markets - week 13, 2020 (Apr

08,

2020)

-

U.S. &

Canada softwood and panel markets - week 12, 2020 (Mar

31,

2020)

-

U.S. &

Canada softwood and panel markets - week 11, 2020 (Mar

24,

2020)

-

U.S. &

Canada softwood and panel markets - week 5, 2020 (Feb

11,

2020)

-

U.S. &

Canada softwood and panel markets - week 4, 2020 (Feb

4,

2020)

-

U.S. &

Canada softwood and panel markets - week 3, 2020 (January

27,

2020)

-

U.S. &

Canada softwood and panel markets - week 2, 2020 (January

20,

2020)

-

U.S. &

Canada softwood and panel markets - week 1, 2020 (January

13,

2020)

-

U.S. &

Canada softwood and panel markets - week 50, 2019 (December

17,

2019)

-

U.S. &

Canada softwood and panel markets - week 49, 2019 (December

10,

2019)

-

U.S. &

Canada softwood and panel markets - week 48, 2019 (December

3,

2019)

-

U.S. &

Canada softwood and panel markets - week 47, 2019 (November

26,

2019)

-

U.S. &

Canada softwood and panel markets - week 46, 2019 (November

19,

2019)

-

U.S. &

Canada softwood and panel markets - week 45, 2019 (November

12,

2019)

-

U.S. &

Canada softwood and panel markets - week 44, 2019 (November

5,

2019)

-

U.S. &

Canada softwood and panel markets - week 43, 2019 ( October

29,

2019)

-

U.S. &

Canada softwood and panel markets - week 42, 2019 ( October

22,

2019)

-

U.S. &

Canada softwood and panel markets - week 41, 2019 ( October

15,

2019)

-

U.S. &

Canada softwood and panel markets - week 40, 2019 ( October

8,

2019)

-

U.S. &

Canada softwood and panel markets - week 39, 2019 ( October

1,

2019)

-

U.S. &

Canada softwood and panel markets - week 38, 2019 ( September 24,

2019)

-

U.S. softwood and panel markets - week 37, 2019 ( September 17,

2019)

-

U.S. softwood and panel markets - week 36, 2019 ( September 10,

2019)

-

U.S. softwood and panel markets - week 35, 2019 ( September 3,

2019)

-

U.S. softwood and panel markets - week 34, 2019 ( August 23,

2019)

-

U.S. softwood and panel markets - week 33, 2019 ( August 16,

2019)

-

U.S. softwood and panel markets - week 32, 2019 ( August 09,

2019)

-

U.S. softwood and panel markets - week 31, 2019 ( August 02,

2019)

-

U.S. softwood and panel markets - week 30, 2019 ( July

26, 2019)

-

U.S. softwood and panel markets - week 29, 2019 ( July 19,

2019)

-

U.S. softwood and panel markets - week 28, 2019 ( July 12,

2019)

-

U.S. softwood and panel markets - week 27, 2019 ( July 03,

2019)

-

U.S. softwood and panel markets - week 26, 2019 ( June 28,

2019)

-

U.S. softwood and panel markets - week 25, 2019 ( June 21,

2019)

-

U.S. softwood and panel markets - week 24, 2019 ( June 14,

2019)

-

U.S. softwood and panel markets - week 23, 2019 ( June 07,

2019)

-

U.S. softwood and panel markets - week 22, 2019 ( May 31,

2019)

-

U.S. softwood and panel markets - week 21, 2019 ( May 24,

2019)

-

U.S. softwood and panel markets - week 20, 2019 ( May 17,

2019)

-

U.S. softwood and panel markets - week 19, 2019 ( May 10,

2019)

-

U.S. softwood and panel markets - week 18, 2019 ( May 03,

2019)

-

U.S. softwood and panel markets - week 17, 2019 ( April 26,

2019)

-

U.S. softwood and panel markets - week 16, 2019 ( April 19,

2019)

-

U.S. softwood and panel markets - week 15, 2019 ( April 12,

2019)

-

U.S. softwood and panel markets - week 14, 2019 ( April 05,

2019)

-

U.S. softwood and panel markets - week 13, 2019 ( March

29, 2019)

-

U.S. softwood and panel markets - week 12, 2019 ( March

22, 2019)

-

U.S. softwood and panel markets - week 11, 2019 ( March

15, 2019)

-

U.S. softwood and panel markets - week 10, 2019 ( March

08, 2019)

-

U.S. softwood and panel markets - week 9, 2019 ( March

01, 2019)

-

U.S. softwood and panel markets - week 8, 2019 ( February.

22, 2019)

-

U.S. softwood and panel markets - week 7, 2019 ( February.

15, 2019)

-

U.S. softwood and panel markets - week 6, 2019 ( February.

08, 2019)

-

U.S. softwood and panel markets - week 5, 2019 ( February.

01, 2019)

-

U.S. softwood and panel markets - week 4, 2019 (January. 25,

2019)

-

U.S. softwood and panel markets - week 3, 2019 (January. 18,

2019)

-

U.S. softwood and panel markets - week 2, 2019 (January. 11,

2019)

-

U.S. softwood and panel markets - week 1, 2019 (January. 04,

2019)

|