By Madison's Lumber Reporter

After a wild ride down then up over the

past few months, most standard construction

framing dimension softwood lumber prices

stabilized last week, to levels both producers

and customers are comfortable with. Inventories

remain spotty as sawmill production is still

constrained and buyers continue to look for

highly specified loads only.

Purveyors of Western Spruce-Pine-Fir commodities

in the United States described last week as

similar to the previous one as most customers

had their near-term needs covered and continued

to be careful in their dealings. Players

reported good consumption levels in Western and

Southwestern states.

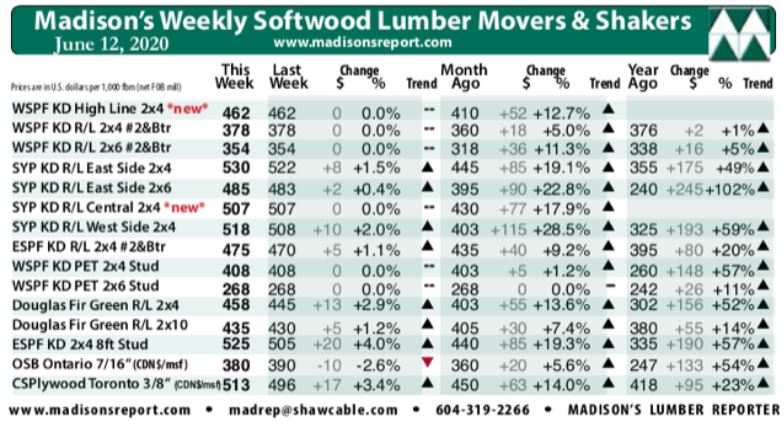

The largest producers of Western SPF in Canada

noted that business came in fits and starts last

week. Around midweek a large block of 2×4 R/L

#2&Btr was snapped up with alacrity, but the

remainder of the week was more focused on

digestion, as field inventories weren’t as

depleted as usual. Order files were now into the

week of July third on most items, with sawmills

running two- to three-weeks late on existing

orders.

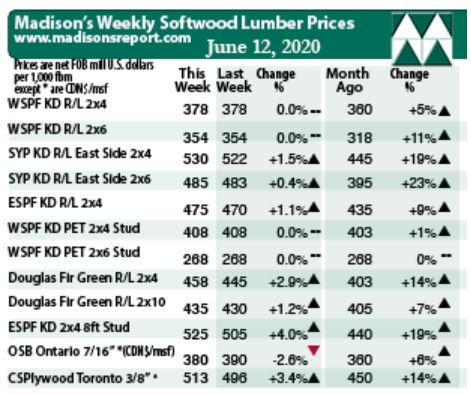

For the week ending June 12, 2020, prices of

most standard construction framing dimension

softwood lumber items remained flat, with

benchmark item WSPF 2×4 #2&Btr KD still at US378

mfbm, as the week before. The price for this

benchmark lumber commodity was up +$18, or plus

five per cent from one month ago. Compared to

the same week in 2019 when it was US$376, this

price is up +$2, or plus one per cent.

“Caution ruled every lumber sales deal last week, and demand from

Eastern regions was again more active than in the West.” — Madison’s

Lumber Reporter

In the East, it was a sporadic week for lumber traders, with spurts of

sales activity one moment and torpidity the next. Prices of most Eastern

SPF widths and trims continued to appreciate however 2×8 had been in

particularly short supply for some time and climbed the most, rising

+$20 to $425 mfbm in the Toronto market and +$25 to $520 in the Great

Lakes market. Last week started on a strong note as a large contingent

of worried buyers jumped in at the same time, before sales activity

comparatively quieted from Tuesday to Friday.

On the US Eastern Seaboard, the chaotic state of Northeastern US wood

markets persisted last week according to Eastern stocking wholesalers.

Everyone had come in hard with purchases over the previous two weeks,

thus sales activity had reached a fever pitch and vendors hoarded wood.

So last week the market was badly oversold. Meanwhile customers were

calling incessantly, screaming for their expected deliveries.

“Players reported good consumption levels in Western and

Southwestern states, whereas many Midwestern and Northeastern areas were

still catching up with demand by comparison. Sales volumes of dimension

items remained steady.” — Madison’s Lumber Reporter

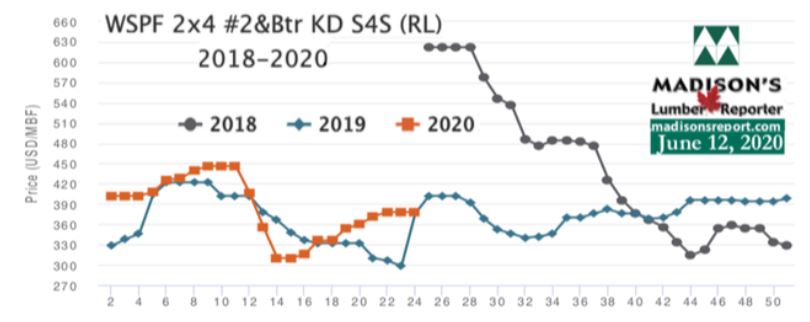

Dropping slightly from one year ago, last week’s Western S-P-F 2×4 price

fell -$3, or negative one per cent, relative to the one year rolling

average price of US$381 mfbm and was down -$19, or negative five per

cent, relative to the two year rolling average price of US$397 mfbm.

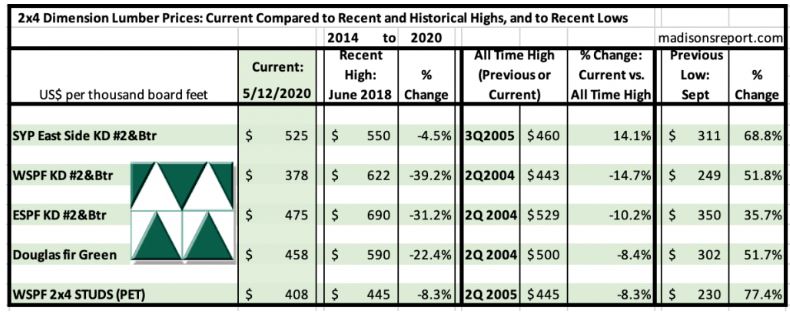

The below table is a comparison of recent highs, in June 2018, and

current June 2020 benchmark dimension softwood lumber 2×4 prices

compared to historical highs of 2004/05 and compared to recent lows of

Sept 2015:

Related News:

-

U.S. &

Canada softwood and panel markets - week 22, 2020 (Jun

10,

2020)

-

U.S. &

Canada softwood and panel markets - week 21, 2020 (Jun

3,

2020)

-

U.S. &

Canada softwood and panel markets - week 20, 2020 (May 27,

2020)

-

U.S. &

Canada softwood and panel markets - week 19, 2020 (May 21,

2020)

-

U.S. &

Canada softwood and panel markets - week 18, 2020 (May 15,

2020)

-

U.S. &

Canada softwood and panel markets - week 17, 2020 (May 8,

2020)

-

U.S. &

Canada softwood and panel markets - week 16, 2020 (May 1,

2020)

-

U.S. &

Canada softwood and panel markets - week 15, 2020 (Apr

23,

2020)

-

U.S. &

Canada softwood and panel markets - week 14, 2020 (Apr

17,

2020)

-

U.S. &

Canada softwood and panel markets - week 13, 2020 (Apr

08,

2020)

-

U.S. &

Canada softwood and panel markets - week 12, 2020 (Mar

31,

2020)

-

U.S. &

Canada softwood and panel markets - week 11, 2020 (Mar

24,

2020)

-

U.S. &

Canada softwood and panel markets - week 5, 2020 (Feb

11,

2020)

-

U.S. &

Canada softwood and panel markets - week 4, 2020 (Feb

4,

2020)

-

U.S. &

Canada softwood and panel markets - week 3, 2020 (January

27,

2020)

-

U.S. &

Canada softwood and panel markets - week 2, 2020 (January

20,

2020)

-

U.S. &

Canada softwood and panel markets - week 1, 2020 (January

13,

2020)

-

U.S. &

Canada softwood and panel markets - week 50, 2019 (December

17,

2019)

-

U.S. &

Canada softwood and panel markets - week 49, 2019 (December

10,

2019)

-

U.S. &

Canada softwood and panel markets - week 48, 2019 (December

3,

2019)

-

U.S. &

Canada softwood and panel markets - week 47, 2019 (November

26,

2019)

-

U.S. &

Canada softwood and panel markets - week 46, 2019 (November

19,

2019)

-

U.S. &

Canada softwood and panel markets - week 45, 2019 (November

12,

2019)

-

U.S. &

Canada softwood and panel markets - week 44, 2019 (November

5,

2019)

-

U.S. &

Canada softwood and panel markets - week 43, 2019 ( October

29,

2019)

-

U.S. &

Canada softwood and panel markets - week 42, 2019 ( October

22,

2019)

-

U.S. &

Canada softwood and panel markets - week 41, 2019 ( October

15,

2019)

-

U.S. &

Canada softwood and panel markets - week 40, 2019 ( October

8,

2019)

-

U.S. &

Canada softwood and panel markets - week 39, 2019 ( October

1,

2019)

-

U.S. &

Canada softwood and panel markets - week 38, 2019 ( September 24,

2019)

-

U.S. softwood and panel markets - week 37, 2019 ( September 17,

2019)

-

U.S. softwood and panel markets - week 36, 2019 ( September 10,

2019)

-

U.S. softwood and panel markets - week 35, 2019 ( September 3,

2019)

-

U.S. softwood and panel markets - week 34, 2019 ( August 23,

2019)

-

U.S. softwood and panel markets - week 33, 2019 ( August 16,

2019)

-

U.S. softwood and panel markets - week 32, 2019 ( August 09,

2019)

-

U.S. softwood and panel markets - week 31, 2019 ( August 02,

2019)

-

U.S. softwood and panel markets - week 30, 2019 ( July

26, 2019)

-

U.S. softwood and panel markets - week 29, 2019 ( July 19,

2019)

-

U.S. softwood and panel markets - week 28, 2019 ( July 12,

2019)

-

U.S. softwood and panel markets - week 27, 2019 ( July 03,

2019)

-

U.S. softwood and panel markets - week 26, 2019 ( June 28,

2019)

-

U.S. softwood and panel markets - week 25, 2019 ( June 21,

2019)

-

U.S. softwood and panel markets - week 24, 2019 ( June 14,

2019)

-

U.S. softwood and panel markets - week 23, 2019 ( June 07,

2019)

-

U.S. softwood and panel markets - week 22, 2019 ( May 31,

2019)

-

U.S. softwood and panel markets - week 21, 2019 ( May 24,

2019)

-

U.S. softwood and panel markets - week 20, 2019 ( May 17,

2019)

-

U.S. softwood and panel markets - week 19, 2019 ( May 10,

2019)

-

U.S. softwood and panel markets - week 18, 2019 ( May 03,

2019)

-

U.S. softwood and panel markets - week 17, 2019 ( April 26,

2019)

-

U.S. softwood and panel markets - week 16, 2019 ( April 19,

2019)

-

U.S. softwood and panel markets - week 15, 2019 ( April 12,

2019)

-

U.S. softwood and panel markets - week 14, 2019 ( April 05,

2019)

-

U.S. softwood and panel markets - week 13, 2019 ( March

29, 2019)

-

U.S. softwood and panel markets - week 12, 2019 ( March

22, 2019)

-

U.S. softwood and panel markets - week 11, 2019 ( March

15, 2019)

-

U.S. softwood and panel markets - week 10, 2019 ( March

08, 2019)

-

U.S. softwood and panel markets - week 9, 2019 ( March

01, 2019)

-

U.S. softwood and panel markets - week 8, 2019 ( February.

22, 2019)

-

U.S. softwood and panel markets - week 7, 2019 ( February.

15, 2019)

-

U.S. softwood and panel markets - week 6, 2019 ( February.

08, 2019)

-

U.S. softwood and panel markets - week 5, 2019 ( February.

01, 2019)

-

U.S. softwood and panel markets - week 4, 2019 (January. 25,

2019)

-

U.S. softwood and panel markets - week 3, 2019 (January. 18,

2019)

-

U.S. softwood and panel markets - week 2, 2019 (January. 11,

2019)

-

U.S. softwood and panel markets - week 1, 2019 (January. 04,

2019)

|