By Madison's Lumber Reporter

While demand for construction framing dimension

softwood lumber continued to surpass supply last

week, it was noticeable that buyer orders to

sawmills were slowing down. Indeed, customer

interest seemed to shift from the benchmark

Western Spruce-Pine-Fir to the East Side, as

prices of Eastern Spruce-Pine-Fir increased by

more than that of Western.

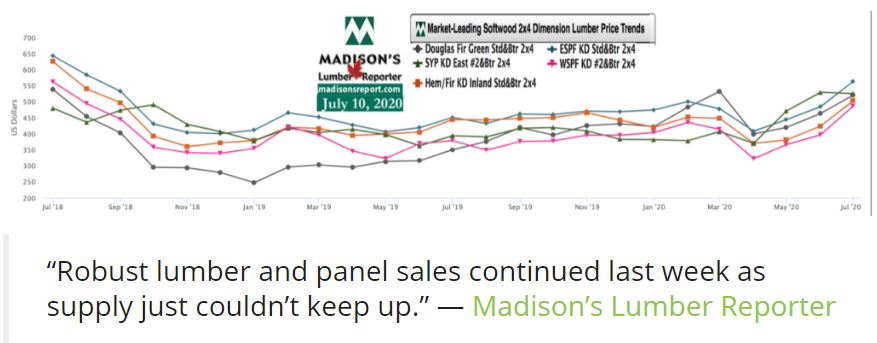

Demand for plywood, meanwhile, was unabated for

reconstruction following social unrest about

racial inequality.

Western S-P-F producers in the US reported another stellar week during

which they wished they had more material to cover unceasing inquiry from

buyers. Retailers were frustrated with late shipments but were also

aware that little could be done about pandemic-caused shortages of

transportation equipment and labour.

large producer was sold out before 8:00am, leaving the US wholesale

market wanting. Sawmill order files were at least four weeks out on all

dimension lumber items.

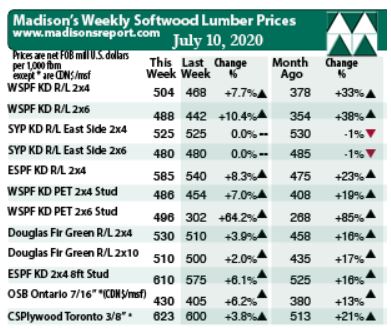

For the week ending July 10, 2020, prices of standard construction

framing dimension softwood lumber items continued sharp increases. In

particular, benchmark lumber item Western S-P-F 2×4 #2&Btr KD rose

further, up by +36, or +8 per cent, to US$504 mfbm, from US$468 the

previous week. The price for this lumber commodity was up +$126, or +33

per cent, from one month ago. Compared to the same week in 2019 this

price is up +$112, or +29 per cent.

“Sellers of Eastern S-P-F in the US reported increasing cases of

substitution; as customers desperately snatching any wood they could

find regardless of species or designation.” — Madison’s Lumber Reporter

Purveyors of Eastern S-P-F dimension lumber and studs had another tricky

week, with prices again all over the place. Sawmills were tentative

about getting their wares to market as they didn’t want to leave

potential money on the table. Construction activity remained strong on

both sides of the border and many contractors were unable to find wood

materials’ coverage for current and upcoming building jobs.

Recovering well compared to last year but still far behind mid-2018,

last week’s Western S-P-F 2×4 price improved +$85, or +22 per cent,

relative to the one-year rolling average price of US$383 mfbm and

increased +$77, or +20 per cent, relative to the two-year rolling

average price of US$391 mfbm.

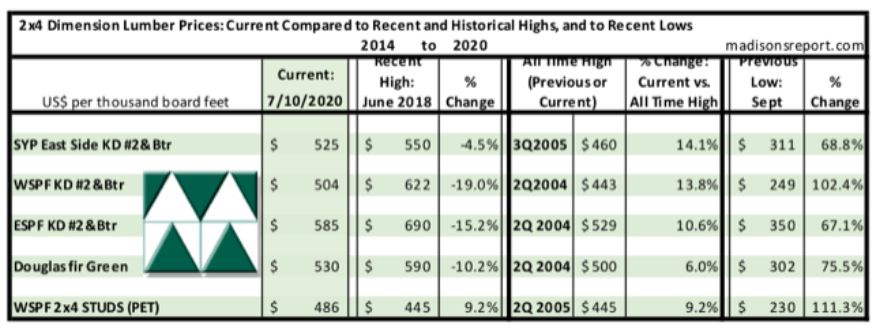

The below table is a comparison of recent highs, in June 2018, and

current July 2020 benchmark dimension softwood lumber 2×4 prices

compared to historical highs of 2004-2005 and compared to recent lows of

Sept. 2015:

As in the West, Eastern S-P-F suppliers noted that buyers had gotten

used to not worrying about asking prices and instead were focussed on

the simple concept of availability. Players couldn’t think of a

commodity that wasn’t rabidly sought after, and any scrap of leftover

inventory held by a sawmill or wholesaler was jumped on with alacrity.

Lumber producer order files pushed into the back half of August as the

acute shortage of wood stirred up desperation among buyers.

Still making big jumps and catching up to recent-record highs of

mid-2018, last week’s Western S-P-F 2×4 price improved +$119, or +31 per

cent, relative to the one-year rolling average price of US$385 mfbm and

increased +$114, or +29 per cent, relative to the two-year rolling

average price of US$390 mfbm.

Related News:

-

U.S. & Canada softwood and panel markets - week 26, 2020 (Jul

10,

2020)

-

U.S. & Canada softwood and panel markets - week 25, 2020 (Jul

02,

2020)

-

U.S. & Canada softwood and panel markets - week 24, 2020 (Jun

25,

2020)

-

U.S. & Canada softwood and panel markets - week 23, 2020 (Jun

17,

2020)

-

U.S. &

Canada softwood and panel markets - week 22, 2020 (Jun

10,

2020)

-

U.S. &

Canada softwood and panel markets - week 21, 2020 (Jun

3,

2020)

-

U.S. &

Canada softwood and panel markets - week 20, 2020 (May 27,

2020)

-

U.S. &

Canada softwood and panel markets - week 19, 2020 (May 21,

2020)

-

U.S. &

Canada softwood and panel markets - week 18, 2020 (May 15,

2020)

-

U.S. &

Canada softwood and panel markets - week 17, 2020 (May 8,

2020)

-

U.S. &

Canada softwood and panel markets - week 16, 2020 (May 1,

2020)

-

U.S. &

Canada softwood and panel markets - week 15, 2020 (Apr

23,

2020)

-

U.S. &

Canada softwood and panel markets - week 14, 2020 (Apr

17,

2020)

-

U.S. &

Canada softwood and panel markets - week 13, 2020 (Apr

08,

2020)

-

U.S. &

Canada softwood and panel markets - week 12, 2020 (Mar

31,

2020)

-

U.S. &

Canada softwood and panel markets - week 11, 2020 (Mar

24,

2020)

-

U.S. &

Canada softwood and panel markets - week 5, 2020 (Feb

11,

2020)

-

U.S. &

Canada softwood and panel markets - week 4, 2020 (Feb

4,

2020)

-

U.S. &

Canada softwood and panel markets - week 3, 2020 (January

27,

2020)

-

U.S. &

Canada softwood and panel markets - week 2, 2020 (January

20,

2020)

-

U.S. &

Canada softwood and panel markets - week 1, 2020 (January

13,

2020)

-

U.S. &

Canada softwood and panel markets - week 50, 2019 (December

17,

2019)

-

U.S. &

Canada softwood and panel markets - week 49, 2019 (December

10,

2019)

-

U.S. &

Canada softwood and panel markets - week 48, 2019 (December

3,

2019)

-

U.S. &

Canada softwood and panel markets - week 47, 2019 (November

26,

2019)

-

U.S. &

Canada softwood and panel markets - week 46, 2019 (November

19,

2019)

-

U.S. &

Canada softwood and panel markets - week 45, 2019 (November

12,

2019)

-

U.S. &

Canada softwood and panel markets - week 44, 2019 (November

5,

2019)

-

U.S. &

Canada softwood and panel markets - week 43, 2019 ( October

29,

2019)

-

U.S. &

Canada softwood and panel markets - week 42, 2019 ( October

22,

2019)

-

U.S. &

Canada softwood and panel markets - week 41, 2019 ( October

15,

2019)

-

U.S. &

Canada softwood and panel markets - week 40, 2019 ( October

8,

2019)

-

U.S. &

Canada softwood and panel markets - week 39, 2019 ( October

1,

2019)

-

U.S. &

Canada softwood and panel markets - week 38, 2019 ( September 24,

2019)

-

U.S. softwood and panel markets - week 37, 2019 ( September 17,

2019)

-

U.S. softwood and panel markets - week 36, 2019 ( September 10,

2019)

-

U.S. softwood and panel markets - week 35, 2019 ( September 3,

2019)

-

U.S. softwood and panel markets - week 34, 2019 ( August 23,

2019)

-

U.S. softwood and panel markets - week 33, 2019 ( August 16,

2019)

-

U.S. softwood and panel markets - week 32, 2019 ( August 09,

2019)

-

U.S. softwood and panel markets - week 31, 2019 ( August 02,

2019)

-

U.S. softwood and panel markets - week 30, 2019 ( July

26, 2019)

-

U.S. softwood and panel markets - week 29, 2019 ( July 19,

2019)

-

U.S. softwood and panel markets - week 28, 2019 ( July 12,

2019)

-

U.S. softwood and panel markets - week 27, 2019 ( July 03,

2019)

-

U.S. softwood and panel markets - week 26, 2019 ( June 28,

2019)

-

U.S. softwood and panel markets - week 25, 2019 ( June 21,

2019)

-

U.S. softwood and panel markets - week 24, 2019 ( June 14,

2019)

-

U.S. softwood and panel markets - week 23, 2019 ( June 07,

2019)

-

U.S. softwood and panel markets - week 22, 2019 ( May 31,

2019)

-

U.S. softwood and panel markets - week 21, 2019 ( May 24,

2019)

-

U.S. softwood and panel markets - week 20, 2019 ( May 17,

2019)

-

U.S. softwood and panel markets - week 19, 2019 ( May 10,

2019)

-

U.S. softwood and panel markets - week 18, 2019 ( May 03,

2019)

-

U.S. softwood and panel markets - week 17, 2019 ( April 26,

2019)

-

U.S. softwood and panel markets - week 16, 2019 ( April 19,

2019)

-

U.S. softwood and panel markets - week 15, 2019 ( April 12,

2019)

-

U.S. softwood and panel markets - week 14, 2019 ( April 05,

2019)

-

U.S. softwood and panel markets - week 13, 2019 ( March

29, 2019)

-

U.S. softwood and panel markets - week 12, 2019 ( March

22, 2019)

-

U.S. softwood and panel markets - week 11, 2019 ( March

15, 2019)

-

U.S. softwood and panel markets - week 10, 2019 ( March

08, 2019)

-

U.S. softwood and panel markets - week 9, 2019 ( March

01, 2019)

-

U.S. softwood and panel markets - week 8, 2019 ( February.

22, 2019)

-

U.S. softwood and panel markets - week 7, 2019 ( February.

15, 2019)

-

U.S. softwood and panel markets - week 6, 2019 ( February.

08, 2019)

-

U.S. softwood and panel markets - week 5, 2019 ( February.

01, 2019)

-

U.S. softwood and panel markets - week 4, 2019 (January. 25,

2019)

-

U.S. softwood and panel markets - week 3, 2019 (January. 18,

2019)

-

U.S. softwood and panel markets - week 2, 2019 (January. 11,

2019)

-

U.S. softwood and panel markets - week 1, 2019 (January. 04,

2019)

|