By Madison's Lumber Reporter

At a time

when end-users have usually received delivery

for expected building needs until after

September, demand for North American

construction framing dimension Softwood Lumber

remained strong last week. Already with order

files into the end of September, sawmills quoted

higher on prices for product that was nowhere

near a production date. Customer inventories

were so lean and supply so weak that some Lumber

commodity items were impossible to find. When

volumes were located buyers agreed to any price

whatsoever, as long as they were assured

delivery. Even if that wouldn’t be for six

weeks.

In seemingly never-ending bad news, the 2020

storm season has arrived and is currently

battering the US east coast. If that damage is

serious, sales of Plywood will spike for

immediate needs then again later for rebuilding.

Supply of Panel building materials is as low as

that of Dimension Lumber, thus it is possible

for Plywood prices to drive up yet further.

Normally the rush of demand lasts approximately

six weeks. However this is clearly not a normal

time, and the US storm season is just starting.

Check back with Madison’s frequently to find out

what movements Panel prices, Plywood and

Oriented Strand Board (OSB), are doing.

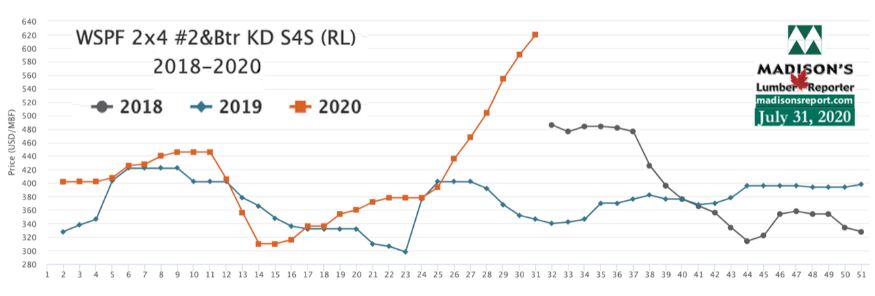

Following a Board-generated spate of confusion early the previous week,

the U.S. Western S-P-F Softwood Lumber market returned to a frenzy of

demand last week to close out July. Everyone from end users to secondary

suppliers hectically pursued any scrap of wood they got wind of, often

ending up empty-handed. Inventories at all levels were virtually

depleted and sawmills continued to fall behind in their harried efforts

to keep pace with demand. Prices were up significantly on all commodity

items and sawmill order files stretched into late August or early

September.

Canadian Western S-P-F purveyors described a state of near-pandemonium

in the market last week as the price of R/L #2&Btr 2×4 eclipsed the

vaunted US$600 mfbm mark, rising $30 to US$620 mfbm (net FOB sawmill).

All other dimension offerings climbed between $10 and $44, aside from

#4/Economy 2×4 and 2×6 which remained flat. Customers have become numb

to sticker shock in recent months and ultimately capitulated, so

desperate was their need for solid wood commodities. Canadian sawmills

continued to sell out every morning by 7:30am, with little to nothing

available for peddling on the cash market. Inventories at all levels

were empty.

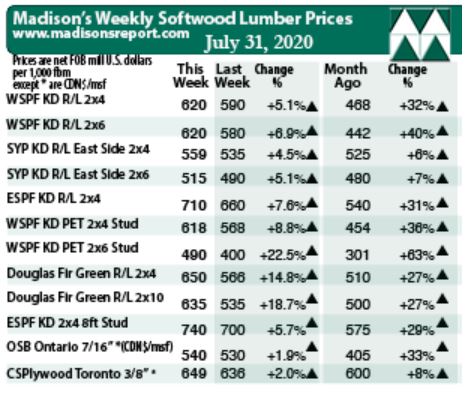

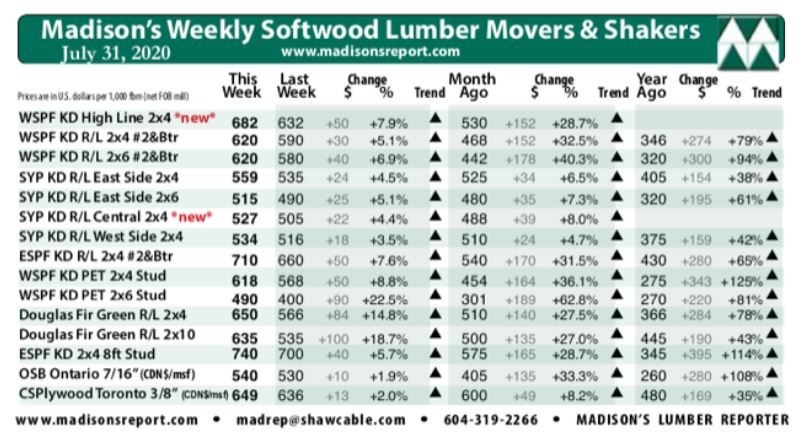

For the week ending July 31, 2020, prices of standard construction

framing dimension softwood lumber items popped up even higher. Benchmark

softwood lumber item Western S-P-F 2×4 #2&Btr KD price increased by +30,

or +5 per cent, to US$620 mfbm (net FOB sawmill), from US$590 the

previous week. The price for this lumber commodity was up +$152, or +32

per cent, from one month ago. Compared to the same week in 2019, when

this item was selling for US$346 mfbm, it is up +$274, or +79 per cent.

“Customers have become numb to sticker shock in

recent months and ultimately capitulated, so desperate was their need

for solid wood commodities.” — Madison’s Lumber Reporter

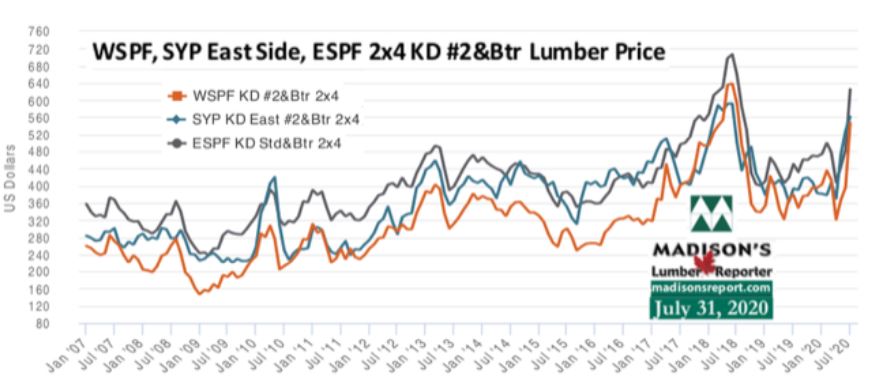

The crazy market in the Northeastern US persisted last week as frantic

buyers committed to wood they wouldn’t see until mid-September at prices

never even conceived of before. With costs so high and shipping so far

behind, Eastern stocking wholesalers at the docks in New Jersey noted

that prices or delivery dates were no longer the main sticking points,

rather it was credit lines. To paraphrase one veteran vendor, if you

can’t finish one job due to supply constraints how can you expect to get

the credit to start another one?

Last week’s Western S-P-F 2×4 price rose +$222, or +56 per cent,

relative to the one-year rolling average price of US$398 mfbm and grew

+$230, or +59 per cent, compared to the two-year rolling average prices

of US$390 mfbm.

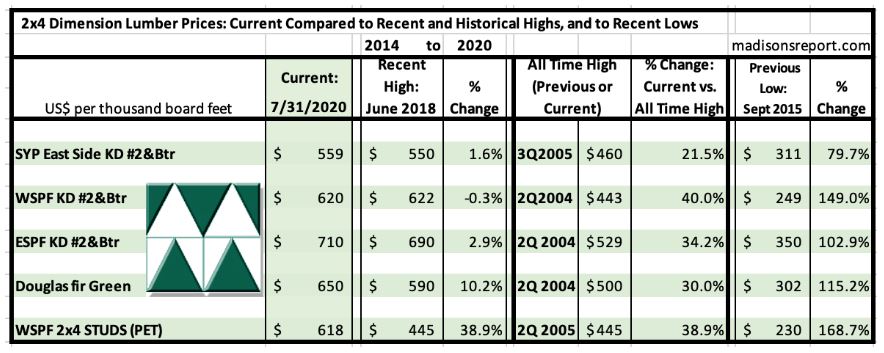

The below table is a comparison of recent highs, in June 2018, and

current July 2020 benchmark dimension Softwood Lumber 2×4 prices

compared to historical highs of 2004/05 and compared to recent lows of

Sept 2015:

Related News:

-

U.S. & Canada softwood and panel markets - week 29, 2020 (Jul

22,

2020)

-

U.S. & Canada softwood and panel markets - week 28, 2020 (Jul

22,

2020)

-

U.S. & Canada softwood and panel markets - week 27, 2020 (Jul

17,

2020)

-

U.S. & Canada softwood and panel markets - week 26, 2020 (Jul

10,

2020)

-

U.S. & Canada softwood and panel markets - week 25, 2020 (Jul

02,

2020)

-

U.S. & Canada softwood and panel markets - week 24, 2020 (Jun

25,

2020)

-

U.S. & Canada softwood and panel markets - week 23, 2020 (Jun

17,

2020)

-

U.S. &

Canada softwood and panel markets - week 22, 2020 (Jun

10,

2020)

-

U.S. &

Canada softwood and panel markets - week 21, 2020 (Jun

3,

2020)

-

U.S. &

Canada softwood and panel markets - week 20, 2020 (May 27,

2020)

-

U.S. &

Canada softwood and panel markets - week 19, 2020 (May 21,

2020)

-

U.S. &

Canada softwood and panel markets - week 18, 2020 (May 15,

2020)

-

U.S. &

Canada softwood and panel markets - week 17, 2020 (May 8,

2020)

-

U.S. &

Canada softwood and panel markets - week 16, 2020 (May 1,

2020)

-

U.S. &

Canada softwood and panel markets - week 15, 2020 (Apr

23,

2020)

-

U.S. &

Canada softwood and panel markets - week 14, 2020 (Apr

17,

2020)

-

U.S. &

Canada softwood and panel markets - week 13, 2020 (Apr

08,

2020)

-

U.S. &

Canada softwood and panel markets - week 12, 2020 (Mar

31,

2020)

-

U.S. &

Canada softwood and panel markets - week 11, 2020 (Mar

24,

2020)

-

U.S. &

Canada softwood and panel markets - week 5, 2020 (Feb

11,

2020)

-

U.S. &

Canada softwood and panel markets - week 4, 2020 (Feb

4,

2020)

-

U.S. &

Canada softwood and panel markets - week 3, 2020 (January

27,

2020)

-

U.S. &

Canada softwood and panel markets - week 2, 2020 (January

20,

2020)

-

U.S. &

Canada softwood and panel markets - week 1, 2020 (January

13,

2020)

-

U.S. &

Canada softwood and panel markets - week 50, 2019 (December

17,

2019)

-

U.S. &

Canada softwood and panel markets - week 49, 2019 (December

10,

2019)

-

U.S. &

Canada softwood and panel markets - week 48, 2019 (December

3,

2019)

-

U.S. &

Canada softwood and panel markets - week 47, 2019 (November

26,

2019)

-

U.S. &

Canada softwood and panel markets - week 46, 2019 (November

19,

2019)

-

U.S. &

Canada softwood and panel markets - week 45, 2019 (November

12,

2019)

-

U.S. &

Canada softwood and panel markets - week 44, 2019 (November

5,

2019)

-

U.S. &

Canada softwood and panel markets - week 43, 2019 ( October

29,

2019)

-

U.S. &

Canada softwood and panel markets - week 42, 2019 ( October

22,

2019)

-

U.S. &

Canada softwood and panel markets - week 41, 2019 ( October

15,

2019)

-

U.S. &

Canada softwood and panel markets - week 40, 2019 ( October

8,

2019)

-

U.S. &

Canada softwood and panel markets - week 39, 2019 ( October

1,

2019)

-

U.S. &

Canada softwood and panel markets - week 38, 2019 ( September 24,

2019)

-

U.S. softwood and panel markets - week 37, 2019 ( September 17,

2019)

-

U.S. softwood and panel markets - week 36, 2019 ( September 10,

2019)

-

U.S. softwood and panel markets - week 35, 2019 ( September 3,

2019)

-

U.S. softwood and panel markets - week 34, 2019 ( August 23,

2019)

-

U.S. softwood and panel markets - week 33, 2019 ( August 16,

2019)

-

U.S. softwood and panel markets - week 32, 2019 ( August 09,

2019)

-

U.S. softwood and panel markets - week 31, 2019 ( August 02,

2019)

-

U.S. softwood and panel markets - week 30, 2019 ( July

26, 2019)

-

U.S. softwood and panel markets - week 29, 2019 ( July 19,

2019)

-

U.S. softwood and panel markets - week 28, 2019 ( July 12,

2019)

-

U.S. softwood and panel markets - week 27, 2019 ( July 03,

2019)

-

U.S. softwood and panel markets - week 26, 2019 ( June 28,

2019)

-

U.S. softwood and panel markets - week 25, 2019 ( June 21,

2019)

-

U.S. softwood and panel markets - week 24, 2019 ( June 14,

2019)

-

U.S. softwood and panel markets - week 23, 2019 ( June 07,

2019)

-

U.S. softwood and panel markets - week 22, 2019 ( May 31,

2019)

-

U.S. softwood and panel markets - week 21, 2019 ( May 24,

2019)

-

U.S. softwood and panel markets - week 20, 2019 ( May 17,

2019)

-

U.S. softwood and panel markets - week 19, 2019 ( May 10,

2019)

-

U.S. softwood and panel markets - week 18, 2019 ( May 03,

2019)

-

U.S. softwood and panel markets - week 17, 2019 ( April 26,

2019)

-

U.S. softwood and panel markets - week 16, 2019 ( April 19,

2019)

-

U.S. softwood and panel markets - week 15, 2019 ( April 12,

2019)

-

U.S. softwood and panel markets - week 14, 2019 ( April 05,

2019)

-

U.S. softwood and panel markets - week 13, 2019 ( March

29, 2019)

-

U.S. softwood and panel markets - week 12, 2019 ( March

22, 2019)

-

U.S. softwood and panel markets - week 11, 2019 ( March

15, 2019)

-

U.S. softwood and panel markets - week 10, 2019 ( March

08, 2019)

-

U.S. softwood and panel markets - week 9, 2019 ( March

01, 2019)

-

U.S. softwood and panel markets - week 8, 2019 ( February.

22, 2019)

-

U.S. softwood and panel markets - week 7, 2019 ( February.

15, 2019)

-

U.S. softwood and panel markets - week 6, 2019 ( February.

08, 2019)

-

U.S. softwood and panel markets - week 5, 2019 ( February.

01, 2019)

-

U.S. softwood and panel markets - week 4, 2019 (January. 25,

2019)

-

U.S. softwood and panel markets - week 3, 2019 (January. 18,

2019)

-

U.S. softwood and panel markets - week 2, 2019 (January. 11,

2019)

-

U.S. softwood and panel markets - week 1, 2019 (January. 04,

2019)

|