By Madison's Lumber Reporter

North

American softwood lumber manufacturers,

wholesalers, distributors, buyers, and end-users

alike agree that this current supply-demand

situation, and resulting steep price increases

week-after-week, is truly unknown territory.

Sawmills across Canada and the US are either

running at full capacity or working to ramp-up

production after the new social-distancing rules

from the Covid-19 restrictions were put into the

place. Meanwhile, US housing — construction,

sales, and prices — is heating up only more and

more. All this at a time of year when home

builders and contractors have already ordered

and are receiving the wood they need for

projects ongoing through September.

Suffice to say: no one knows what is going on,

except that demand is non-stop and there just

isn’t enough wood on-hand with suppliers to keep

up. Order files at sawmills, whether in the

West, the East, or the South, were all firmly

into September. Customers looking for wood now

have to wait until mid-September before that

production is even booked at sawmills, then even

longer to receive delivery.

“Softwood lumber prices climbed yet again

as frustration and urgency among buyers reached

a fever pitch.” — Madison’s Lumber Reporter

Buyers of Western S-P-F in the US were getting used to picking their

jaws up off the floor each week as softwood lumber prices rose again to

meet or surpass previous record highs. In the face of these

unprecedented new levels, demand remained strong as ever according to

traders. Sawmill order files stretched into September on most items,

with increasingly late rail car arrivals adding multiple weeks to those

timelines. A general tone of frantic urgency continued to dominate the

market as customers jumped on any scrap of wood they could find,

regardless of species. Availability at all levels was basically

nonexistent, with wood coming in and going out too fast for players to

build inventory.

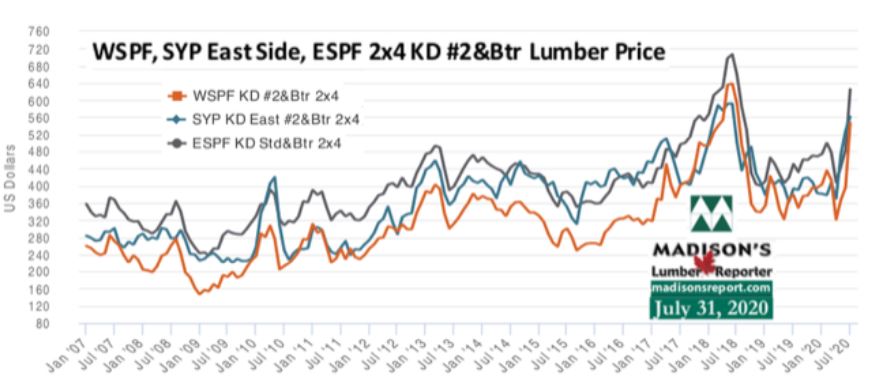

The wild ride of Western S-P-F in Canada continued last week as #2&Btr

2×4 climbed another $46 to US$666 mfbm. Standard grade and High Line

dimension all increased by double digits as sawmills were again

aggressive with their numbers and still received no pushback from

buyers. After demand in Canada paused briefly the previous week it came

roaring back, quickly cleaning out large producers every morning before

they could offer any cash wood to US customers. With secondary suppliers

unable to build any inventory, players don’t anticipate a correction to

prices in the near future. Order files at sawmills were into early

September, and shipment delays caused further frustration.

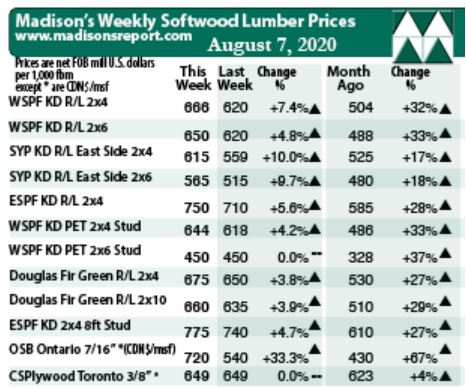

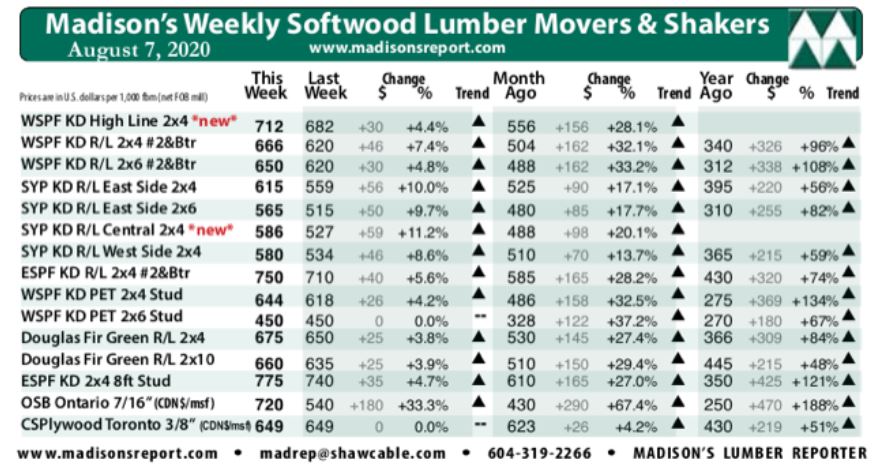

For the week ending August 7, 2020, prices of standard construction

framing dimension softwood lumber items jumped significantly. Benchmark

softwood lumber item Western S-P-F 2×4 #2&Btr KD price increased by +46,

or +7 per cent, to US$666 mfbm (net FOB sawmill), from US$620 the

previous week. The price for this lumber commodity was up +$162, or +32

per cent, from one month ago. Compared to the same week in 2019, when

this item was selling for US$340 mfbm, it is up +$326, or a whopping +96

per cent.

“Prices of softwood lumber advanced significantly again

and sawmills pushed their order files into early September in most

cases..” — Madison’s Lumber Reporter

Demand in the Eastern portion of the continent was extremely strong

again last week. Sawmills raised their asking prices on #2&Btr Eastern

S-P-F dimension between $40 and $55 in the Great Lakes market and $45

and $55 in the Toronto market. Hectic sales activity and inquiry were

the norm, and buyers desperately grabbed any material they could find.

Early September order files were commonly reported by sawmills and

customers knew they wouldn’t receive their orders until at least two

weeks after that.

As shocking price increases continued, last week’s Western S-P-F 2×4

price rose +$262, or +65 per cent, relative to the one-year rolling

average price of US$404 mfbm and grew a massive +$275, or +70 per cent,

compared to the two-year rolling average prices of US$391 mfbm.

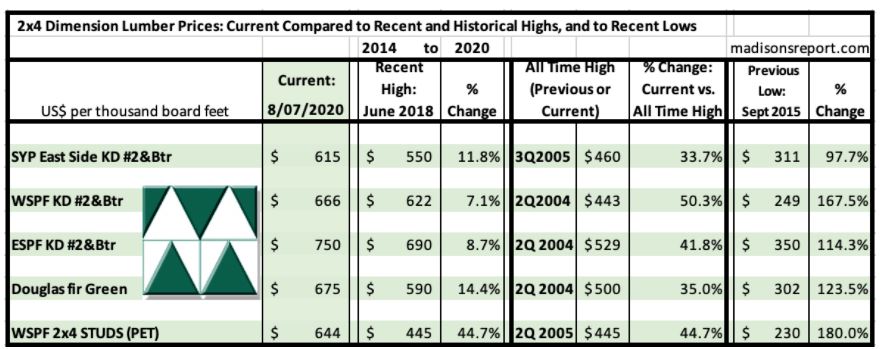

The below table is a comparison of recent highs, in June 2018, and

current August 2020 benchmark dimension Softwood Lumber 2×4 prices

compared to historical highs of 2004/05 and compared to recent lows of

Sept 2015:

Related News:

-

U.S. & Canada softwood and panel markets - week

30, 2020 (Aug

05,

2020)

-

U.S. & Canada softwood and panel markets - week 29, 2020 (Jul

29,

2020)

-

U.S. & Canada softwood and panel markets - week 28, 2020 (Jul

22,

2020)

-

U.S. & Canada softwood and panel markets - week 27, 2020 (Jul

17,

2020)

-

U.S. & Canada softwood and panel markets - week 26, 2020 (Jul

10,

2020)

-

U.S. & Canada softwood and panel markets - week 25, 2020 (Jul

02,

2020)

-

U.S. & Canada softwood and panel markets - week 24, 2020 (Jun

25,

2020)

-

U.S. & Canada softwood and panel markets - week 23, 2020 (Jun

17,

2020)

-

U.S. &

Canada softwood and panel markets - week 22, 2020 (Jun

10,

2020)

-

U.S. &

Canada softwood and panel markets - week 21, 2020 (Jun

3,

2020)

-

U.S. &

Canada softwood and panel markets - week 20, 2020 (May 27,

2020)

-

U.S. &

Canada softwood and panel markets - week 19, 2020 (May 21,

2020)

-

U.S. &

Canada softwood and panel markets - week 18, 2020 (May 15,

2020)

-

U.S. &

Canada softwood and panel markets - week 17, 2020 (May 8,

2020)

-

U.S. &

Canada softwood and panel markets - week 16, 2020 (May 1,

2020)

-

U.S. &

Canada softwood and panel markets - week 15, 2020 (Apr

23,

2020)

-

U.S. &

Canada softwood and panel markets - week 14, 2020 (Apr

17,

2020)

-

U.S. &

Canada softwood and panel markets - week 13, 2020 (Apr

08,

2020)

-

U.S. &

Canada softwood and panel markets - week 12, 2020 (Mar

31,

2020)

-

U.S. &

Canada softwood and panel markets - week 11, 2020 (Mar

24,

2020)

-

U.S. &

Canada softwood and panel markets - week 5, 2020 (Feb

11,

2020)

-

U.S. &

Canada softwood and panel markets - week 4, 2020 (Feb

4,

2020)

-

U.S. &

Canada softwood and panel markets - week 3, 2020 (January

27,

2020)

-

U.S. &

Canada softwood and panel markets - week 2, 2020 (January

20,

2020)

-

U.S. &

Canada softwood and panel markets - week 1, 2020 (January

13,

2020)

-

U.S. &

Canada softwood and panel markets - week 50, 2019 (December

17,

2019)

-

U.S. &

Canada softwood and panel markets - week 49, 2019 (December

10,

2019)

-

U.S. &

Canada softwood and panel markets - week 48, 2019 (December

3,

2019)

-

U.S. &

Canada softwood and panel markets - week 47, 2019 (November

26,

2019)

-

U.S. &

Canada softwood and panel markets - week 46, 2019 (November

19,

2019)

-

U.S. &

Canada softwood and panel markets - week 45, 2019 (November

12,

2019)

-

U.S. &

Canada softwood and panel markets - week 44, 2019 (November

5,

2019)

-

U.S. &

Canada softwood and panel markets - week 43, 2019 ( October

29,

2019)

-

U.S. &

Canada softwood and panel markets - week 42, 2019 ( October

22,

2019)

-

U.S. &

Canada softwood and panel markets - week 41, 2019 ( October

15,

2019)

-

U.S. &

Canada softwood and panel markets - week 40, 2019 ( October

8,

2019)

-

U.S. &

Canada softwood and panel markets - week 39, 2019 ( October

1,

2019)

-

U.S. &

Canada softwood and panel markets - week 38, 2019 ( September 24,

2019)

-

U.S. softwood and panel markets - week 37, 2019 ( September 17,

2019)

-

U.S. softwood and panel markets - week 36, 2019 ( September 10,

2019)

-

U.S. softwood and panel markets - week 35, 2019 ( September 3,

2019)

-

U.S. softwood and panel markets - week 34, 2019 ( August 23,

2019)

-

U.S. softwood and panel markets - week 33, 2019 ( August 16,

2019)

-

U.S. softwood and panel markets - week 32, 2019 ( August 09,

2019)

-

U.S. softwood and panel markets - week 31, 2019 ( August 02,

2019)

-

U.S. softwood and panel markets - week 30, 2019 ( July

26, 2019)

-

U.S. softwood and panel markets - week 29, 2019 ( July 19,

2019)

-

U.S. softwood and panel markets - week 28, 2019 ( July 12,

2019)

-

U.S. softwood and panel markets - week 27, 2019 ( July 03,

2019)

-

U.S. softwood and panel markets - week 26, 2019 ( June 28,

2019)

-

U.S. softwood and panel markets - week 25, 2019 ( June 21,

2019)

-

U.S. softwood and panel markets - week 24, 2019 ( June 14,

2019)

-

U.S. softwood and panel markets - week 23, 2019 ( June 07,

2019)

-

U.S. softwood and panel markets - week 22, 2019 ( May 31,

2019)

-

U.S. softwood and panel markets - week 21, 2019 ( May 24,

2019)

-

U.S. softwood and panel markets - week 20, 2019 ( May 17,

2019)

-

U.S. softwood and panel markets - week 19, 2019 ( May 10,

2019)

-

U.S. softwood and panel markets - week 18, 2019 ( May 03,

2019)

-

U.S. softwood and panel markets - week 17, 2019 ( April 26,

2019)

-

U.S. softwood and panel markets - week 16, 2019 ( April 19,

2019)

-

U.S. softwood and panel markets - week 15, 2019 ( April 12,

2019)

-

U.S. softwood and panel markets - week 14, 2019 ( April 05,

2019)

-

U.S. softwood and panel markets - week 13, 2019 ( March

29, 2019)

-

U.S. softwood and panel markets - week 12, 2019 ( March

22, 2019)

-

U.S. softwood and panel markets - week 11, 2019 ( March

15, 2019)

-

U.S. softwood and panel markets - week 10, 2019 ( March

08, 2019)

-

U.S. softwood and panel markets - week 9, 2019 ( March

01, 2019)

-

U.S. softwood and panel markets - week 8, 2019 ( February.

22, 2019)

-

U.S. softwood and panel markets - week 7, 2019 ( February.

15, 2019)

-

U.S. softwood and panel markets - week 6, 2019 ( February.

08, 2019)

-

U.S. softwood and panel markets - week 5, 2019 ( February.

01, 2019)

-

U.S. softwood and panel markets - week 4, 2019 (January. 25,

2019)

-

U.S. softwood and panel markets - week 3, 2019 (January. 18,

2019)

-

U.S. softwood and panel markets - week 2, 2019 (January. 11,

2019)

-

U.S. softwood and panel markets - week 1, 2019 (January. 04,

2019)

|