By Madison's Lumber Reporter

Madison’s Lumber Reporter advises North American

forest products manufacturers to put on their

seat belts, as the latest housing market data

indicates no stop to relentlessly rising

softwood lumber prices any time soon. Currently,

sawmills in Canada and the U.S. simply can not

keep up with ongoing very strong demand for

house construction in both countries. While some

builders and contractors are beginning to hold

off on projects in anticipation of the usual

autumn slow-down in demand for building

materials, others are committed to construction

already started and can do nothing but place

orders for much-needed wood. As stated in the

past few weeks: it is delivery times rather than

price which determine whether an order for

lumber will be closed. Customers continue to

vigorously search throughout the supply chain

for even small quantities of necessary lumber,

despite having to wait more than a month for

materials to arrive at job sites.

Both existing home sales and new home sales, as

well as prices, data released in the past few

days in the U.S. and Canada show extremely

strong demand. A lot of this demand has been

pent-up since before the lock down and

restrictions due to the COVID-19 pandemic;

meaning there will be no reversal any time soon.

Truly this is unprecedented, in several ways,

and it is impossible to make a projection about

what is going to happen as winter 2020 looms.

Storm season in the U.S. looks to be coming on

strong, which could very well put further upward

pressure on panel prices. Especially plywood,

for repairs and reconstruction. “Lumber

prices soared higher as desperate demand

continued to outpace constrained supply.” —

Madison’s Lumber Reporter

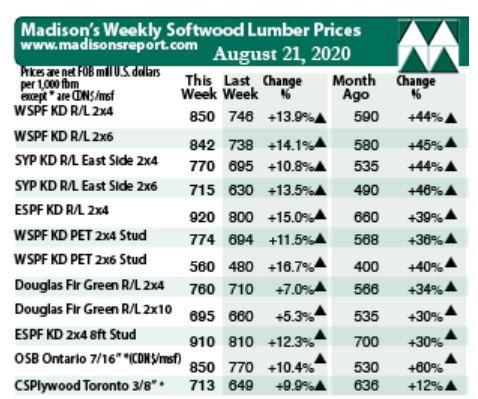

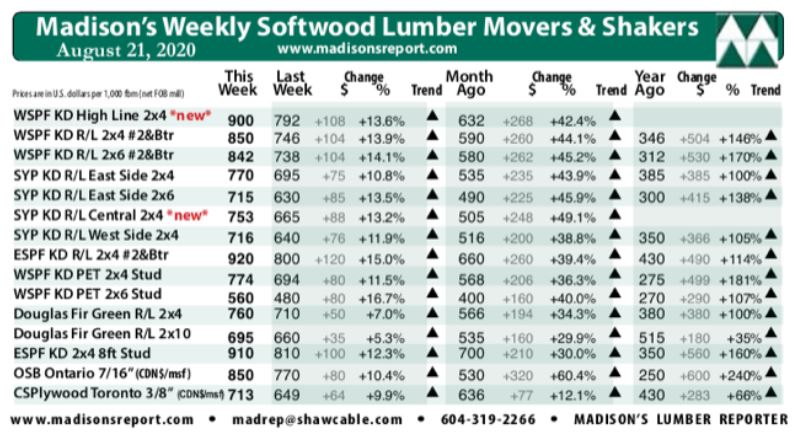

Western S-P-F purveyors in the United States reported another crazy week

of extremely limited availability as buyers desperately tried to cover

their most pressing needs. Prices soared again and sawmills pushed their

order files into late September, with delivery times extending into

mid-October thanks to mounting rail car delays. Field inventories at all

levels were depleted and secondary suppliers had little to offer for

quick shipment. Prices of low grade offerings came on strong in the past

fortnight as buyers broadened their search to include literally any

piece of processed fibre they could find.

There was no pause in the insanity last week as Canadian Western S-P-F

producers sold out every day before 8:00am, leaving no cash wood

available for customers in the U.S. Prices vaulted again, last week by

an astounding $104 on both 2×4 and 2×6 R/L #2&Btr dimension, to US$850

and U.S.$842 mfbm respectively. Sales of low grade items got some

serious traction last week also, with #3/Utility and #4/Economy rising

by between $40 and $76. According to sellers, there was no push back

whatsoever on these head-spinning prices as the market remained under

bought and field inventories were virtually empty. Demand in Canada was

especially nutty to hear producers tell it. September 28 order files at

sawmills were common, while actual arrival times pushed into November as

transportation worsened.

Much to the astonishment of all and dismay of some, for the week ending

August 21, 2020, prices of standard construction framing dimension

softwood lumber items soared almost out of the scope of possibility.

Benchmark softwood lumber item Western S-P-F 2×4 #2&Btr KD price hurtled

up +104, or +14 per cent, to US$850 mfbm (net FOB sawmill), from US$746

the previous week. The price for this lumber commodity was up +$260, or

+44 per cent, from one month ago. Compared to the same week in 2019,

when this item was selling for US$346 mfbm, it is up +$504, or an

unprecedented +146 per cent.

“For Eastern stocking wholesalers at the ports in New Jersey,

prices continued to rise last week and sales retained their fever-pitch.

Demand apparently slowed down marginally, with vendors noting that less

volume was changing hands.” — Madison’s Lumber Reporter

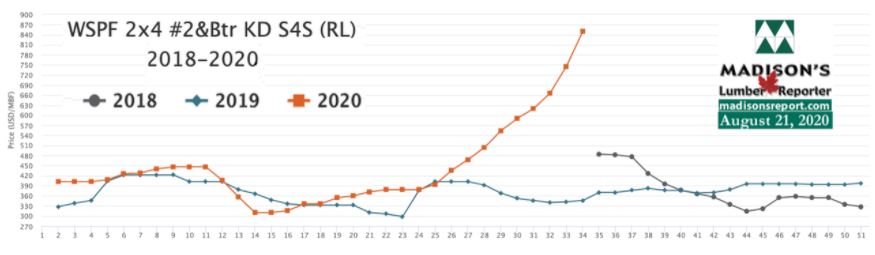

Shooting up into previously unknown territory, last week’s Western S-P-F

2×4 price increased by +$428, or +101 per cent, relative to the one-year

rolling average price of US$422 mfbm and was up +$453, or +114 per cent,

compared to the two-year rolling average prices of US$397 mfbm.

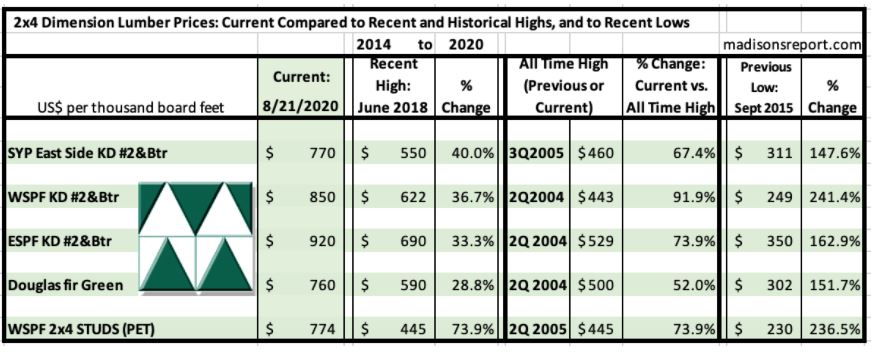

The below table is a comparison of recent highs, in June 2018, and

current August 2020 benchmark dimension Softwood Lumber 2×4 prices

compared to historical highs of 2004/05 and compared to recent lows of

Sept 2015:

Related News:

-

U.S. & Canada softwood and panel markets - week

32, 2020 (Aug

19,

2020)

-

U.S. & Canada softwood and panel markets - week

31, 2020 (Aug

12,

2020)

-

U.S. & Canada softwood and panel markets - week

30, 2020 (Aug

05,

2020)

-

U.S. & Canada softwood and panel markets - week 29, 2020 (Jul

29,

2020)

-

U.S. & Canada softwood and panel markets - week 28, 2020 (Jul

22,

2020)

-

U.S. & Canada softwood and panel markets - week 27, 2020 (Jul

17,

2020)

-

U.S. & Canada softwood and panel markets - week 26, 2020 (Jul

10,

2020)

-

U.S. & Canada softwood and panel markets - week 25, 2020 (Jul

02,

2020)

-

U.S. & Canada softwood and panel markets - week 24, 2020 (Jun

25,

2020)

-

U.S. & Canada softwood and panel markets - week 23, 2020 (Jun

17,

2020)

-

U.S. &

Canada softwood and panel markets - week 22, 2020 (Jun

10,

2020)

-

U.S. &

Canada softwood and panel markets - week 21, 2020 (Jun

3,

2020)

-

U.S. &

Canada softwood and panel markets - week 20, 2020 (May 27,

2020)

-

U.S. &

Canada softwood and panel markets - week 19, 2020 (May 21,

2020)

-

U.S. &

Canada softwood and panel markets - week 18, 2020 (May 15,

2020)

-

U.S. &

Canada softwood and panel markets - week 17, 2020 (May 8,

2020)

-

U.S. &

Canada softwood and panel markets - week 16, 2020 (May 1,

2020)

-

U.S. &

Canada softwood and panel markets - week 15, 2020 (Apr

23,

2020)

-

U.S. &

Canada softwood and panel markets - week 14, 2020 (Apr

17,

2020)

-

U.S. &

Canada softwood and panel markets - week 13, 2020 (Apr

08,

2020)

-

U.S. &

Canada softwood and panel markets - week 12, 2020 (Mar

31,

2020)

-

U.S. &

Canada softwood and panel markets - week 11, 2020 (Mar

24,

2020)

-

U.S. &

Canada softwood and panel markets - week 5, 2020 (Feb

11,

2020)

-

U.S. &

Canada softwood and panel markets - week 4, 2020 (Feb

4,

2020)

-

U.S. &

Canada softwood and panel markets - week 3, 2020 (January

27,

2020)

-

U.S. &

Canada softwood and panel markets - week 2, 2020 (January

20,

2020)

-

U.S. &

Canada softwood and panel markets - week 1, 2020 (January

13,

2020)

-

U.S. &

Canada softwood and panel markets - week 50, 2019 (December

17,

2019)

-

U.S. &

Canada softwood and panel markets - week 49, 2019 (December

10,

2019)

-

U.S. &

Canada softwood and panel markets - week 48, 2019 (December

3,

2019)

-

U.S. &

Canada softwood and panel markets - week 47, 2019 (November

26,

2019)

-

U.S. &

Canada softwood and panel markets - week 46, 2019 (November

19,

2019)

-

U.S. &

Canada softwood and panel markets - week 45, 2019 (November

12,

2019)

-

U.S. &

Canada softwood and panel markets - week 44, 2019 (November

5,

2019)

-

U.S. &

Canada softwood and panel markets - week 43, 2019 ( October

29,

2019)

-

U.S. &

Canada softwood and panel markets - week 42, 2019 ( October

22,

2019)

-

U.S. &

Canada softwood and panel markets - week 41, 2019 ( October

15,

2019)

-

U.S. &

Canada softwood and panel markets - week 40, 2019 ( October

8,

2019)

-

U.S. &

Canada softwood and panel markets - week 39, 2019 ( October

1,

2019)

-

U.S. &

Canada softwood and panel markets - week 38, 2019 ( September 24,

2019)

-

U.S. softwood and panel markets - week 37, 2019 ( September 17,

2019)

-

U.S. softwood and panel markets - week 36, 2019 ( September 10,

2019)

-

U.S. softwood and panel markets - week 35, 2019 ( September 3,

2019)

-

U.S. softwood and panel markets - week 34, 2019 ( August 23,

2019)

-

U.S. softwood and panel markets - week 33, 2019 ( August 16,

2019)

-

U.S. softwood and panel markets - week 32, 2019 ( August 09,

2019)

-

U.S. softwood and panel markets - week 31, 2019 ( August 02,

2019)

-

U.S. softwood and panel markets - week 30, 2019 ( July

26, 2019)

-

U.S. softwood and panel markets - week 29, 2019 ( July 19,

2019)

-

U.S. softwood and panel markets - week 28, 2019 ( July 12,

2019)

-

U.S. softwood and panel markets - week 27, 2019 ( July 03,

2019)

-

U.S. softwood and panel markets - week 26, 2019 ( June 28,

2019)

-

U.S. softwood and panel markets - week 25, 2019 ( June 21,

2019)

-

U.S. softwood and panel markets - week 24, 2019 ( June 14,

2019)

-

U.S. softwood and panel markets - week 23, 2019 ( June 07,

2019)

-

U.S. softwood and panel markets - week 22, 2019 ( May 31,

2019)

-

U.S. softwood and panel markets - week 21, 2019 ( May 24,

2019)

-

U.S. softwood and panel markets - week 20, 2019 ( May 17,

2019)

-

U.S. softwood and panel markets - week 19, 2019 ( May 10,

2019)

-

U.S. softwood and panel markets - week 18, 2019 ( May 03,

2019)

-

U.S. softwood and panel markets - week 17, 2019 ( April 26,

2019)

-

U.S. softwood and panel markets - week 16, 2019 ( April 19,

2019)

-

U.S. softwood and panel markets - week 15, 2019 ( April 12,

2019)

-

U.S. softwood and panel markets - week 14, 2019 ( April 05,

2019)

-

U.S. softwood and panel markets - week 13, 2019 ( March

29, 2019)

-

U.S. softwood and panel markets - week 12, 2019 ( March

22, 2019)

-

U.S. softwood and panel markets - week 11, 2019 ( March

15, 2019)

-

U.S. softwood and panel markets - week 10, 2019 ( March

08, 2019)

-

U.S. softwood and panel markets - week 9, 2019 ( March

01, 2019)

-

U.S. softwood and panel markets - week 8, 2019 ( February.

22, 2019)

-

U.S. softwood and panel markets - week 7, 2019 ( February.

15, 2019)

-

U.S. softwood and panel markets - week 6, 2019 ( February.

08, 2019)

-

U.S. softwood and panel markets - week 5, 2019 ( February.

01, 2019)

-

U.S. softwood and panel markets - week 4, 2019 (January. 25,

2019)

-

U.S. softwood and panel markets - week 3, 2019 (January. 18,

2019)

-

U.S. softwood and panel markets - week 2, 2019 (January. 11,

2019)

-

U.S. softwood and panel markets - week 1, 2019 (January. 04,

2019)

|