By Madison's Lumber Reporter

There was more confusion in the North American

construction framing dimension softwood lumber

market last week as prices of most home building

solid wood commodity items stayed flat, except

Eastern S-P-F which did correct down somewhat.

The supply-demand balance seemed to be finding

an even keel, although customers still were

reluctant to make big purchases at unprecedented

highs. The latest U.S. data for housing starts,

home sales, and house prices all show phenomenal

increases, indicating very strong demand for

real construction and remodeling projects could

keep prices up for a while yet.

Privately-owned U.S. housing starts in August

were at a seasonally adjusted annual rate of

1,416,000, the U.S. Commerce Department said

September 17. This is -5 per cent below the

revised July estimate of 1,492,000, but is +3

per cent above the August 2019 rate of

1,377,000. Total starts were up +3 per cent

year-over-year compared to August 2019. The dip

in housing starts was driven by a -25 per cent

decline in multifamily construction activity.

Single-family housing starts in August were at a

rate of 1,021,000; this is +4 per cent above the

revised July figure of 981,000. Single family

starts were up +12 per cent year-over-year.

Elsewhere, the U.S. Commerce Department said

Thursday new home sales rose +5 per cent to a

seasonally adjusted annual rate of 1.011 million

units last month, the highest level since

September 2006. New home sales are counted at

the signing of a contract, making them a leading

housing market indicator. New home sales are up

+43.2 per cent from August 2019. There were

282,000 new homes on the market in the U.S. last

month, down from 291,000 in July. At August’s

sales pace it would take 3.3 months to clear the

supply of houses on the market, down from 3.6

months in July. About 71 per cent of the homes

sold last month were either under construction

or yet to be built. “The August figure is the

first reading above 1 million since 2006, so

both new and existing home sales registered

their best results since 2006 in August,” said

Amherst Pierpont Chief Economist Stephen Stanley

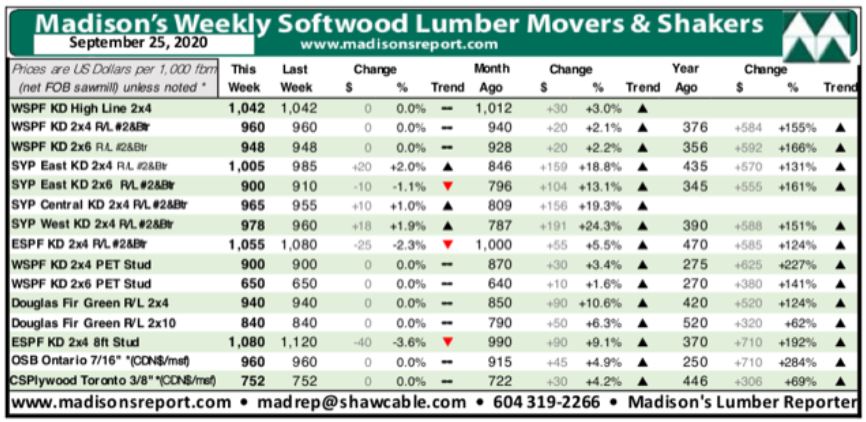

"Eastern Canadian lumber and stud

producers reported slower sales activity last

week as buyers who would have pounced on loads a

couple weeks ago began to vacillate and throw

out counter offers. Sawmill order files were

around three weeks out with very limited

material available any earlier.” — Madison’s

Lumber Reporter

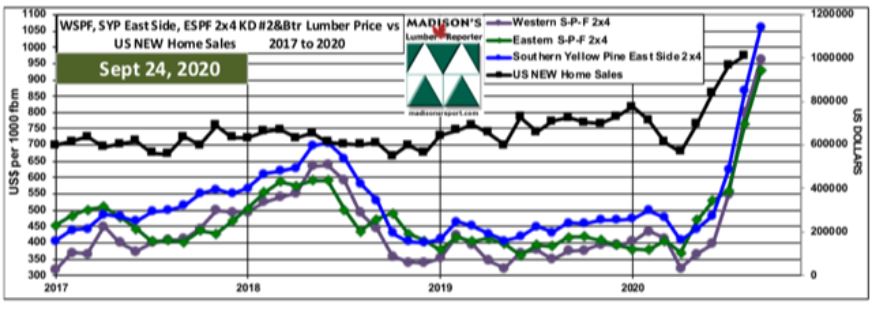

Sales volumes of Western S-P-F lumber and studs in the United States

took another step back last week. Buyers were increasingly cautious as

the disparity between November lumber futures and the current cash

market reduced overall urgency to buy. Sawmills held on to order files

into at least late October and kept their prices flat. Lack of supply

was a constant topic of discussion and field inventories remained nearly

empty in most cases.

Western S-P-F sales activity in Canada remained quiet last week as

buyers were content to wait for previously-ordered wood to arrive while

they filled their inventory gaps opportunistically from the distribution

level. Producers maintained five week order files at sawmills and were

unworried about the pause in demand, as they were keenly aware of the

depleted state of all downstream field inventories. Rail car supply was

still an issue, which predictably put increasing pressure on truck

availability.

“Overall supply levels remained extremely low throughout the

chain, and demand continued to handily outpace material availability. ”

— Madison’s Lumber Reporter

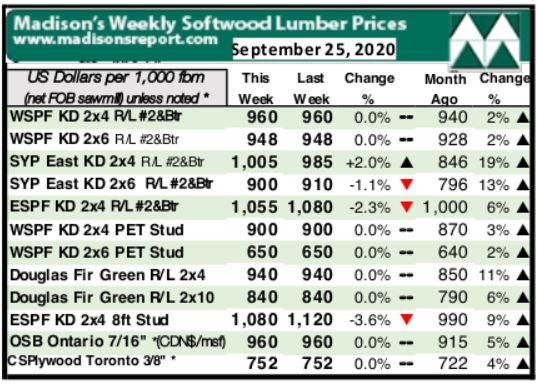

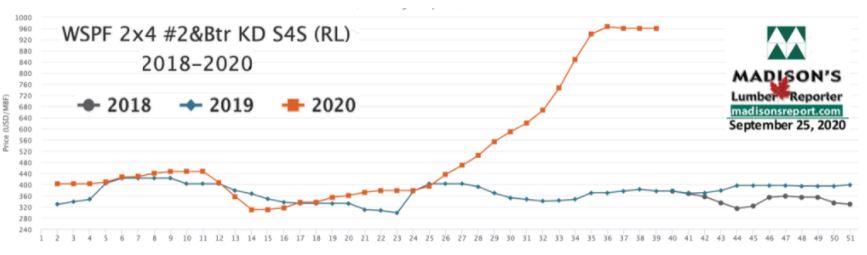

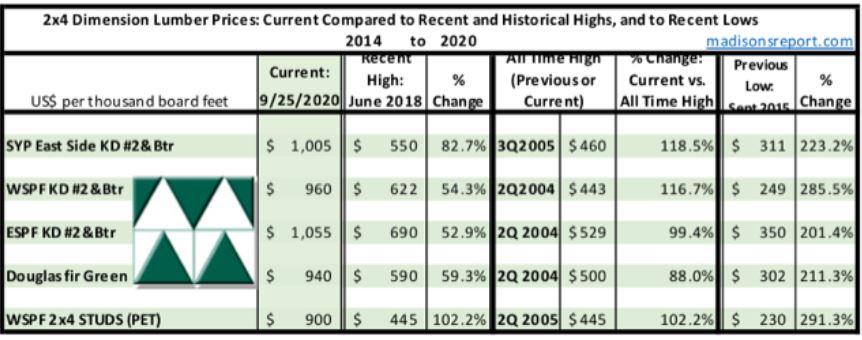

For the week ending September 25, 2020 the price of benchmark

softwood lumber commodity item Western S-P-F KD 2×4 #2&Btr remained

flat, as in recent weeks, at US$960 mfbm, said Madison’s Lumber

Reporter. This price is +$20, or +2 per cent more than it was one month

ago. Compared to mid-September 2019, this price is up a remarkable

+$584, or +155 per cent.

“Dimension lumber prices were flat while panels (Plywood and OSB)

seemed to have finally topped out. ” — Madison’s Lumber Reporter

Compared to one-year-ago, last week’s Western S-P-F KD 2×4 #2&Btr price

was +$480, or +100 per cent, higher than the one-year rolling average

price of US$480 mfbm and was up +$538, or +127 per cent, compared to the

two-year rolling average price of US$422 mfbm.

The below table is a comparison of recent highs, in June 2018, and

current September 2020 benchmark dimension Softwood Lumber 2×4 prices

compared to historical highs of 2004/05 and compared to recent lows of

Sept 2015:

Related News:

-

U.S. & Canada softwood and panel markets - week

37, 2020 (Sep

23,

2020)

-

U.S. & Canada softwood and panel markets - week

36, 2020 (Sep

16,

2020)

-

U.S. & Canada softwood and panel markets - week

35, 2020 (Sep

09,

2020)

-

U.S. & Canada softwood and panel markets - week

34, 2020 (Sep

02,

2020)

-

U.S. & Canada softwood and panel markets - week

33, 2020 (Aug

26,

2020)

-

U.S. & Canada softwood and panel markets - week

32, 2020 (Aug

19,

2020)

-

U.S. & Canada softwood and panel markets - week

31, 2020 (Aug

12,

2020)

-

U.S. & Canada softwood and panel markets - week

30, 2020 (Aug

05,

2020)

-

U.S. & Canada softwood and panel markets - week 29, 2020 (Jul

29,

2020)

-

U.S. & Canada softwood and panel markets - week 28, 2020 (Jul

22,

2020)

-

U.S. & Canada softwood and panel markets - week 27, 2020 (Jul

17,

2020)

-

U.S. & Canada softwood and panel markets - week 26, 2020 (Jul

10,

2020)

-

U.S. & Canada softwood and panel markets - week 25, 2020 (Jul

02,

2020)

-

U.S. & Canada softwood and panel markets - week 24, 2020 (Jun

25,

2020)

-

U.S. & Canada softwood and panel markets - week 23, 2020 (Jun

17,

2020)

-

U.S. &

Canada softwood and panel markets - week 22, 2020 (Jun

10,

2020)

-

U.S. &

Canada softwood and panel markets - week 21, 2020 (Jun

3,

2020)

-

U.S. &

Canada softwood and panel markets - week 20, 2020 (May 27,

2020)

-

U.S. &

Canada softwood and panel markets - week 19, 2020 (May 21,

2020)

-

U.S. &

Canada softwood and panel markets - week 18, 2020 (May 15,

2020)

-

U.S. &

Canada softwood and panel markets - week 17, 2020 (May 8,

2020)

-

U.S. &

Canada softwood and panel markets - week 16, 2020 (May 1,

2020)

-

U.S. &

Canada softwood and panel markets - week 15, 2020 (Apr

23,

2020)

-

U.S. &

Canada softwood and panel markets - week 14, 2020 (Apr

17,

2020)

-

U.S. &

Canada softwood and panel markets - week 13, 2020 (Apr

08,

2020)

-

U.S. &

Canada softwood and panel markets - week 12, 2020 (Mar

31,

2020)

-

U.S. &

Canada softwood and panel markets - week 11, 2020 (Mar

24,

2020)

-

U.S. &

Canada softwood and panel markets - week 5, 2020 (Feb

11,

2020)

-

U.S. &

Canada softwood and panel markets - week 4, 2020 (Feb

4,

2020)

-

U.S. &

Canada softwood and panel markets - week 3, 2020 (January

27,

2020)

-

U.S. &

Canada softwood and panel markets - week 2, 2020 (January

20,

2020)

-

U.S. &

Canada softwood and panel markets - week 1, 2020 (January

13,

2020)

-

U.S. &

Canada softwood and panel markets - week 50, 2019 (December

17,

2019)

-

U.S. &

Canada softwood and panel markets - week 49, 2019 (December

10,

2019)

-

U.S. &

Canada softwood and panel markets - week 48, 2019 (December

3,

2019)

-

U.S. &

Canada softwood and panel markets - week 47, 2019 (November

26,

2019)

-

U.S. &

Canada softwood and panel markets - week 46, 2019 (November

19,

2019)

-

U.S. &

Canada softwood and panel markets - week 45, 2019 (November

12,

2019)

-

U.S. &

Canada softwood and panel markets - week 44, 2019 (November

5,

2019)

-

U.S. &

Canada softwood and panel markets - week 43, 2019 ( October

29,

2019)

-

U.S. &

Canada softwood and panel markets - week 42, 2019 ( October

22,

2019)

-

U.S. &

Canada softwood and panel markets - week 41, 2019 ( October

15,

2019)

-

U.S. &

Canada softwood and panel markets - week 40, 2019 ( October

8,

2019)

-

U.S. &

Canada softwood and panel markets - week 39, 2019 ( October

1,

2019)

-

U.S. &

Canada softwood and panel markets - week 38, 2019 ( September 24,

2019)

-

U.S. softwood and panel markets - week 37, 2019 ( September 17,

2019)

-

U.S. softwood and panel markets - week 36, 2019 ( September 10,

2019)

-

U.S. softwood and panel markets - week 35, 2019 ( September 3,

2019)

-

U.S. softwood and panel markets - week 34, 2019 ( August 23,

2019)

-

U.S. softwood and panel markets - week 33, 2019 ( August 16,

2019)

-

U.S. softwood and panel markets - week 32, 2019 ( August 09,

2019)

-

U.S. softwood and panel markets - week 31, 2019 ( August 02,

2019)

-

U.S. softwood and panel markets - week 30, 2019 ( July

26, 2019)

-

U.S. softwood and panel markets - week 29, 2019 ( July 19,

2019)

-

U.S. softwood and panel markets - week 28, 2019 ( July 12,

2019)

-

U.S. softwood and panel markets - week 27, 2019 ( July 03,

2019)

-

U.S. softwood and panel markets - week 26, 2019 ( June 28,

2019)

-

U.S. softwood and panel markets - week 25, 2019 ( June 21,

2019)

-

U.S. softwood and panel markets - week 24, 2019 ( June 14,

2019)

-

U.S. softwood and panel markets - week 23, 2019 ( June 07,

2019)

-

U.S. softwood and panel markets - week 22, 2019 ( May 31,

2019)

-

U.S. softwood and panel markets - week 21, 2019 ( May 24,

2019)

-

U.S. softwood and panel markets - week 20, 2019 ( May 17,

2019)

-

U.S. softwood and panel markets - week 19, 2019 ( May 10,

2019)

-

U.S. softwood and panel markets - week 18, 2019 ( May 03,

2019)

-

U.S. softwood and panel markets - week 17, 2019 ( April 26,

2019)

-

U.S. softwood and panel markets - week 16, 2019 ( April 19,

2019)

-

U.S. softwood and panel markets - week 15, 2019 ( April 12,

2019)

-

U.S. softwood and panel markets - week 14, 2019 ( April 05,

2019)

-

U.S. softwood and panel markets - week 13, 2019 ( March

29, 2019)

-

U.S. softwood and panel markets - week 12, 2019 ( March

22, 2019)

-

U.S. softwood and panel markets - week 11, 2019 ( March

15, 2019)

-

U.S. softwood and panel markets - week 10, 2019 ( March

08, 2019)

-

U.S. softwood and panel markets - week 9, 2019 ( March

01, 2019)

-

U.S. softwood and panel markets - week 8, 2019 ( February.

22, 2019)

-

U.S. softwood and panel markets - week 7, 2019 ( February.

15, 2019)

-

U.S. softwood and panel markets - week 6, 2019 ( February.

08, 2019)

-

U.S. softwood and panel markets - week 5, 2019 ( February.

01, 2019)

-

U.S. softwood and panel markets - week 4, 2019 (January. 25,

2019)

-

U.S. softwood and panel markets - week 3, 2019 (January. 18,

2019)

-

U.S. softwood and panel markets - week 2, 2019 (January. 11,

2019)

-

U.S. softwood and panel markets - week 1, 2019 (January. 04,

2019)

|