Despite somewhat soft demand, as many customers weren’t sure where prices

were going so waited to buy, lumber prices popped up again in mid-February.

This due mostly to ongoing capacity restrictions, especially in the

important timber supply basket of British Columbia. As the spring building

season fast approaches, end-users will not be able to wait much longer to

order the wood necessary for upcoming building projects. Especially given

that delivery times remain quite extended — currently a minimum of six

weeks. Inventories in the field are tight, as secondary suppliers also held

off buying to see if prices might drop. Or flatten. At the current level,

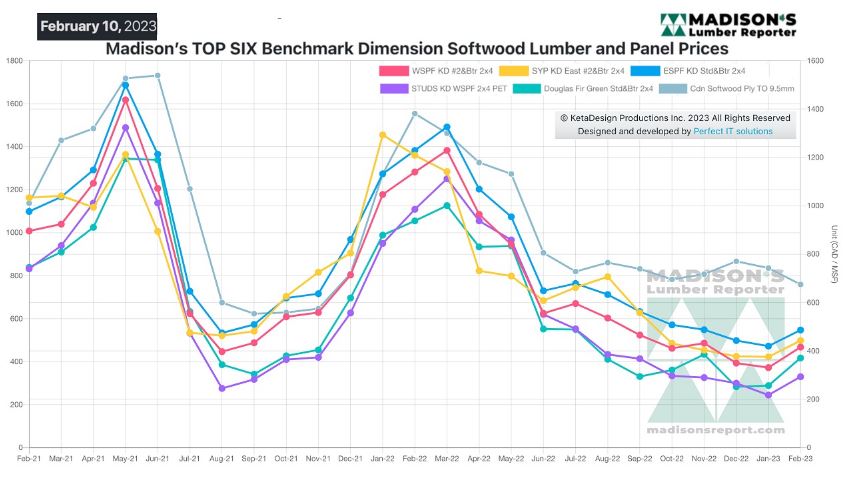

the benchmark commodity item, Western S-P-F 2×4, price is hovering at just

below the recognized average cost-of-production of US$500 mfbm.

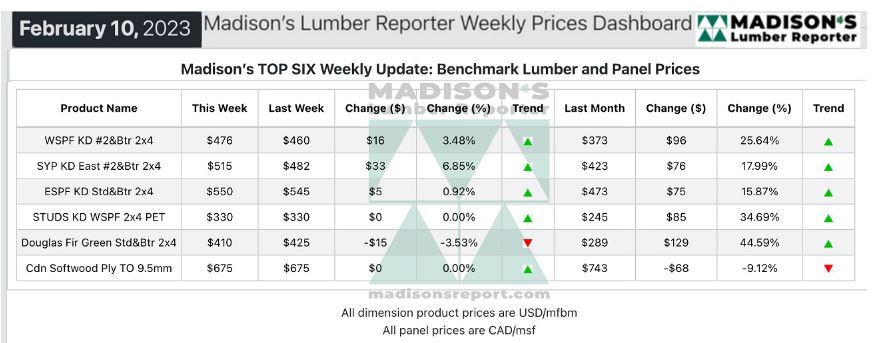

In the week ending February 10, the price of benchmark softwood lumber item

Western Spruce-Pine-Fir 2×4 #2&Btr KD (RL) was US$476 mfbm, which is up by

$16 or 3.0 per cent, from the previous week when it was US$360 mfbm. This is

up by $104, or 28 per cent, from one month ago when it was $373.

Supply levels remained tight due to the significant reduction in production

volume caused by the aforementioned mill changes.

“Prices of panels appeared to find a bottom, while the recent climb in

lumber and stud prices tapered off to stable-but-firm levels.” — Madison’s

Lumber Reporter

The Western S-P-F market in the United States experienced balance after a

period of solid business activity generated by Western producer curtailment

and closure announcements. Sawmill order files extended into late-February

or early-March, reflecting producers’ cautiously optimistic confidence. On

the other hand, buyers took a step back after shoring up their inventories

in January, waiting for the market to show a clear direction.

Demand for Western S-P-F in Canada slowed down to a more stable pace with

commodity prices settling at or slightly above the previous week’s levels.

In reaction to the myriad curtailment and closure announcements over the

past five weeks, most buyers had already extended their coverage, choosing

to digest their positions for the time being. Availability of prompt supply

was limited, even as the odd load popped up before quickly getting snatched.

Two- to four-week order files were most common as producers solidified their

positions for the balance of February.

“The U.S. Northeast witnessed unseasonable weather conditions, leading

Eastern wholesalers to speculate that the spring season may not be as

favourable as anticipated. This resulted in a decline in sales and a

reluctance among buyers to build up their inventory for the upcoming

building season. Additionally, inventory holders were cautious about paying

more for carloads, given the lengthy transportation time of approximately

six weeks.” — Madison’s Lumber Reporter

Compared to the same week last year, when it was US$1,220 mfbm, the price of

Western Spruce-Pine-Fir 2×4 #2&Btr KD (RL) for the week ending February 10,

2023 this price was down by $744, or 61 per cent. Compared to two years ago

when it was $960, that week’s price is down by $484, or 50 per cent.

More Reports: