|

Lumber and panel market weekly report ----

Week

37, 2022 |

|

By Madison's Lumber Reporter

As inventories in the field tightened up in

North America, many benchmark softwood lumber

prices stayed flat in mid-September. Supply at

producers was quite lean, providing sawmills the

opportunity to keep prices flat as they boosted

order files out to two weeks – which is quite

strong for the time of year. For their part,

wholesalers and other secondary suppliers

offered somewhat lower prices to keep their more

ample volumes of product on-hand moving. The

week had begun with a potential major job action

on US railways at the top of everyone’s minds,

prompting those who had been waiting to make

purchases to get off the fence and actually buy.

Of course, the dispute was settled well before

any actual work stoppage occurred, so by the end

of that week all fears of delayed deliveries

were dismissed.

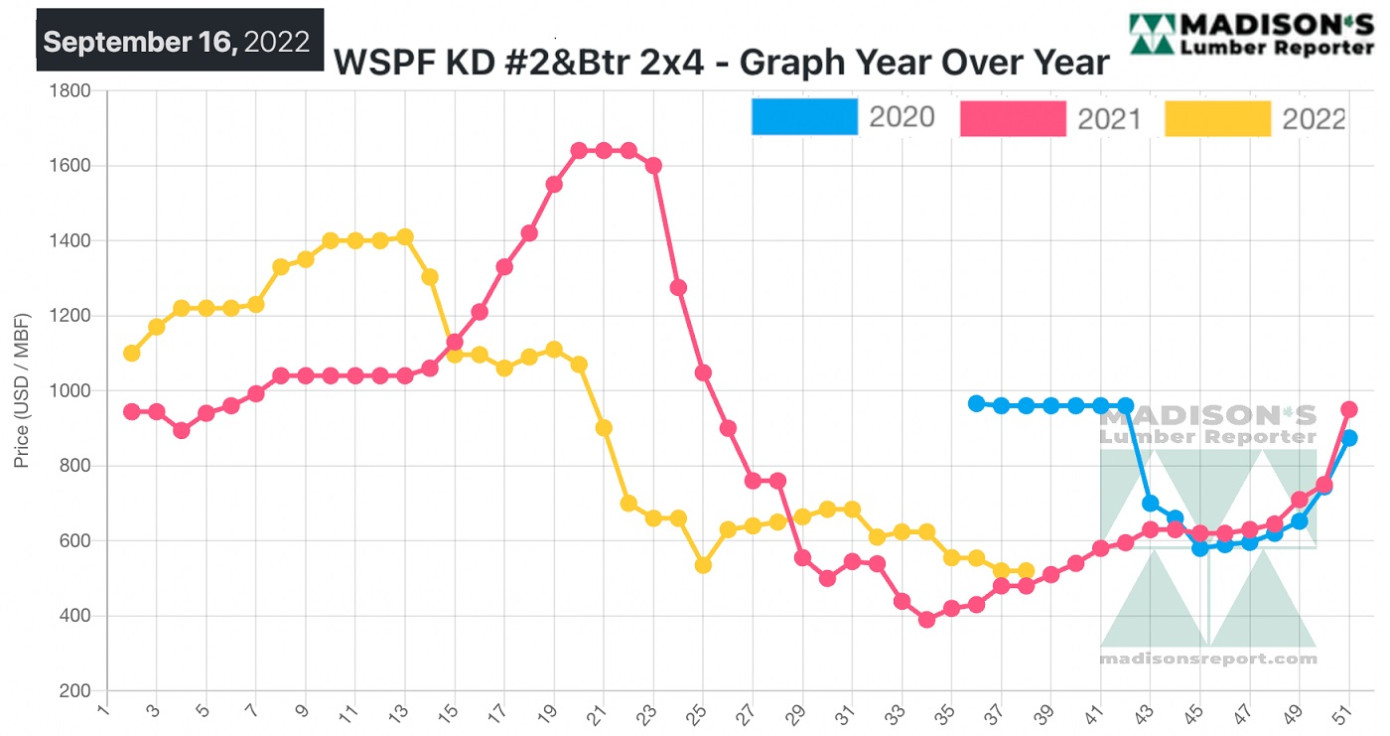

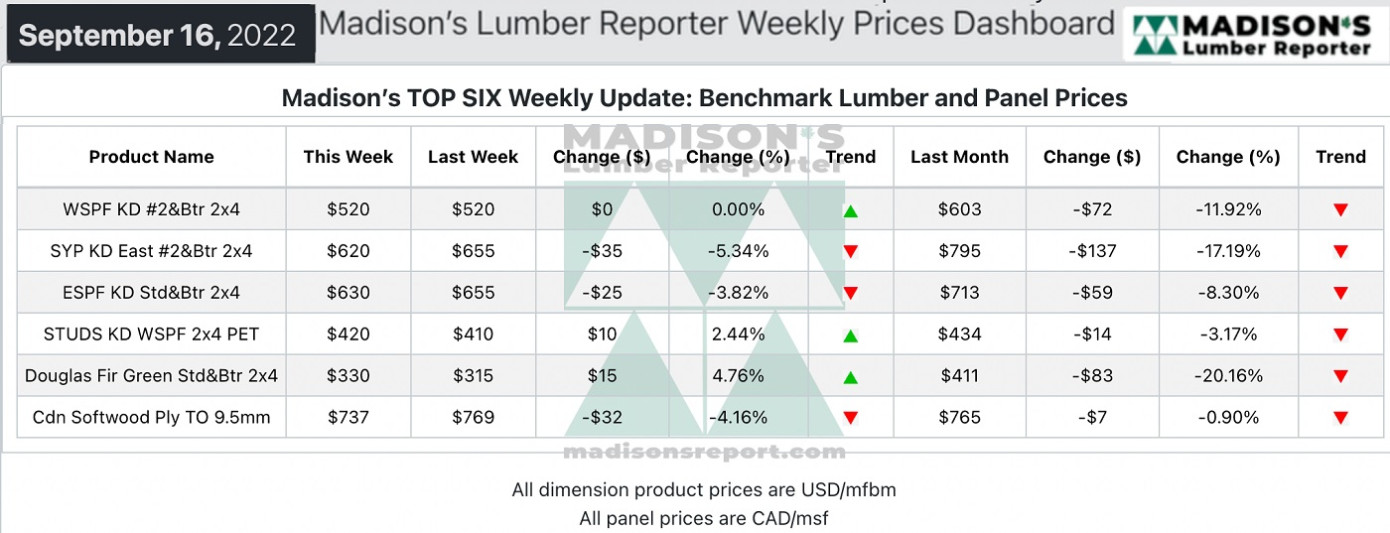

Limited field inventories for the week ending

September 16, 2022 kept the price of benchmark

softwood lumber item Western Spruce-Pine-Fir 2x4

#2&Btr KD (RL) at US$520 mfbm, said weekly

forest products industry price guide newsletter

Madison’s Lumber Reporter. This is down by $0,

or 0% from the previous week when it was $520,

and is down by -$83, or -14%, from one month ago

when it was $603.

Sawmills were apparently still taking counter

offers to clear out certain straight lengths

which continued to show prompt availability,

while common R/L offerings began to garner order

files up to two weeks out.

The lumber market was in a pensive, anticipatory

state as players waited for a resolution to the

potential nationwide rail strike in the United

States.

US Western S-P-F sawmills reported encouraging

levels of demand as buyers responded to

uncertainty caused by the rail employment

fiasco. Further forcing customers’ hands were

the persistently-depleted state of field

inventories, following a long period of strictly

hand-to-mouth buying.

Purveyors of Western S-P-F lumber in Canada

noted a better tone to demand. A considerable

contingent of buyers pulled the trigger as

pressure generated by the threat of a nationwide

rail strike in the US became too much to bear.

Suppliers consequently reported steadily

improving demand, with prices on several

bread-and-butter commodities printing flat or up

from the previous week’s levels. However, the

longevity of this recent surge in business was

very much in question.

Stud prices rebounded for the most part, with

2x6 trims gaining the most ground. The

turnaround further dismasted already-confused

buyers, pushing many off the fence and into

deal-now mode. Stud mill order files were into

late-September and knocking on the door of

October, while previously-ample availability in

most items appeared to be drying up.

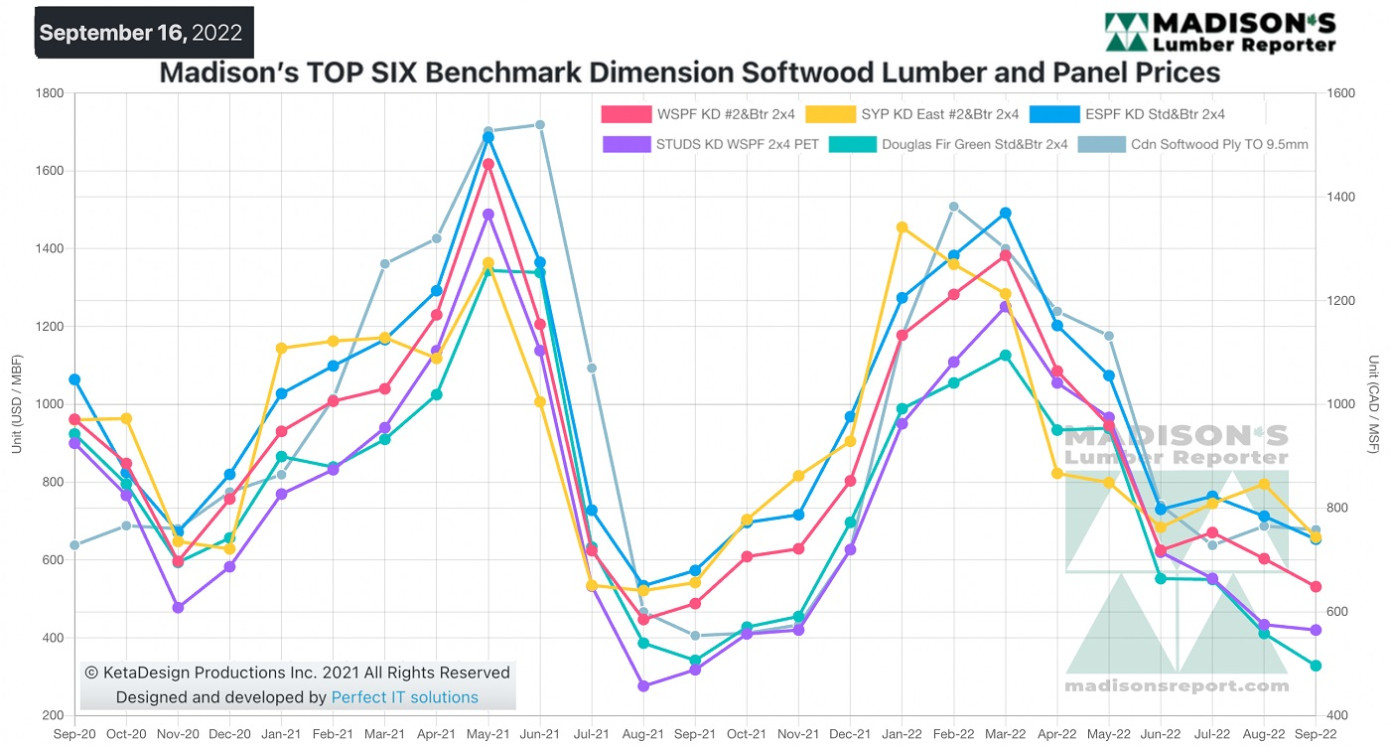

Madison’s Benchmark Top-Six Softwood Lumber and Panel

Prices: Monthly Averages

Compared to the same week last year, when it was US$480 mfbm, the price

of Western Spruce-Pine-Fir 2x4 #2&Btr KD (RL) for the week ending

September 16, 2022 was up by +$40, or +8%. Compared to two years ago

when it was $960, that week’s price is down by -$440, or -46%.

.

-

U.S. & Canada softwood and panel markets - week

36 2022 (Sep

20,

2022)

-

U.S. & Canada softwood and panel markets - week

35 2022 (Sep

13,

2022)

-

U.S. & Canada softwood and panel markets - week

34 2022 (Sep

06,

2022)

-

U.S. & Canada softwood and panel markets - week

33 2022 (Aug

30,

2022)

-

U.S. & Canada softwood and panel markets - week

32 2022 (Aug

23,

2022)

-

U.S. & Canada softwood and panel markets - week

31 2022 (Aug

16,

2022)

-

U.S. & Canada softwood and panel markets - week

30 2022 (Aug

09,

2022)

-

U.S. & Canada softwood and panel markets - week

29 2022 (Aug

02,

2022)

-

U.S. & Canada softwood and panel markets - week

28 2022 (Jul

26,

2022)

-

U.S. & Canada softwood and panel markets - week

27 2022 (Jul

19,

2022)

-

U.S. & Canada softwood and panel markets - week

26 2022 (Jul

12,

2022)

-

U.S. & Canada softwood and panel markets - week

25 2022 (Jul

05,

2022)

-

U.S. & Canada softwood and panel markets - week

24 2022 (Jun

29,

2022)

-

U.S. & Canada softwood and panel markets - week

23 2022 (Jun

22,

2022)

-

U.S. & Canada softwood and panel markets - week

22 2022 (Jun

15,

2022)

-

U.S. & Canada softwood and panel markets - week

21 2022 (Jun

08,

2022)

-

U.S. & Canada softwood and panel markets - week

20 2022 (Jun

01,

2022)

-

U.S. & Canada softwood and panel markets - week

19 2022 (May

25,

2022)

-

U.S. & Canada softwood and panel markets - week

18 2022 (May

18,

2022)

-

U.S. & Canada softwood and panel markets - week

17 2022 (May

11,

2022)

-

U.S. & Canada softwood and panel markets - week

16 2022 (May

04,

2022)

-

U.S. & Canada softwood and panel markets - week

15 2022 (Apr

26,

2022)

-

U.S. & Canada softwood and panel markets - week

14 2022 (Apr

19,

2022)

-

U.S. & Canada softwood and panel markets - week

13 2022 (Apr

12,

2022)

-

U.S. & Canada softwood and panel markets - week

12 2022 (Apr

05,

2022)

-

U.S. & Canada softwood and panel markets - week

11 2022 (Mar

29,

2022)

-

U.S. & Canada softwood and panel markets - week

10 2022 (Mar

22,

2022)

-

U.S. & Canada softwood and panel markets - week

9 2022 (Mar

15,

2022)

-

U.S. & Canada softwood and panel markets - week

8 2022 (Mar

08,

2022)

-

U.S. & Canada softwood and panel markets - week

7 2022 (Mar

01,

2022)

-

U.S. & Canada softwood and panel markets - week

6 2022 (Feb

22,

2022)

-

U.S. & Canada softwood and panel markets - week

5 2022 (Feb

15,

2022)

-

U.S. & Canada softwood and panel markets - week

4 2022 (Feb

08,

2022)

-

U.S. & Canada softwood and panel markets - week

3 2022 (Feb

01,

2022)

-

U.S. & Canada softwood and panel markets - week

2 2022 (Jan

25,

2022)

-

U.S. & Canada softwood and panel markets - week

1 2022 (Jan

18,

2022)

-

U.S. & Canada softwood and panel markets - week

47 2021 (Dec

22,

2021)

-

U.S. & Canada softwood and panel markets - week

46 2021 (Dec

15,

2021)

-

U.S. & Canada softwood and panel markets - week

45 2021 (Dec

08,

2021)

-

U.S. & Canada softwood and panel markets - week

44 2021 (Dec

01,

2021)

-

U.S. & Canada softwood and panel markets - week

43 2021 (Nov24,

2021)

-

U.S. & Canada softwood and panel markets - week

42 2021 (Nov17,

2021)

-

U.S. & Canada softwood and panel markets - week

41 2021 (Nov10,

2021)

-

U.S. & Canada softwood and panel markets - week

40 2021 (Nov

03,

2021)

-

U.S. & Canada softwood and panel markets - week

39 2021 (Oct

27,

2021)

-

U.S. & Canada softwood and panel markets - week

38 2021 (Oct

20,

2021)

-

U.S. & Canada softwood and panel markets - week

37 2021 (Oct

13,

2021)

-

U.S. & Canada softwood and panel markets - week

36 2021 (Oct

06,

2021)

-

U.S. & Canada softwood and panel markets - week

35 2021 (Sep

29,

2021)

-

U.S. & Canada softwood and panel markets - week

34 2021 (Sep

22,

2021)

-

U.S. & Canada softwood and panel markets - week

33 2021 (Sep

8,

2021)

-

U.S. & Canada softwood and panel markets - week

32 2021 (Sep

1,

2021)

-

U.S. & Canada softwood and panel markets - week

31 2021 (Aug

25,

2021)

-

U.S. & Canada softwood and panel markets - week

30 2021 (Aug

18,

2021)

-

U.S. & Canada softwood and panel markets - week

29 2021 (Aug

11,

2021)

-

U.S. & Canada softwood and panel markets - week

28 2021 (Aug

04,

2021)

-

U.S. & Canada softwood and panel markets - week

27 2021 (Jul

28,

2021)

-

U.S. & Canada softwood and panel markets - week

26 2021 (Jul

21,

2021)

-

U.S. & Canada softwood and panel markets - week

25 2021 (Jul

14,

2021)

-

U.S. & Canada softwood and panel markets - week

24 2021 (Jul

07,

2021)

-

U.S. & Canada softwood and panel markets - week

23 2021 (Jun

30,

2021)

-

U.S. & Canada softwood and panel markets - week

22 2021 (Jun

23,

2021)

-

U.S. & Canada softwood and panel markets - week

21 2021 (Jun

10,

2021)

-

U.S. & Canada softwood and panel markets - week

20 2021 (Jun

03,

2021)

-

U.S. & Canada softwood and panel markets - week

19 2021 (May

26,

2021)

-

U.S. & Canada softwood and panel markets - week

18 2021 (May

19,

2021)

-

U.S. & Canada softwood and panel markets - week

17 2021 (May

12,

2021)

-

U.S. & Canada softwood and panel markets - week

16 2021 (May

5,

2021)

-

U.S. & Canada softwood and panel markets - week

15 2021 (Apr

28,

2021)

-

U.S. & Canada softwood and panel markets - week

14 2021 (Apr

21,

2021)

-

U.S. & Canada softwood and panel markets - week

13 2021 (Apr

15,

2021)

-

U.S. & Canada softwood and panel markets - week

12 2021 (Apr

8,

2021)

-

U.S. & Canada softwood and panel markets - week

11 2021 (Apr

1,

2021)

-

U.S. & Canada softwood and panel markets - week

10 2021 (Mar

25,

2021)

-

U.S. & Canada softwood and panel markets - week

09 2021 (Mar

17,

2021)

-

U.S. & Canada softwood and panel markets - week

08 2021 (Mar

10,

2021)

-

U.S. & Canada softwood and panel markets - week

07 2021 (Mar

03,

2021)

-

U.S. & Canada softwood and panel markets - week

06 2021 (Feb

24,

2021)

-

U.S. & Canada softwood and panel markets - week

05 2021 (Feb

16,

2021)

-

U.S. & Canada softwood and panel markets - week

04 2021 (Feb

04,

2021)

-

U.S. & Canada softwood and panel markets - week

03 2021 (Jan

29,

2021)

-

U.S.&nb303& Canada softwood and panel markets - week

02 2021 (Jan

22,

2021)

-

U.S. & Canada softwood and panel markets - week

01 2021 (Jan

15,

2021)

-

U.S. & Canada softwood and panel markets - week

49 2020 (Dec

16,

2020)

-

U.S. & Canada softwood and panel markets - week

48 2020 (Dec

09,

2020)

-

U.S. & Canada softwood and panel markets - week

47 2020 (Dec

02,

2020)

-

U.S. & Canada softwood and panel markets - week

46 2020 (Nov

25,

2020)

-

U.S. & Canada softwood and panel markets - week

45 2020 (Nov

18,

2020)

-

U.S. & Canada softwood and panel markets - week

44 2020 (Nov

11,

2020)

-

U.S. & Canada softwood and panel markets - week

43 2020 (Nov

4,

2020)

-

U.S. & Canada softwood and panel markets - week

42 2020 (Oct

28,

2020)

-

U.S. & Canada softwood and panel markets - week

41 2020 (Oct

21,

2020)

-

U.S. & Canada softwood and panel markets - week

40 2020 (Oct

14,

2020)

-

U.S. & Canada softwood and panel markets - week

39, 2020 (Oct

07,

2020)

-

U.S. & Canada softwood and panel markets - week

38, 2020 (Sep

30,

2020)

-

U.S. & Canada softwood and panel markets - week

37, 2020 (Sep

23,

2020)

-

U.S. & Canada softwood and panel markets - week

36, 2020 (Sep

16,

2020)

-

U.S. & Canada softwood and panel markets - week

35, 2020 (Sep

09,

2020)

-

U.S. & Canada softwood and panel markets - week

34, 2020 (Sep

02,

2020)

-

U.S. & Canada softwood and panel markets - week

33, 2020 (Aug

26,

2020)

-

U.S. & Canada softwood and panel markets - week

32, 2020 (Aug

19,

2020)

-

U.S. & Canada softwood and panel markets - week

31, 2020 (Aug

12,

2020)

-

U.S. & Canada softwood and panel markets - week

30, 2020 (Aug

05,

2020)

-

U.S. & Canada softwood and panel markets - week 29, 2020 (Jul

29,

2020)

-

U.S. & Canada softwood and panel markets - week 28, 2020 (Jul

22,

2020)

-

U.S. & Canada softwood and panel markets - week 27, 2020 (Jul

17,

2020)

-

U.S. & Canada softwood and panel markets - week 26, 2020 (Jul

10,

2020)

-

U.S. & Canada softwood and panel markets - week 25, 2020 (Jul

02,

2020)

-

U.S. & Canada softwood and panel markets - week 24, 2020 (Jun

25,

2020)

-

U.S. & Canada softwood and panel markets - week 23, 2020 (Jun

17,

2020)

-

U.S. &

Canada softwood and panel markets - week 22, 2020 (Jun

10,

2020)

-

U.S. &

Canada softwood and panel markets - week 21, 2020 (Jun

3,

2020)

-

U.S. &

Canada softwood and panel markets - week 20, 2020 (May 27,

2020)

-

U.S. &

Canada softwood and panel markets - week 19, 2020 (May 21,

2020)

-

U.S. &

Canada softwood and panel markets - week 18, 2020 (May 15,

2020)

-

U.S. &

Canada softwood and panel markets - week 17, 2020 (May 8,

2020)

-

U.S. &

Canada softwood and panel markets - week 16, 2020 (May 1,

2020)

-

U.S. &

Canada softwood and panel markets - week 15, 2020 (Apr

23,

2020)

-

U.S. &

Canada softwood and panel markets - week 14, 2020 (Apr

17,

2020)

-

U.S. &

Canada softwood and panel markets - week 13, 2020 (Apr

08,

2020)

-

U.S. &

Canada softwood and panel markets - week 12, 2020 (Mar

31,

2020)

-

U.S. &

Canada softwood and panel markets - week 11, 2020 (Mar

24,

2020)

-

U.S. &

Canada softwood and panel markets - week 5, 2020 (Feb

11,

2020)

-

U.S. &

Canada softwood and panel markets - week 4, 2020 (Feb

4,

2020)

-

U.S. &

Canada softwood and panel markets - week 3, 2020 (January

27,

2020)

-

U.S. &

Canada softwood and panel markets - week 2, 2020 (January

20,

2020)

-

U.S. &

Canada softwood and panel markets - week 1, 2020 (January

13,

2020)

-

U.S. &

Canada softwood and panel markets - week 50, 2019 (December

17,

2019)

-

U.S. &

Canada softwood and panel markets - week 49, 2019 (December

10,

2019)

-

U.S. &

Canada softwood and panel markets - week 48, 2019 (December

3,

2019)

-

U.S. &

Canada softwood and panel markets - week 47, 2019 (November

26,

2019)

-

U.S. &

Canada softwood and panel markets - week 46, 2019 (November

19,

2019)

-

U.S. &

Canada softwood and panel markets - week 45, 2019 (November

12,

2019)

-

U.S. &

Canada softwood and panel markets - week 44, 2019 (November

5,

2019)

-

U.S. &

Canada softwood and panel markets - week 43, 2019 ( October

29,

2019)

-

U.S. &

Canada softwood and panel markets - week 42, 2019 ( October

22,

2019)

-

U.S. &

Canada softwood and panel markets - week 41, 2019 ( October

15,

2019)

-

U.S. &

Canada softwood and panel markets - week 40, 2019 ( October

8,

2019)

-

U.S. &

Canada softwood and panel markets - week 39, 2019 ( October

1,

2019)

-

U.S. &

Canada softwood and panel markets - week 38, 2019 ( September 24,

2019)

-

U.S. softwood and panel markets - week 37, 2019 ( September 17,

2019)

-

U.S. softwood and panel markets - week 36, 2019 ( September 10,

2019)

-

U.S. softwood and panel markets - week 35, 2019 ( September 3,

2019)

-

U.S. softwood and panel markets - week 34, 2019 ( August 23,

2019)

-

U.S. softwood and panel markets - week 33, 2019 ( August 16,

2019)

-

U.S. softwood and panel markets - week 32, 2019 ( August 09,

2019)

-

U.S. softwood and panel markets - week 31, 2019 ( August 02,

2019)

-

U.S. softwood and panel markets - week 30, 2019 ( July

26, 2019)

-

U.S. softwood and panel markets - week 29, 2019 ( July 19,

2019)

-

U.S. softwood and panel markets - week 28, 2019 ( July 12,

2019)

-

U.S. softwood and panel markets - week 27, 2019 ( July 03,

2019)

-

U.S. softwood and panel markets - week 26, 2019 ( June 28,

2019)

-

U.S. softwood and panel markets - week 25, 2019 ( June 21,

2019)

-

U.S. softwood and panel markets - week 24, 2019 ( June 14,

2019)

-

U.S. softwood and panel markets - week 23, 2019 ( June 07,

2019)

-

U.S. softwood and panel markets - week 22, 2019 ( May 31,

2019)

-

U.S. softwood and panel markets - week 21, 2019 ( May 24,

2019)

-

U.S. softwood and panel markets - week 20, 2019 ( May 17,

2019)

-

U.S. softwood and panel markets - week 19, 2019 ( May 10,

2019)

-

U.S. softwood and panel markets - week 18, 2019 ( May 03,

2019)

-

U.S. softwood and panel markets - week 17, 2019 ( April 26,

2019)

-

U.S. softwood and panel markets - week 16, 2019 ( April 19,

2019)

-

U.S. softwood and panel markets - week 15, 2019 ( April 12,

2019)

-

U.S. softwood and panel markets - week 14, 2019 ( April 05,

2019)

-

U.S. softwood and panel markets - week 13, 2019 ( March

29, 2019)

-

U.S. softwood and panel markets - week 12, 2019 ( March

22, 2019)

-

U.S. softwood and panel markets - week 11, 2019 ( March

15, 2019)

-

U.S. softwood and panel markets - week 10, 2019 ( March

08, 2019)

-

U.S. softwood and panel markets - week 9, 2019 ( March

01, 2019)

-

U.S. softwood and panel markets - week 8, 2019 ( February.

22, 2019)

-

U.S. softwood and panel markets - week 7, 2019 ( February.

15, 2019)

-

U.S. softwood and panel markets - week 6, 2019 ( February.

08, 2019)

-

U.S. softwood and panel markets - week 5, 2019 ( February.

01, 2019)

-

U.S. softwood and panel markets - week 4, 2019 (January. 25,

2019)

-

U.S. softwood and panel markets - week 3, 2019 (January. 18,

2019)

-

U.S. softwood and panel markets - week 2, 2019 (January. 11,

2019)

-

U.S. softwood and panel markets - week 1, 2019 (January. 04,

2019)

|

|

|