|

Lumber and panel market weekly report ----

Week

7, 2022 |

|

By Madison's Lumber Reporter

Most lumber prices rose by a noticeable margin

in the week ending February 18, as ongoing

strong demand and relentless delayed deliveries

prompted customers who had been waiting on the

sidelines to step in and buy. Due to

still-lengthening order files, sawmills were

able to hold their ground on prices.

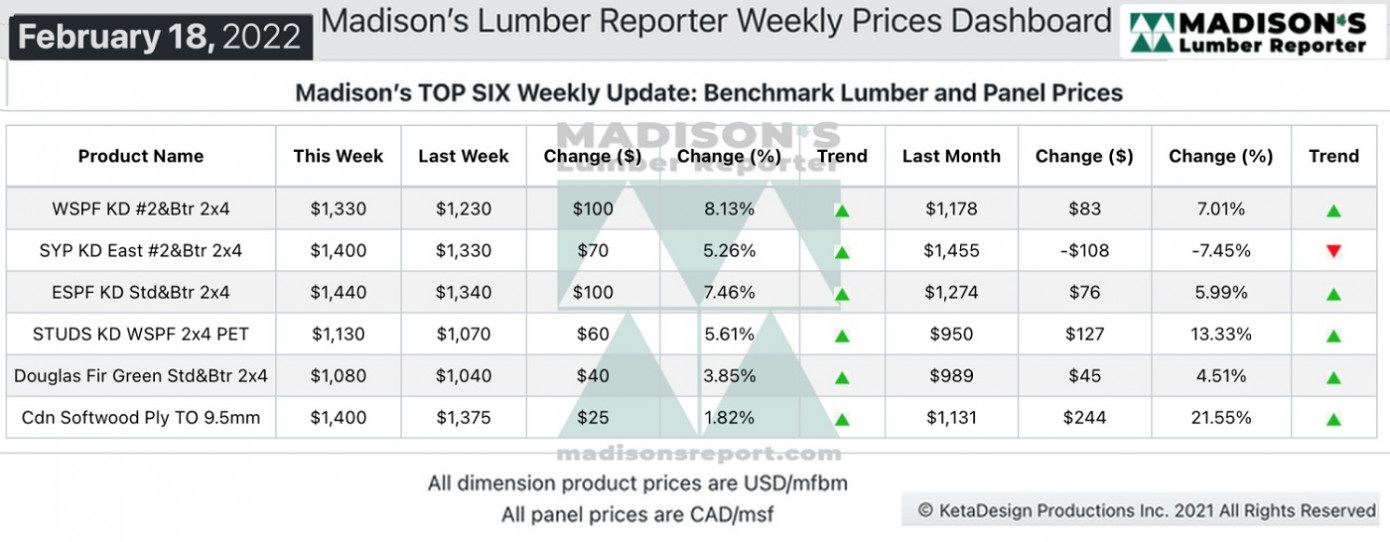

Some items, which had risen too high in recent

weeks – like Southern Yellow Pine 2×4 East Side

– corrected down significantly, to come in line

with similar products. This indicates the market

is finding balance between supply and demand.

The latest US housing starts and new home sales

data shows a slight lull; however permit

applications are up by quite a bit and new house

prices rose yet further in January. As spring

building season comes on over the next couple of

months, there is indication of powerful

underpinnings for continued robust construction

activity.

Most industry folks, whether lumber or housing,

agree that this year will closely match the hot

activity of 2021.

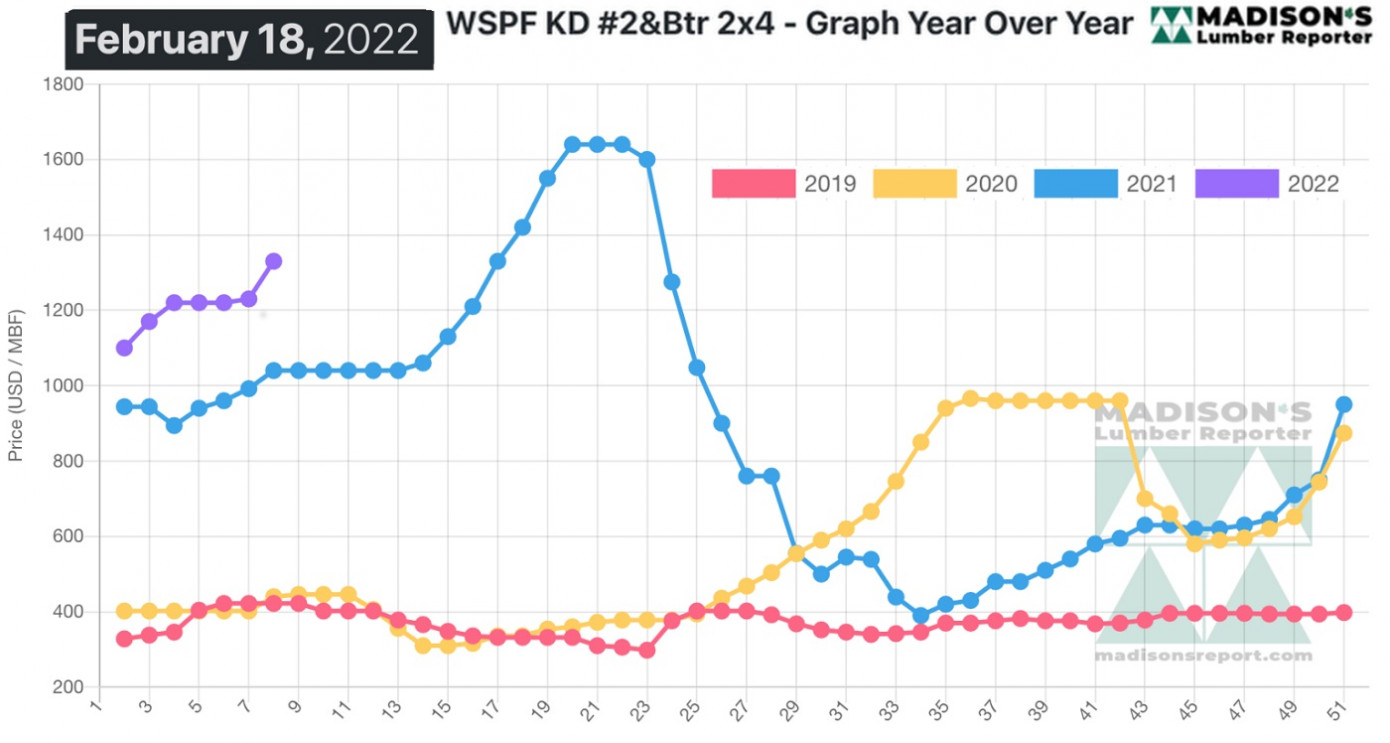

Jumping up further over small gains the previous

week, in the week ending February 18, 2022, the

price of benchmark softwood lumber item Western

Spruce-Pine-Fir 2×4 #2&Btr KD (RL) was US$1,330

mfbm. This is up by +$100, or +8%, from the

previous week when it was $1,230, said forest

products industry price guide newsletter

Madison’s Lumber Reporter.

That week’s price is up by +$153, or +13% from

one month ago when it was $1,178.

Following the early-February sales lull largely precipitated by slumping

futures, US buyers were busy for the past two weeks securing coverage

from Canadian suppliers of Western S-P-F; placing orders for the

remainder of the month and into March.

A ceaseless overall lack of available Western S-P-F lumber and studs in

the US continued to bring buyers back to the table repeatedly. There

remained a pervasive air of caution to every deal however, as no one

could forget the considerable growing pains experienced during a similar

run-up of prices last year at this time.

Both primary and secondary suppliers had their yards picked clean of any

material that came available. Actually moving that volume to market was

another matter entirely.

Robust demand for Western S-P-F commodities persisted, according to

suppliers in Canada. Following the early-February lull largely

precipitated by slumping futures, US buyers were busy for the past two

weeks securing coverage for the remainder of the month and into March.

Reported prices varied from supplier-to-supplier, but any sense of

weakness was gone as all numbers firmed up further.

Sawmills showed increasing confidence as the week wore on, as incoming

demand allowed them to extend order files into early- or mid-March in

most cases.

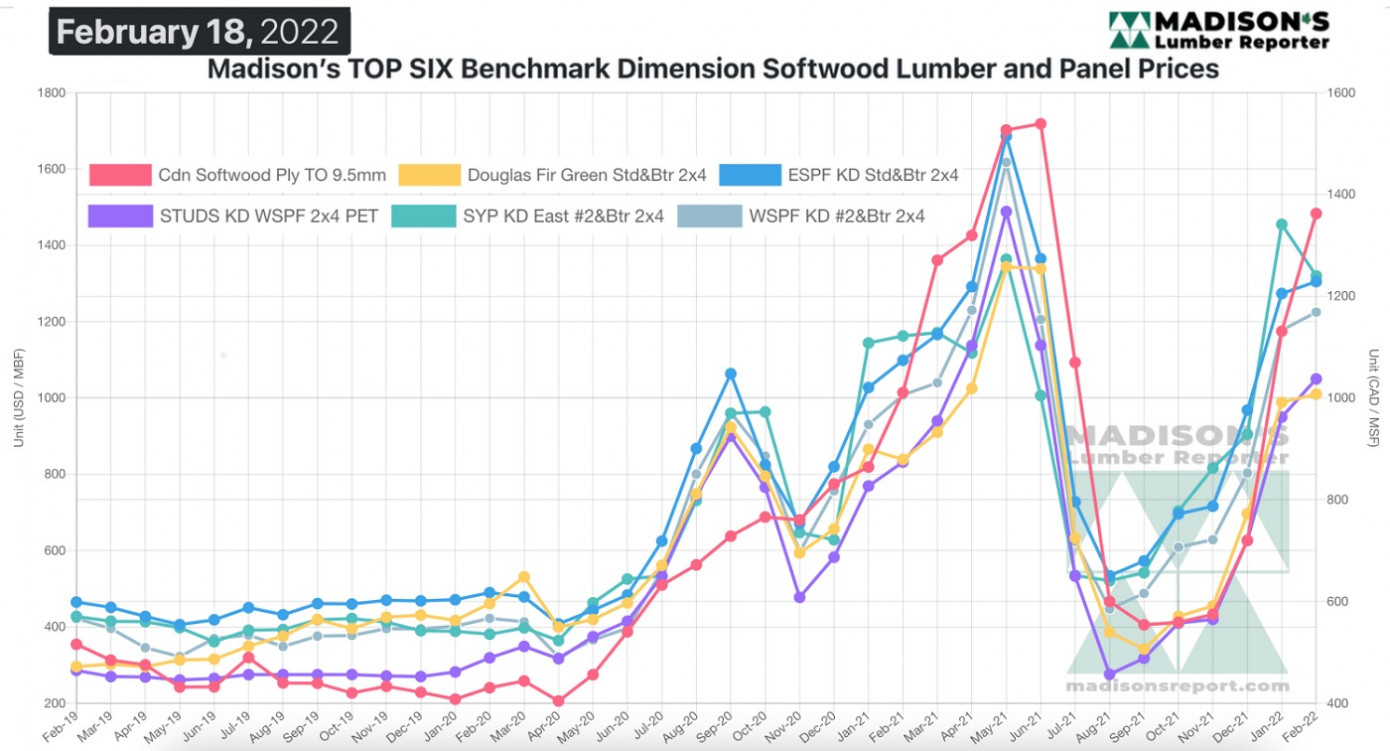

Madison’s Benchmark Top-Six Softwood Lumber and Panel

Prices: Monthly Averages

When compared to the same week last year, when it was US$1,040 mfbm,

for in the week ending February 18, 2022 the price of Western S-P-F is

up by +$290, or +28%. Compared to two years’ ago when it was $440, that

week’s price is up by +$890, or +202%.

-

U.S. & Canada softwood and panel markets - week

6 2022 (Feb

22,

2022)

-

U.S. & Canada softwood and panel markets - week

5 2022 (Feb

15,

2022)

-

U.S. & Canada softwood and panel markets - week

4 2022 (Feb

08,

2022)

-

U.S. & Canada softwood and panel markets - week

3 2022 (Feb

01,

2022)

-

U.S. & Canada softwood and panel markets - week

2 2022 (Jan

25,

2022)

-

U.S. & Canada softwood and panel markets - week

1 2022 (Jan

18,

2022)

-

U.S. & Canada softwood and panel markets - week

47 2021 (Dec

22,

2021)

-

U.S. & Canada softwood and panel markets - week

46 2021 (Dec

15,

2021)

-

U.S. & Canada softwood and panel markets - week

45 2021 (Dec

08,

2021)

-

U.S. & Canada softwood and panel markets - week

44 2021 (Dec

01,

2021)

-

U.S. & Canada softwood and panel markets - week

43 2021 (Nov24,

2021)

-

U.S. & Canada softwood and panel markets - week

42 2021 (Nov17,

2021)

-

U.S. & Canada softwood and panel markets - week

41 2021 (Nov10,

2021)

-

U.S. & Canada softwood and panel markets - week

40 2021 (Nov

03,

2021)

-

U.S. & Canada softwood and panel markets - week

39 2021 (Oct

27,

2021)

-

U.S. & Canada softwood and panel markets - week

38 2021 (Oct

20,

2021)

-

U.S. & Canada softwood and panel markets - week

37 2021 (Oct

13,

2021)

-

U.S. & Canada softwood and panel markets - week

36 2021 (Oct

06,

2021)

-

U.S. & Canada softwood and panel markets - week

35 2021 (Sep

29,

2021)

-

U.S. & Canada softwood and panel markets - week

34 2021 (Sep

22,

2021)

-

U.S. & Canada softwood and panel markets - week

33 2021 (Sep

8,

2021)

-

U.S. & Canada softwood and panel markets - week

32 2021 (Sep

1,

2021)

-

U.S. & Canada softwood and panel markets - week

31 2021 (Aug

25,

2021)

-

U.S. & Canada softwood and panel markets - week

30 2021 (Aug

18,

2021)

-

U.S. & Canada softwood and panel markets - week

29 2021 (Aug

11,

2021)

-

U.S. & Canada softwood and panel markets - week

28 2021 (Aug

04,

2021)

-

U.S. & Canada softwood and panel markets - week

27 2021 (Jul

28,

2021)

-

U.S. & Canada softwood and panel markets - week

26 2021 (Jul

21,

2021)

-

U.S. & Canada softwood and panel markets - week

25 2021 (Jul

14,

2021)

-

U.S. & Canada softwood and panel markets - week

24 2021 (Jul

07,

2021)

-

U.S. & Canada softwood and panel markets - week

23 2021 (Jun

30,

2021)

-

U.S. & Canada softwood and panel markets - week

22 2021 (Jun

23,

2021)

-

U.S. & Canada softwood and panel markets - week

21 2021 (Jun

10,

2021)

-

U.S. & Canada softwood and panel markets - week

20 2021 (Jun

03,

2021)

-

U.S. & Canada softwood and panel markets - week

19 2021 (May

26,

2021)

-

U.S. & Canada softwood and panel markets - week

18 2021 (May

19,

2021)

-

U.S. & Canada softwood and panel markets - week

17 2021 (May

12,

2021)

-

U.S. & Canada softwood and panel markets - week

16 2021 (May

5,

2021)

-

U.S. & Canada softwood and panel markets - week

15 2021 (Apr

28,

2021)

-

U.S. & Canada softwood and panel markets - week

14 2021 (Apr

21,

2021)

-

U.S. & Canada softwood and panel markets - week

13 2021 (Apr

15,

2021)

-

U.S. & Canada softwood and panel markets - week

12 2021 (Apr

8,

2021)

-

U.S. & Canada softwood and panel markets - week

11 2021 (Apr

1,

2021)

-

U.S. & Canada softwood and panel markets - week

10 2021 (Mar

25,

2021)

-

U.S. & Canada softwood and panel markets - week

09 2021 (Mar

17,

2021)

-

U.S. & Canada softwood and panel markets - week

08 2021 (Mar

10,

2021)

-

U.S. & Canada softwood and panel markets - week

07 2021 (Mar

03,

2021)

-

U.S. & Canada softwood and panel markets - week

06 2021 (Feb

24,

2021)

-

U.S. & Canada softwood and panel markets - week

05 2021 (Feb

16,

2021)

-

U.S. & Canada softwood and panel markets - week

04 2021 (Feb

04,

2021)

-

U.S. & Canada softwood and panel markets - week

03 2021 (Jan

29,

2021)

-

U.S.&nb303& Canada softwood and panel markets - week

02 2021 (Jan

22,

2021)

-

U.S. & Canada softwood and panel markets - week

01 2021 (Jan

15,

2021)

-

U.S. & Canada softwood and panel markets - week

49 2020 (Dec

16,

2020)

-

U.S. & Canada softwood and panel markets - week

48 2020 (Dec

09,

2020)

-

U.S. & Canada softwood and panel markets - week

47 2020 (Dec

02,

2020)

-

U.S. & Canada softwood and panel markets - week

46 2020 (Nov

25,

2020)

-

U.S. & Canada softwood and panel markets - week

45 2020 (Nov

18,

2020)

-

U.S. & Canada softwood and panel markets - week

44 2020 (Nov

11,

2020)

-

U.S. & Canada softwood and panel markets - week

43 2020 (Nov

4,

2020)

-

U.S. & Canada softwood and panel markets - week

42 2020 (Oct

28,

2020)

-

U.S. & Canada softwood and panel markets - week

41 2020 (Oct

21,

2020)

-

U.S. & Canada softwood and panel markets - week

40 2020 (Oct

14,

2020)

-

U.S. & Canada softwood and panel markets - week

39, 2020 (Oct

07,

2020)

-

U.S. & Canada softwood and panel markets - week

38, 2020 (Sep

30,

2020)

-

U.S. & Canada softwood and panel markets - week

37, 2020 (Sep

23,

2020)

-

U.S. & Canada softwood and panel markets - week

36, 2020 (Sep

16,

2020)

-

U.S. & Canada softwood and panel markets - week

35, 2020 (Sep

09,

2020)

-

U.S. & Canada softwood and panel markets - week

34, 2020 (Sep

02,

2020)

-

U.S. & Canada softwood and panel markets - week

33, 2020 (Aug

26,

2020)

-

U.S. & Canada softwood and panel markets - week

32, 2020 (Aug

19,

2020)

-

U.S. & Canada softwood and panel markets - week

31, 2020 (Aug

12,

2020)

-

U.S. & Canada softwood and panel markets - week

30, 2020 (Aug

05,

2020)

-

U.S. & Canada softwood and panel markets - week 29, 2020 (Jul

29,

2020)

-

U.S. & Canada softwood and panel markets - week 28, 2020 (Jul

22,

2020)

-

U.S. & Canada softwood and panel markets - week 27, 2020 (Jul

17,

2020)

-

U.S. & Canada softwood and panel markets - week 26, 2020 (Jul

10,

2020)

-

U.S. & Canada softwood and panel markets - week 25, 2020 (Jul

02,

2020)

-

U.S. & Canada softwood and panel markets - week 24, 2020 (Jun

25,

2020)

-

U.S. & Canada softwood and panel markets - week 23, 2020 (Jun

17,

2020)

-

U.S. &

Canada softwood and panel markets - week 22, 2020 (Jun

10,

2020)

-

U.S. &

Canada softwood and panel markets - week 21, 2020 (Jun

3,

2020)

-

U.S. &

Canada softwood and panel markets - week 20, 2020 (May 27,

2020)

-

U.S. &

Canada softwood and panel markets - week 19, 2020 (May 21,

2020)

-

U.S. &

Canada softwood and panel markets - week 18, 2020 (May 15,

2020)

-

U.S. &

Canada softwood and panel markets - week 17, 2020 (May 8,

2020)

-

U.S. &

Canada softwood and panel markets - week 16, 2020 (May 1,

2020)

-

U.S. &

Canada softwood and panel markets - week 15, 2020 (Apr

23,

2020)

-

U.S. &

Canada softwood and panel markets - week 14, 2020 (Apr

17,

2020)

-

U.S. &

Canada softwood and panel markets - week 13, 2020 (Apr

08,

2020)

-

U.S. &

Canada softwood and panel markets - week 12, 2020 (Mar

31,

2020)

-

U.S. &

Canada softwood and panel markets - week 11, 2020 (Mar

24,

2020)

-

U.S. &

Canada softwood and panel markets - week 5, 2020 (Feb

11,

2020)

-

U.S. &

Canada softwood and panel markets - week 4, 2020 (Feb

4,

2020)

-

U.S. &

Canada softwood and panel markets - week 3, 2020 (January

27,

2020)

-

U.S. &

Canada softwood and panel markets - week 2, 2020 (January

20,

2020)

-

U.S. &

Canada softwood and panel markets - week 1, 2020 (January

13,

2020)

-

U.S. &

Canada softwood and panel markets - week 50, 2019 (December

17,

2019)

-

U.S. &

Canada softwood and panel markets - week 49, 2019 (December

10,

2019)

-

U.S. &

Canada softwood and panel markets - week 48, 2019 (December

3,

2019)

-

U.S. &

Canada softwood and panel markets - week 47, 2019 (November

26,

2019)

-

U.S. &

Canada softwood and panel markets - week 46, 2019 (November

19,

2019)

-

U.S. &

Canada softwood and panel markets - week 45, 2019 (November

12,

2019)

-

U.S. &

Canada softwood and panel markets - week 44, 2019 (November

5,

2019)

-

U.S. &

Canada softwood and panel markets - week 43, 2019 ( October

29,

2019)

-

U.S. &

Canada softwood and panel markets - week 42, 2019 ( October

22,

2019)

-

U.S. &

Canada softwood and panel markets - week 41, 2019 ( October

15,

2019)

-

U.S. &

Canada softwood and panel markets - week 40, 2019 ( October

8,

2019)

-

U.S. &

Canada softwood and panel markets - week 39, 2019 ( October

1,

2019)

-

U.S. &

Canada softwood and panel markets - week 38, 2019 ( September 24,

2019)

-

U.S. softwood and panel markets - week 37, 2019 ( September 17,

2019)

-

U.S. softwood and panel markets - week 36, 2019 ( September 10,

2019)

-

U.S. softwood and panel markets - week 35, 2019 ( September 3,

2019)

-

U.S. softwood and panel markets - week 34, 2019 ( August 23,

2019)

-

U.S. softwood and panel markets - week 33, 2019 ( August 16,

2019)

-

U.S. softwood and panel markets - week 32, 2019 ( August 09,

2019)

-

U.S. softwood and panel markets - week 31, 2019 ( August 02,

2019)

-

U.S. softwood and panel markets - week 30, 2019 ( July

26, 2019)

-

U.S. softwood and panel markets - week 29, 2019 ( July 19,

2019)

-

U.S. softwood and panel markets - week 28, 2019 ( July 12,

2019)

-

U.S. softwood and panel markets - week 27, 2019 ( July 03,

2019)

-

U.S. softwood and panel markets - week 26, 2019 ( June 28,

2019)

-

U.S. softwood and panel markets - week 25, 2019 ( June 21,

2019)

-

U.S. softwood and panel markets - week 24, 2019 ( June 14,

2019)

-

U.S. softwood and panel markets - week 23, 2019 ( June 07,

2019)

-

U.S. softwood and panel markets - week 22, 2019 ( May 31,

2019)

-

U.S. softwood and panel markets - week 21, 2019 ( May 24,

2019)

-

U.S. softwood and panel markets - week 20, 2019 ( May 17,

2019)

-

U.S. softwood and panel markets - week 19, 2019 ( May 10,

2019)

-

U.S. softwood and panel markets - week 18, 2019 ( May 03,

2019)

-

U.S. softwood and panel markets - week 17, 2019 ( April 26,

2019)

-

U.S. softwood and panel markets - week 16, 2019 ( April 19,

2019)

-

U.S. softwood and panel markets - week 15, 2019 ( April 12,

2019)

-

U.S. softwood and panel markets - week 14, 2019 ( April 05,

2019)

-

U.S. softwood and panel markets - week 13, 2019 ( March

29, 2019)

-

U.S. softwood and panel markets - week 12, 2019 ( March

22, 2019)

-

U.S. softwood and panel markets - week 11, 2019 ( March

15, 2019)

-

U.S. softwood and panel markets - week 10, 2019 ( March

08, 2019)

-

U.S. softwood and panel markets - week 9, 2019 ( March

01, 2019)

-

U.S. softwood and panel markets - week 8, 2019 ( February.

22, 2019)

-

U.S. softwood and panel markets - week 7, 2019 ( February.

15, 2019)

-

U.S. softwood and panel markets - week 6, 2019 ( February.

08, 2019)

-

U.S. softwood and panel markets - week 5, 2019 ( February.

01, 2019)

-

U.S. softwood and panel markets - week 4, 2019 (January. 25,

2019)

-

U.S. softwood and panel markets - week 3, 2019 (January. 18,

2019)

-

U.S. softwood and panel markets - week 2, 2019 (January. 11,

2019)

-

U.S. softwood and panel markets - week 1, 2019 (January. 04,

2019)

|

|

|