|

Lumber and panel market weekly report ----

Week 41, 2022 |

|

By Madison's Lumber Reporter

As October drew to a close, significant

production curtailments at several large British

Columbia lumber producers helped keep softwood

lumber prices flat. Most of these operators

cited high log costs versus lower lumber prices

as the reason for taking this downtime.

Meanwhile, it seemed that Weyerhaueser and the

union came to an agreement, so the recent lack

of Hemlock and Douglas fir lumber items is

expected to be rectified over the coming month.

These supply constraints, combined with quite

low inventories in the field, provided lumber

sellers with the ability to eschew

counter-offers and stick with their prescribed

price lists for another week, at least.

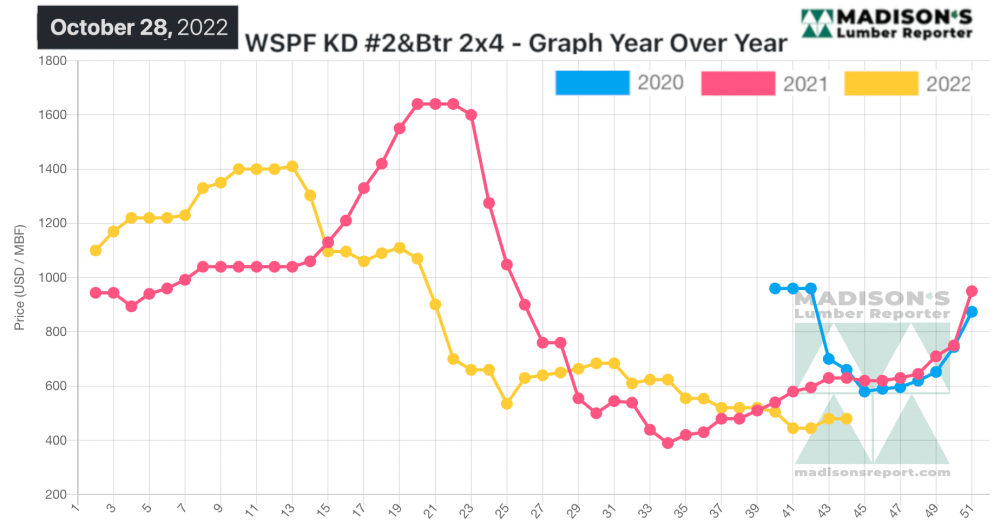

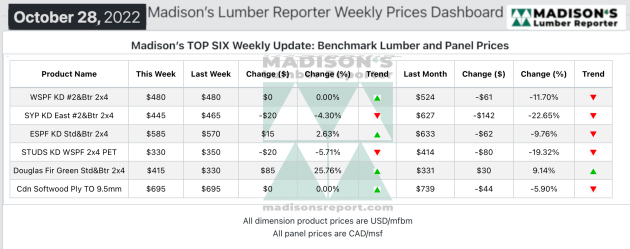

Staying even from the previous week, in the week

ending October 28, the price of benchmark

softwood lumber item Western Spruce-Pine-Fir 2×4

#2&Btr KD (RL) was again US$480 mfbm. This is

down by $44, or 8.0 per cent, from one month ago

when it was $524.

Players all over noted the importance of recent

curtailment announcements from two large B.C.

producers, with that development nudging many

heretofore reticent buyers off the fence.

“ Sales of most commodities continued

to strengthen in a low-key fashion; the Weyco

strike continued to throw the Hem/Fir market for

a loop.” — Madison’s Lumber Reporter

Western S-P-F traders in the United States

reported diminishing sawmill offerings as the

end of October neared. Prices correspondingly

were at or slightly above the previous week’s

levels as sawmills established order files into

the first or second week of November. Six-inch

dimension was in comparatively high demand.

Persistently-depleted field inventories across

the board were another incentive to get deals

done. Demand for low grade commodities lagged

behind that of #2&Btr.

Sneaky strong demand kept Canadian suppliers of

Western S-P-F lumber busy, thanks in large part

to momentum generated by recent curtailment

announcements from two major producers in

Western Canada. Sawmill lists were light to

start the week and only dwindled from there.

Buyers tried to remain cautious and focus on LTL

deals through the distribution network, but

availability there was drying up also. Asking

prices on #2&Btr and High Line dimension items

were flat from the previous week’s levels, or

climbed between $10 and $30, as producers were

firm on their numbers and no longer amenable to

counter-offers.

“ Demand for Western S-P-F studs rode

a continued undercurrent of strength according

to Canadian suppliers, even if it lagged behind

that of dimension. Mills maintained firm pricing

on six-inch trims while 2×4-8’s and -9’s came

off $20 and $10 respectively. Buyers remained

hesitant to cover more than their immediate

needs, with hand-to-mouth purchasing still the

most common strategy. Wholesalers and

distributers were busier than mills again, and

inventory among all suppliers was getting

tighter with each passing week. Strong order

files into mid-November and dwindling

availability appeared to underscore the

strengthening position of producers.” —

Madison’s Lumber Reporter

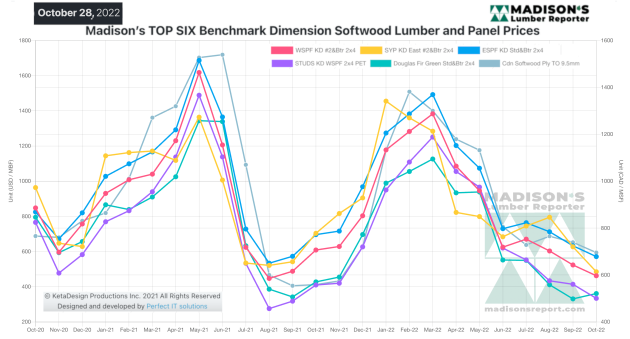

Madison’s Benchmark Top-Six Softwood Lumber and Panel

Prices: Monthly Averages

Compared to the same week last year, when it was US$630 mfbm, the price

of Western Spruce-Pine-Fir 2×4 #2&Btr KD (RL) for the week ending

October 28 was down by $150, or 24 per cent. Compared to two years ago

when it was $660, that week’s price is down by $180, or 27 per cent.

-

U.S. & Canada softwood and panel markets - week

40 2022 (Nov

02,

2022)

-

U.S. & Canada softwood and panel markets - week

39 2022 (Oct

11,

2022)

-

U.S. & Canada softwood and panel markets - week 38 2022 (Oct

04,

2022)

-

U.S. & Canada softwood and panel markets - week 37 2022 (Sep

28,

2022)

-

U.S. & Canada softwood and panel markets - week 36 2022 (Sep

20,

2022)

-

U.S. & Canada softwood and panel markets - week 35 2022 (Sep

13,

2022)

-

U.S. & Canada softwood and panel markets - week 34 2022 (Sep

06,

2022)

-

U.S. & Canada softwood and panel markets - week 33 2022 (Aug

30,

2022)

-

U.S. & Canada softwood and panel markets - week 32 2022 (Aug

23,

2022)

-

U.S. & Canada softwood and panel markets - week 31 2022 (Aug

16,

2022)

-

U.S. & Canada softwood and panel markets - week 30 2022 (Aug

09,

2022)

-

U.S. & Canada softwood and panel markets - week 29 2022 (Aug

02,

2022)

-

U.S. & Canada softwood and panel markets - week 28 2022 (Jul

26,

2022)

-

U.S. & Canada softwood and panel markets - week 27 2022 (Jul

19,

2022)

-

U.S. & Canada softwood and panel markets - week 26 2022 (Jul

12,

2022)

-

U.S. & Canada softwood and panel markets - week 25 2022 (Jul

05,

2022)

-

U.S. & Canada softwood and panel markets - week 24 2022 (Jun

29,

2022)

-

U.S. & Canada softwood and panel markets - week 23 2022 (Jun

22,

2022)

-

U.S. & Canada softwood and panel markets - week 22 2022 (Jun

15,

2022)

-

U.S. & Canada softwood and panel markets - week 21 2022 (Jun

08,

2022)

-

U.S. & Canada softwood and panel markets - week 20 2022 (Jun

01,

2022)

-

U.S. & Canada softwood and panel markets - week 19 2022 (May

25,

2022)

-

U.S. & Canada softwood and panel markets - week 18 2022 (May

18,

2022)

-

U.S. & Canada softwood and panel markets - week 17 2022 (May

11,

2022)

-

U.S. & Canada softwood and panel markets - week 16 2022 (May

04,

2022)

-

U.S. & Canada softwood and panel markets - week 15 2022 (Apr

26,

2022)

-

U.S. & Canada softwood and panel markets - week 14 2022 (Apr

19,

2022)

-

U.S. & Canada softwood and panel markets - week 13 2022 (Apr

12,

2022)

-

U.S. & Canada softwood and panel markets - week 12 2022 (Apr

05,

2022)

-

U.S. & Canada softwood and panel markets - week 11 2022 (Mar

29,

2022)

-

U.S. & Canada softwood and panel markets - week 10 2022 (Mar

22,

2022)

-

U.S. & Canada softwood and panel markets - week 9 2022 (Mar

15,

2022)

-

U.S. & Canada softwood and panel markets - week 8 2022 (Mar

08,

2022)

-

U.S. & Canada softwood and panel markets - week 7 2022 (Mar

01,

2022)

-

U.S. & Canada softwood and panel markets - week 6 2022 (Feb

22,

2022)

-

U.S. & Canada softwood and panel markets - week 5 2022 (Feb

15,

2022)

-

U.S. & Canada softwood and panel markets - week 4 2022 (Feb

08,

2022)

-

U.S. & Canada softwood and panel markets - week 3 2022 (Feb

01,

2022)

-

U.S. & Canada softwood and panel markets - week 2 2022 (Jan

25,

2022)

-

U.S. & Canada softwood and panel markets - week 1 2022 (Jan

18,

2022)

-

U.S. & Canada softwood and panel markets - week 47 2021 (Dec

22,

2021)

-

U.S. & Canada softwood and panel markets - week 46 2021 (Dec

15,

2021)

-

U.S. & Canada softwood and panel markets - week 45 2021 (Dec

08,

2021)

-

U.S. & Canada softwood and panel markets - week 44 2021 (Dec

01,

2021)

-

U.S. & Canada softwood and panel markets - week 43 2021 (Nov24,

2021)

-

U.S. & Canada softwood and panel markets - week 42 2021 (Nov17,

2021)

-

U.S. & Canada softwood and panel markets - week 41 2021 (Nov10,

2021)

-

U.S. & Canada softwood and panel markets - week 40 2021 (Nov

03,

2021)

-

U.S. & Canada softwood and panel markets - week 39 2021 (Oct

27,

2021)

-

U.S. & Canada softwood and panel markets - week 38 2021 (Oct

20,

2021)

-

U.S. & Canada softwood and panel markets - week 37 2021 (Oct

13,

2021)

-

U.S. & Canada softwood and panel markets - week 36 2021 (Oct

06,

2021)

-

U.S. & Canada softwood and panel markets - week 35 2021 (Sep

29,

2021)

-

U.S. & Canada softwood and panel markets - week 34 2021 (Sep

22,

2021)

-

U.S. & Canada softwood and panel markets - week 33 2021 (Sep

8,

2021)

-

U.S. & Canada softwood and panel markets - week 32 2021 (Sep

1,

2021)

-

U.S. & Canada softwood and panel markets - week 31 2021 (Aug

25,

2021)

-

U.S. & Canada softwood and panel markets - week 30 2021 (Aug

18,

2021)

-

U.S. & Canada softwood and panel markets - week 29 2021 (Aug

11,

2021)

-

U.S. & Canada softwood and panel markets - week 28 2021 (Aug

04,

2021)

-

U.S. & Canada softwood and panel markets - week 27 2021 (Jul

28,

2021)

-

U.S. & Canada softwood and panel markets - week 26 2021 (Jul

21,

2021)

-

U.S. & Canada softwood and panel markets - week 25 2021 (Jul

14,

2021)

-

U.S. & Canada softwood and panel markets - week 24 2021 (Jul

07,

2021)

-

U.S. & Canada softwood and panel markets - week 23 2021 (Jun

30,

2021)

-

U.S. & Canada softwood and panel markets - week 22 2021 (Jun

23,

2021)

-

U.S. & Canada softwood and panel markets - week 21 2021 (Jun

10,

2021)

-

U.S. & Canada softwood and panel markets - week 20 2021 (Jun

03,

2021)

-

U.S. & Canada softwood and panel markets - week 19 2021 (May

26,

2021)

-

U.S. & Canada softwood and panel markets - week 18 2021 (May

19,

2021)

-

U.S. & Canada softwood and panel markets - week 17 2021 (May

12,

2021)

-

U.S. & Canada softwood and panel markets - week 16 2021 (May

5,

2021)

-

U.S. & Canada softwood and panel markets - week 15 2021 (Apr

28,

2021)

-

U.S. & Canada softwood and panel markets - week 14 2021 (Apr

21,

2021)

-

U.S. & Canada softwood and panel markets - week 13 2021 (Apr

15,

2021)

-

U.S. & Canada softwood and panel markets - week 12 2021 (Apr

8,

2021)

-

U.S. & Canada softwood and panel markets - week 11 2021 (Apr

1,

2021)

-

U.S. & Canada softwood and panel markets - week 10 2021 (Mar

25,

2021)

-

U.S. & Canada softwood and panel markets - week 09 2021 (Mar

17,

2021)

-

U.S. & Canada softwood and panel markets - week 08 2021 (Mar

10,

2021)

-

U.S. & Canada softwood and panel markets - week 07 2021 (Mar

03,

2021)

-

U.S. & Canada softwood and panel markets - week 06 2021 (Feb

24,

2021)

-

U.S. & Canada softwood and panel markets - week 05 2021 (Feb

16,

2021)

-

U.S. & Canada softwood and panel markets - week 04 2021 (Feb

04,

2021)

-

U.S. & Canada softwood and panel markets - week 03 2021 (Jan

29,

2021)

-

U.S.&nb303& Canada softwood and panel markets - week 02 2021 (Jan

22,

2021)

-

U.S. & Canada softwood and panel markets - week 01 2021 (Jan

15,

2021)

-

U.S. & Canada softwood and panel markets - week 49 2020 (Dec

16,

2020)

-

U.S. & Canada softwood and panel markets - week 48 2020 (Dec

09,

2020)

-

U.S. & Canada softwood and panel markets - week 47 2020 (Dec

02,

2020)

-

U.S. & Canada softwood and panel markets - week 46 2020 (Nov

25,

2020)

-

U.S. & Canada softwood and panel markets - week 45 2020 (Nov

18,

2020)

-

U.S. & Canada softwood and panel markets - week 44 2020 (Nov

11,

2020)

-

U.S. & Canada softwood and panel markets - week 43 2020 (Nov

4,

2020)

-

U.S. & Canada softwood and panel markets - week 42 2020 (Oct

28,

2020)

-

U.S. & Canada softwood and panel markets - week 41 2020 (Oct

21,

2020)

-

U.S. & Canada softwood and panel markets - week 40 2020 (Oct

14,

2020)

-

U.S. & Canada softwood and panel markets - week 39, 2020 (Oct

07,

2020)

-

U.S. & Canada softwood and panel markets - week 38, 2020 (Sep

30,

2020)

-

U.S. & Canada softwood and panel markets - week 37, 2020 (Sep

23,

2020)

-

U.S. & Canada softwood and panel markets - week 36, 2020 (Sep

16,

2020)

-

U.S. & Canada softwood and panel markets - week 35, 2020 (Sep

09,

2020)

-

U.S. & Canada softwood and panel markets - week 34, 2020 (Sep

02,

2020)

-

U.S. & Canada softwood and panel markets - week 33, 2020 (Aug

26,

2020)

-

U.S. & Canada softwood and panel markets - week 32, 2020 (Aug

19,

2020)

-

U.S. & Canada softwood and panel markets - week 31, 2020 (Aug

12,

2020)

-

U.S. & Canada softwood and panel markets - week 30, 2020 (Aug

05,

2020)

-

U.S. & Canada softwood and panel markets - week 29, 2020 (Jul

29,

2020)

-

U.S. & Canada softwood and panel markets - week 28, 2020 (Jul

22,

2020)

-

U.S. & Canada softwood and panel markets - week 27, 2020 (Jul

17,

2020)

-

U.S. & Canada softwood and panel markets - week 26, 2020 (Jul

10,

2020)

-

U.S. & Canada softwood and panel markets - week 25, 2020 (Jul

02,

2020)

-

U.S. & Canada softwood and panel markets - week 24, 2020 (Jun

25,

2020)

-

U.S. & Canada softwood and panel markets - week 23, 2020 (Jun

17,

2020)

-

U.S. & Canada softwood and panel markets - week 22, 2020 (Jun

10, 2020)

-

U.S. & Canada softwood and panel markets - week 21, 2020 (Jun

3, 2020)

-

U.S. & Canada softwood and panel markets - week 20, 2020 (May 27,

2020)

-

U.S. & Canada softwood and panel markets - week 19, 2020 (May 21,

2020)

-

U.S. & Canada softwood and panel markets - week 18, 2020 (May 15,

2020)

-

U.S. & Canada softwood and panel markets - week 17, 2020 (May 8,

2020)

-

U.S. & Canada softwood and panel markets - week 16, 2020 (May 1,

2020)

-

U.S. & Canada softwood and panel markets - week 15, 2020 (Apr

23,

2020)

-

U.S. & Canada softwood and panel markets - week 14, 2020 (Apr

17, 2020)

-

U.S. & Canada softwood and panel markets - week 13, 2020 (Apr

08, 2020)

-

U.S. & Canada softwood and panel markets - week 12, 2020 (Mar

31, 2020)

-

U.S. & Canada softwood and panel markets - week 11, 2020 (Mar

24,

2020)

-

U.S. & Canada softwood and panel markets - week 5, 2020 (Feb

11,

2020)

-

U.S. & Canada softwood and panel markets - week 4, 2020 (Feb

4, 2020)

-

U.S. & Canada softwood and panel markets - week 3, 2020 (January

27,

2020)

-

U.S. & Canada softwood and panel markets - week 2, 2020 (January

20,

2020)

-

U.S. & Canada softwood and panel markets - week 1, 2020 (January

13,

2020)

-

U.S. & Canada softwood and panel markets - week 50, 2019 (December

17,

2019)

-

U.S. & Canada softwood and panel markets - week 49, 2019 (December

10,

2019)

-

U.S. & Canada softwood and panel markets - week 48, 2019 (December

3, 2019)

-

U.S. & Canada softwood and panel markets - week 47, 2019 (November

26, 2019)

-

U.S. & Canada softwood and panel markets - week 46, 2019 (November

19, 2019)

-

U.S. & Canada softwood and panel markets - week 45, 2019 (November

12, 2019)

-

U.S. & Canada softwood and panel markets - week 44, 2019 (November

5, 2019)

-

U.S. & Canada softwood and panel markets - week 43, 2019 ( October

29, 2019)

-

U.S. & Canada softwood and panel markets - week 42, 2019 ( October

22, 2019)

-

U.S. & Canada softwood and panel markets - week 41, 2019 ( October

15, 2019)

-

U.S. & Canada softwood and panel markets - week 40, 2019 ( October

8, 2019)

-

U.S. & Canada softwood and panel markets - week 39, 2019 ( October

1, 2019)

-

U.S. & Canada softwood and panel markets - week 38, 2019 ( September 24,

2019)

-

U.S. softwood and panel markets - week 37, 2019 ( September 17,

2019)

-

U.S. softwood and panel markets - week 36, 2019 ( September 10,

2019)

-

U.S. softwood and panel markets - week 35, 2019 ( September 3,

2019)

-

U.S. softwood and panel markets - week 34, 2019 ( August 23,

2019)

-

U.S. softwood and panel markets - week 33, 2019 ( August 16,

2019)

-

U.S. softwood and panel markets - week 32, 2019 ( August 09,

2019)

-

U.S. softwood and panel markets - week 31, 2019 ( August 02,

2019)

-

U.S. softwood and panel markets - week 30, 2019 ( July

26, 2019)

-

U.S. softwood and panel markets - week 29, 2019 ( July 19,

2019)

-

U.S. softwood and panel markets - week 28, 2019 ( July 12,

2019)

-

U.S. softwood and panel markets - week 27, 2019 ( July 03,

2019)

-

U.S. softwood and panel markets - week 26, 2019 ( June 28,

2019)

-

U.S. softwood and panel markets - week 25, 2019 ( June 21,

2019)

-

U.S. softwood and panel markets - week 24, 2019 ( June 14,

2019)

-

U.S. softwood and panel markets - week 23, 2019 ( June 07,

2019)

-

U.S. softwood and panel markets - week 22, 2019 ( May 31,

2019)

-

U.S. softwood and panel markets - week 21, 2019 ( May 24,

2019)

-

U.S. softwood and panel markets - week 20, 2019 ( May 17,

2019)

-

U.S. softwood and panel markets - week 19, 2019 ( May 10,

2019)

-

U.S. softwood and panel markets - week 18, 2019 ( May 03,

2019)

-

U.S. softwood and panel markets - week 17, 2019 ( April 26,

2019)

-

U.S. softwood and panel markets - week 16, 2019 ( April 19,

2019)

-

U.S. softwood and panel markets - week 15, 2019 ( April 12,

2019)

-

U.S. softwood and panel markets - week 14, 2019 ( April 05,

2019)

-

U.S. softwood and panel markets - week 13, 2019 ( March

29, 2019)

-

U.S. softwood and panel markets - week 12, 2019 ( March

22, 2019)

-

U.S. softwood and panel markets - week 11, 2019 ( March

15, 2019)

-

U.S. softwood and panel markets - week 10, 2019 ( March

08, 2019)

-

U.S. softwood and panel markets - week 9, 2019 ( March

01, 2019)

-

U.S. softwood and panel markets - week 8, 2019 ( February.

22, 2019)

-

U.S. softwood and panel markets - week 7, 2019 ( February.

15, 2019)

-

U.S. softwood and panel markets - week 6, 2019 ( February.

08, 2019)

-

U.S. softwood and panel markets - week 5, 2019 ( February.

01, 2019)

-

U.S. softwood and panel markets - week 4, 2019 (January. 25,

2019)

-

U.S. softwood and panel markets - week 3, 2019 (January. 18,

2019)

-

U.S. softwood and panel markets - week 2, 2019 (January. 11,

2019)

-

U.S. softwood and panel markets - week 1, 2019 (January. 04,

2019)

|

|

|