|

Lumber and panel market weekly report ----

Week 42, 2022 |

|

By Madison's Lumber Reporter

The beginning of November brought a slight

firming up for lumber prices, due to recent

sawmills curtailments — especially in British

Columbia — and ongoing reasonable sales volumes.

Customers found inventories in the field quite

scarce thus had to come back to producers for

their purchases. As the usual seasonal slowdown

is upon us, and lumber demand historically

starts to wane at this time of year, sawmills

start to plan for lowering manufacturing volumes

into the winter and year end. As such, suppliers

were able to pop prices up a little bit, to

satisfy the immediate needs of buyers.

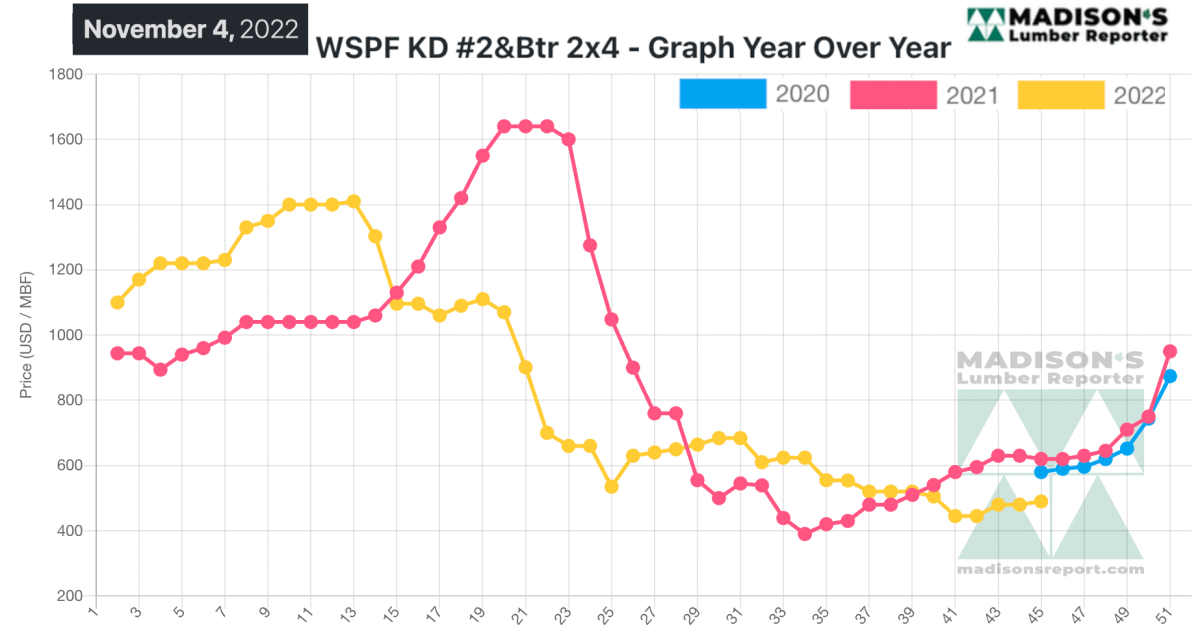

Popping up slightly from the previous week, in

the week ending November 4, the price of

benchmark softwood lumber item Western

Spruce-Pine-Fir 2×4 #2&Btr KD (RL) was US$490

mfbm, said weekly forest products industry price

guide newsletter Madison’s Lumber Reporter. This

is up by $10 or 2.0 per cent from the previous

week when it was $480, and is up by $28, or 6.0

per cent, from one month ago when it was $463.

Demand generated by recent curtailment

announcements from major Western S-P-F producers

seemed all but gone according to traders.

“After a busy October, demand for North American

solid wood commodities took a breather to start

November.” — Madison’s Lumber Reporter

Western S-P-F buyers in the United States were

more circumspect in their dealings than during

most of October. Rather than jumping back into

the market immediately, most sat on the

sidelines and assessed their current inventory

positions and subsequent needs through the

remainder of 2022. Customers who were active in

the market confined their buying forays to the

distribution network for the most part, as they

sought immediate coverage with more reliable

shipping timelines. The pullback in demand from

noncommittal buyers in multifamily, tract, and

mixed commercial construction was noticeable.

Mid- to -late-November order files were reported

by sawmills.

Canadian suppliers of Western S-P-F lumber were

less busy as the general tone in the market

turned insular in consonance with the arrival of

November. The looming spectre of winter was a

big factor, with much of the conversation

centered around battening down the hatches in

response to the change in weather. Sawmill sales

lists were thin and getting thinner, but

faltering buyer activity was more in line with

availability. Sawmill order files were in the

range of two- to three-weeks.

“ Eastern Canadian traders described

a tentative market, as November began with many

buyers turned to the task of processing incoming

orders rather than pursuing further coverage.

Producers kept their dimension lumber asking

prices at or on either side of last week’s

levels. Good demand and takeaway over the past

two weeks allowed sawmills to build up strong

three-week order files in advance of this

comparative quietude.” — Madison’s Lumber

Reporter

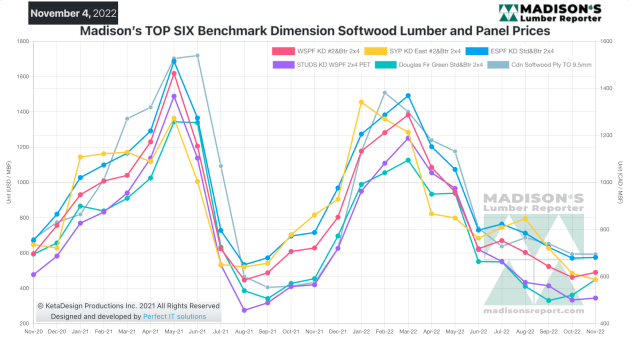

Madison’s Benchmark Top-Six Softwood Lumber and Panel

Prices: Monthly Averages

Compared to the same week last year, when it was US$620 mfbm, the price

of Western Spruce-Pine-Fir 2×4 #2&Btr KD (RL) for the week ending

November 4, was down by $130, or 21 per cent. Compared to two years ago

when it was $580, that week’s price is down by 980, or 16 per cent.

-

U.S. & Canada softwood and panel markets - week

41 2022 (Nov

08,

2022)

-

U.S. & Canada softwood and panel markets - week

40 2022 (Nov

02,

2022)

-

U.S. & Canada softwood and panel markets - week

39 2022 (Oct

11,

2022)

-

U.S. & Canada softwood and panel markets - week 38 2022 (Oct

04,

2022)

-

U.S. & Canada softwood and panel markets - week 37 2022 (Sep

28,

2022)

-

U.S. & Canada softwood and panel markets - week 36 2022 (Sep

20,

2022)

-

U.S. & Canada softwood and panel markets - week 35 2022 (Sep

13,

2022)

-

U.S. & Canada softwood and panel markets - week 34 2022 (Sep

06,

2022)

-

U.S. & Canada softwood and panel markets - week 33 2022 (Aug

30,

2022)

-

U.S. & Canada softwood and panel markets - week 32 2022 (Aug

23,

2022)

-

U.S. & Canada softwood and panel markets - week 31 2022 (Aug

16,

2022)

-

U.S. & Canada softwood and panel markets - week 30 2022 (Aug

09,

2022)

-

U.S. & Canada softwood and panel markets - week 29 2022 (Aug

02,

2022)

-

U.S. & Canada softwood and panel markets - week 28 2022 (Jul

26,

2022)

-

U.S. & Canada softwood and panel markets - week 27 2022 (Jul

19,

2022)

-

U.S. & Canada softwood and panel markets - week 26 2022 (Jul

12,

2022)

-

U.S. & Canada softwood and panel markets - week 25 2022 (Jul

05,

2022)

-

U.S. & Canada softwood and panel markets - week 24 2022 (Jun

29,

2022)

-

U.S. & Canada softwood and panel markets - week 23 2022 (Jun

22,

2022)

-

U.S. & Canada softwood and panel markets - week 22 2022 (Jun

15,

2022)

-

U.S. & Canada softwood and panel markets - week 21 2022 (Jun

08,

2022)

-

U.S. & Canada softwood and panel markets - week 20 2022 (Jun

01,

2022)

-

U.S. & Canada softwood and panel markets - week 19 2022 (May

25,

2022)

-

U.S. & Canada softwood and panel markets - week 18 2022 (May

18,

2022)

-

U.S. & Canada softwood and panel markets - week 17 2022 (May

11,

2022)

-

U.S. & Canada softwood and panel markets - week 16 2022 (May

04,

2022)

-

U.S. & Canada softwood and panel markets - week 15 2022 (Apr

26,

2022)

-

U.S. & Canada softwood and panel markets - week 14 2022 (Apr

19,

2022)

-

U.S. & Canada softwood and panel markets - week 13 2022 (Apr

12,

2022)

-

U.S. & Canada softwood and panel markets - week 12 2022 (Apr

05,

2022)

-

U.S. & Canada softwood and panel markets - week 11 2022 (Mar

29,

2022)

-

U.S. & Canada softwood and panel markets - week 10 2022 (Mar

22,

2022)

-

U.S. & Canada softwood and panel markets - week 9 2022 (Mar

15,

2022)

-

U.S. & Canada softwood and panel markets - week 8 2022 (Mar

08,

2022)

-

U.S. & Canada softwood and panel markets - week 7 2022 (Mar

01,

2022)

-

U.S. & Canada softwood and panel markets - week 6 2022 (Feb

22,

2022)

-

U.S. & Canada softwood and panel markets - week 5 2022 (Feb

15,

2022)

-

U.S. & Canada softwood and panel markets - week 4 2022 (Feb

08,

2022)

-

U.S. & Canada softwood and panel markets - week 3 2022 (Feb

01,

2022)

-

U.S. & Canada softwood and panel markets - week 2 2022 (Jan

25,

2022)

-

U.S. & Canada softwood and panel markets - week 1 2022 (Jan

18,

2022)

-

U.S. & Canada softwood and panel markets - week 47 2021 (Dec

22,

2021)

-

U.S. & Canada softwood and panel markets - week 46 2021 (Dec

15,

2021)

-

U.S. & Canada softwood and panel markets - week 45 2021 (Dec

08,

2021)

-

U.S. & Canada softwood and panel markets - week 44 2021 (Dec

01,

2021)

-

U.S. & Canada softwood and panel markets - week 43 2021 (Nov24,

2021)

-

U.S. & Canada softwood and panel markets - week 42 2021 (Nov17,

2021)

-

U.S. & Canada softwood and panel markets - week 41 2021 (Nov10,

2021)

-

U.S. & Canada softwood and panel markets - week 40 2021 (Nov

03,

2021)

-

U.S. & Canada softwood and panel markets - week 39 2021 (Oct

27,

2021)

-

U.S. & Canada softwood and panel markets - week 38 2021 (Oct

20,

2021)

-

U.S. & Canada softwood and panel markets - week 37 2021 (Oct

13,

2021)

-

U.S. & Canada softwood and panel markets - week 36 2021 (Oct

06,

2021)

-

U.S. & Canada softwood and panel markets - week 35 2021 (Sep

29,

2021)

-

U.S. & Canada softwood and panel markets - week 34 2021 (Sep

22,

2021)

-

U.S. & Canada softwood and panel markets - week 33 2021 (Sep

8,

2021)

-

U.S. & Canada softwood and panel markets - week 32 2021 (Sep

1,

2021)

-

U.S. & Canada softwood and panel markets - week 31 2021 (Aug

25,

2021)

-

U.S. & Canada softwood and panel markets - week 30 2021 (Aug

18,

2021)

-

U.S. & Canada softwood and panel markets - week 29 2021 (Aug

11,

2021)

-

U.S. & Canada softwood and panel markets - week 28 2021 (Aug

04,

2021)

-

U.S. & Canada softwood and panel markets - week 27 2021 (Jul

28,

2021)

-

U.S. & Canada softwood and panel markets - week 26 2021 (Jul

21,

2021)

-

U.S. & Canada softwood and panel markets - week 25 2021 (Jul

14,

2021)

-

U.S. & Canada softwood and panel markets - week 24 2021 (Jul

07,

2021)

-

U.S. & Canada softwood and panel markets - week 23 2021 (Jun

30,

2021)

-

U.S. & Canada softwood and panel markets - week 22 2021 (Jun

23,

2021)

-

U.S. & Canada softwood and panel markets - week 21 2021 (Jun

10,

2021)

-

U.S. & Canada softwood and panel markets - week 20 2021 (Jun

03,

2021)

-

U.S. & Canada softwood and panel markets - week 19 2021 (May

26,

2021)

-

U.S. & Canada softwood and panel markets - week 18 2021 (May

19,

2021)

-

U.S. & Canada softwood and panel markets - week 17 2021 (May

12,

2021)

-

U.S. & Canada softwood and panel markets - week 16 2021 (May

5,

2021)

-

U.S. & Canada softwood and panel markets - week 15 2021 (Apr

28,

2021)

-

U.S. & Canada softwood and panel markets - week 14 2021 (Apr

21,

2021)

-

U.S. & Canada softwood and panel markets - week 13 2021 (Apr

15,

2021)

-

U.S. & Canada softwood and panel markets - week 12 2021 (Apr

8,

2021)

-

U.S. & Canada softwood and panel markets - week 11 2021 (Apr

1,

2021)

-

U.S. & Canada softwood and panel markets - week 10 2021 (Mar

25,

2021)

-

U.S. & Canada softwood and panel markets - week 09 2021 (Mar

17,

2021)

-

U.S. & Canada softwood and panel markets - week 08 2021 (Mar

10,

2021)

-

U.S. & Canada softwood and panel markets - week 07 2021 (Mar

03,

2021)

-

U.S. & Canada softwood and panel markets - week 06 2021 (Feb

24,

2021)

-

U.S. & Canada softwood and panel markets - week 05 2021 (Feb

16,

2021)

-

U.S. & Canada softwood and panel markets - week 04 2021 (Feb

04,

2021)

-

U.S. & Canada softwood and panel markets - week 03 2021 (Jan

29,

2021)

-

U.S.&nb303& Canada softwood and panel markets - week 02 2021 (Jan

22,

2021)

-

U.S. & Canada softwood and panel markets - week 01 2021 (Jan

15,

2021)

-

U.S. & Canada softwood and panel markets - week 49 2020 (Dec

16,

2020)

-

U.S. & Canada softwood and panel markets - week 48 2020 (Dec

09,

2020)

-

U.S. & Canada softwood and panel markets - week 47 2020 (Dec

02,

2020)

-

U.S. & Canada softwood and panel markets - week 46 2020 (Nov

25,

2020)

-

U.S. & Canada softwood and panel markets - week 45 2020 (Nov

18,

2020)

-

U.S. & Canada softwood and panel markets - week 44 2020 (Nov

11,

2020)

-

U.S. & Canada softwood and panel markets - week 43 2020 (Nov

4,

2020)

-

U.S. & Canada softwood and panel markets - week 42 2020 (Oct

28,

2020)

-

U.S. & Canada softwood and panel markets - week 41 2020 (Oct

21,

2020)

-

U.S. & Canada softwood and panel markets - week 40 2020 (Oct

14,

2020)

-

U.S. & Canada softwood and panel markets - week 39, 2020 (Oct

07,

2020)

-

U.S. & Canada softwood and panel markets - week 38, 2020 (Sep

30,

2020)

-

U.S. & Canada softwood and panel markets - week 37, 2020 (Sep

23,

2020)

-

U.S. & Canada softwood and panel markets - week 36, 2020 (Sep

16,

2020)

-

U.S. & Canada softwood and panel markets - week 35, 2020 (Sep

09,

2020)

-

U.S. & Canada softwood and panel markets - week 34, 2020 (Sep

02,

2020)

-

U.S. & Canada softwood and panel markets - week 33, 2020 (Aug

26,

2020)

-

U.S. & Canada softwood and panel markets - week 32, 2020 (Aug

19,

2020)

-

U.S. & Canada softwood and panel markets - week 31, 2020 (Aug

12,

2020)

-

U.S. & Canada softwood and panel markets - week 30, 2020 (Aug

05,

2020)

-

U.S. & Canada softwood and panel markets - week 29, 2020 (Jul

29,

2020)

-

U.S. & Canada softwood and panel markets - week 28, 2020 (Jul

22,

2020)

-

U.S. & Canada softwood and panel markets - week 27, 2020 (Jul

17,

2020)

-

U.S. & Canada softwood and panel markets - week 26, 2020 (Jul

10,

2020)

-

U.S. & Canada softwood and panel markets - week 25, 2020 (Jul

02,

2020)

-

U.S. & Canada softwood and panel markets - week 24, 2020 (Jun

25,

2020)

-

U.S. & Canada softwood and panel markets - week 23, 2020 (Jun

17,

2020)

-

U.S. & Canada softwood and panel markets - week 22, 2020 (Jun

10, 2020)

-

U.S. & Canada softwood and panel markets - week 21, 2020 (Jun

3, 2020)

-

U.S. & Canada softwood and panel markets - week 20, 2020 (May 27,

2020)

-

U.S. & Canada softwood and panel markets - week 19, 2020 (May 21,

2020)

-

U.S. & Canada softwood and panel markets - week 18, 2020 (May 15,

2020)

-

U.S. & Canada softwood and panel markets - week 17, 2020 (May 8,

2020)

-

U.S. & Canada softwood and panel markets - week 16, 2020 (May 1,

2020)

-

U.S. & Canada softwood and panel markets - week 15, 2020 (Apr

23,

2020)

-

U.S. & Canada softwood and panel markets - week 14, 2020 (Apr

17, 2020)

-

U.S. & Canada softwood and panel markets - week 13, 2020 (Apr

08, 2020)

-

U.S. & Canada softwood and panel markets - week 12, 2020 (Mar

31, 2020)

-

U.S. & Canada softwood and panel markets - week 11, 2020 (Mar

24,

2020)

-

U.S. & Canada softwood and panel markets - week 5, 2020 (Feb

11,

2020)

-

U.S. & Canada softwood and panel markets - week 4, 2020 (Feb

4, 2020)

-

U.S. & Canada softwood and panel markets - week 3, 2020 (January

27,

2020)

-

U.S. & Canada softwood and panel markets - week 2, 2020 (January

20,

2020)

-

U.S. & Canada softwood and panel markets - week 1, 2020 (January

13,

2020)

-

U.S. & Canada softwood and panel markets - week 50, 2019 (December

17,

2019)

-

U.S. & Canada softwood and panel markets - week 49, 2019 (December

10,

2019)

-

U.S. & Canada softwood and panel markets - week 48, 2019 (December

3, 2019)

-

U.S. & Canada softwood and panel markets - week 47, 2019 (November

26, 2019)

-

U.S. & Canada softwood and panel markets - week 46, 2019 (November

19, 2019)

-

U.S. & Canada softwood and panel markets - week 45, 2019 (November

12, 2019)

-

U.S. & Canada softwood and panel markets - week 44, 2019 (November

5, 2019)

-

U.S. & Canada softwood and panel markets - week 43, 2019 ( October

29, 2019)

-

U.S. & Canada softwood and panel markets - week 42, 2019 ( October

22, 2019)

-

U.S. & Canada softwood and panel markets - week 41, 2019 ( October

15, 2019)

-

U.S. & Canada softwood and panel markets - week 40, 2019 ( October

8, 2019)

-

U.S. & Canada softwood and panel markets - week 39, 2019 ( October

1, 2019)

-

U.S. & Canada softwood and panel markets - week 38, 2019 ( September 24,

2019)

-

U.S. softwood and panel markets - week 37, 2019 ( September 17,

2019)

-

U.S. softwood and panel markets - week 36, 2019 ( September 10,

2019)

-

U.S. softwood and panel markets - week 35, 2019 ( September 3,

2019)

-

U.S. softwood and panel markets - week 34, 2019 ( August 23,

2019)

-

U.S. softwood and panel markets - week 33, 2019 ( August 16,

2019)

-

U.S. softwood and panel markets - week 32, 2019 ( August 09,

2019)

-

U.S. softwood and panel markets - week 31, 2019 ( August 02,

2019)

-

U.S. softwood and panel markets - week 30, 2019 ( July

26, 2019)

-

U.S. softwood and panel markets - week 29, 2019 ( July 19,

2019)

-

U.S. softwood and panel markets - week 28, 2019 ( July 12,

2019)

-

U.S. softwood and panel markets - week 27, 2019 ( July 03,

2019)

-

U.S. softwood and panel markets - week 26, 2019 ( June 28,

2019)

-

U.S. softwood and panel markets - week 25, 2019 ( June 21,

2019)

-

U.S. softwood and panel markets - week 24, 2019 ( June 14,

2019)

-

U.S. softwood and panel markets - week 23, 2019 ( June 07,

2019)

-

U.S. softwood and panel markets - week 22, 2019 ( May 31,

2019)

-

U.S. softwood and panel markets - week 21, 2019 ( May 24,

2019)

-

U.S. softwood and panel markets - week 20, 2019 ( May 17,

2019)

-

U.S. softwood and panel markets - week 19, 2019 ( May 10,

2019)

-

U.S. softwood and panel markets - week 18, 2019 ( May 03,

2019)

-

U.S. softwood and panel markets - week 17, 2019 ( April 26,

2019)

-

U.S. softwood and panel markets - week 16, 2019 ( April 19,

2019)

-

U.S. softwood and panel markets - week 15, 2019 ( April 12,

2019)

-

U.S. softwood and panel markets - week 14, 2019 ( April 05,

2019)

-

U.S. softwood and panel markets - week 13, 2019 ( March

29, 2019)

-

U.S. softwood and panel markets - week 12, 2019 ( March

22, 2019)

-

U.S. softwood and panel markets - week 11, 2019 ( March

15, 2019)

-

U.S. softwood and panel markets - week 10, 2019 ( March

08, 2019)

-

U.S. softwood and panel markets - week 9, 2019 ( March

01, 2019)

-

U.S. softwood and panel markets - week 8, 2019 ( February.

22, 2019)

-

U.S. softwood and panel markets - week 7, 2019 ( February.

15, 2019)

-

U.S. softwood and panel markets - week 6, 2019 ( February.

08, 2019)

-

U.S. softwood and panel markets - week 5, 2019 ( February.

01, 2019)

-

U.S. softwood and panel markets - week 4, 2019 (January. 25,

2019)

-

U.S. softwood and panel markets - week 3, 2019 (January. 18,

2019)

-

U.S. softwood and panel markets - week 2, 2019 (January. 11,

2019)

-

U.S. softwood and panel markets - week 1, 2019 (January. 04,

2019)

|

|

|