|

Lumber and panel market weekly report ----

Week

32, 2022 |

|

By Madison's Lumber Reporter

During these months of deep summer when

construction activity is still going on but

lumber sales slow because most retailers and

end-user have received the wood they expect to

need before Q3, the lumber market generally

finds new balance. There are, of course, other

variables which affect solid wood prices during

the summer season; such as wildfires, labour

disputes, disruptions to transportation, etc.

This year it looks like there is a nice

equilibrium, as the general price trend over the

past couple of months has been quite stable.

Industry folks are relieved to see some

stability returning, after the intense

fluctuation of prices over the past two years.

The U.S. housing market is cooling off slightly

but is still much more active than 2019 and

earlier, so there is potential for more good

lumber sales volumes coming in the near future.

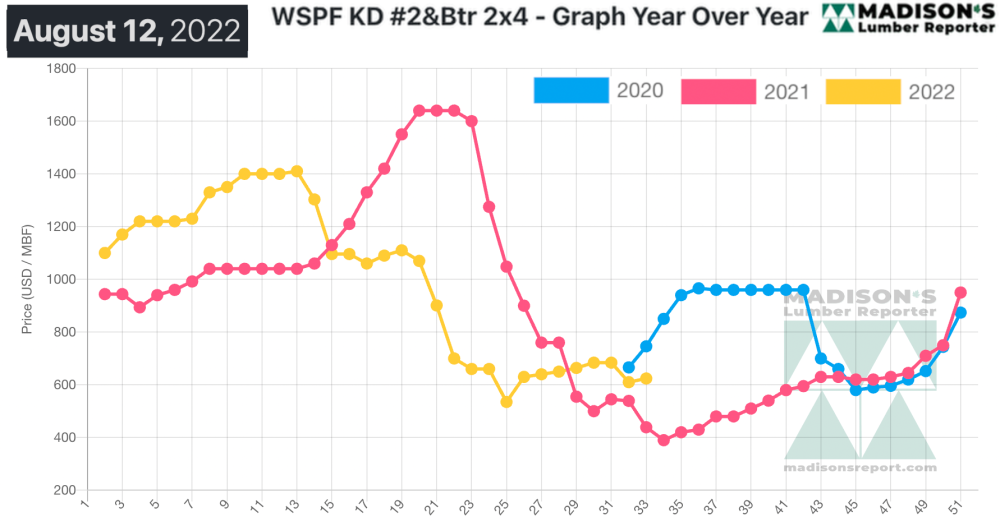

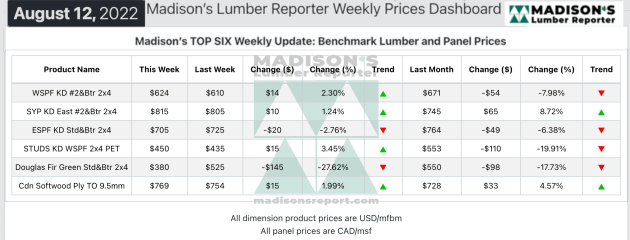

Recovering somewhat from a steep drop the week

before, for the week ending August 12, the price

of benchmark softwood lumber item Western

Spruce-Pine-Fir 2×4 #2&Btr KD (RL) was US$624

mfbm. This is up by $14, or two per cent from

the previous week when it was $610, and is down

by $47, or seven per cent, from one month ago

when it was $671.

Sawmills fiddled with their asking prices as

they established order files into late-August or

early-September, item- and source-dependent.

“A combination of curtailment announcement by a

major producer and the re-designation of lumber

Futures boosted market activity.” — Madison’s

Lumber Reporter

The re-designation of lumber futures to include

Eastern S-P-F products early in the week clouded

an already confused market, pushing many

heretofore reluctant buyers off the fence and

into purchasing-mode. Low grade offerings were

nearly as limited as standard grades.

Western S-P-F suppliers in Canada reported

strong inquiry and follow-through compared to

the previous week. First, a big change to lumber

futures specifications on the CME came about,

making trading more liquid. While volumes remain

tiny compared to other commodities, the prices

quoted immediately jumped up from the previous

week to match cash exactly. The product mix in

futures now includes Eastern S-P-F, so prices

quoted should not be compared just to WSPF as

previously. Adding to that, West Fraser

announced the permanent curtailment of roughly

170 million board feet of combined production at

its Fraser Lake and Williams Lake sawmills in

BC. Order files at sawmills ranged between two-

and four-weeks.

“Demand for bread-and-butter dimensional

Southern Yellow Pine items slumped a bit,

particularly that for 2×6 in the central zone.

Order files on standard grade commodities were

in the one- to three-week range while high grade

pushed into the first week of September. Stud

sales remained robust compared to dimension,

with lead times into the week of August 29th and

stretching into September. ” — Madison’s Lumber

Reporter

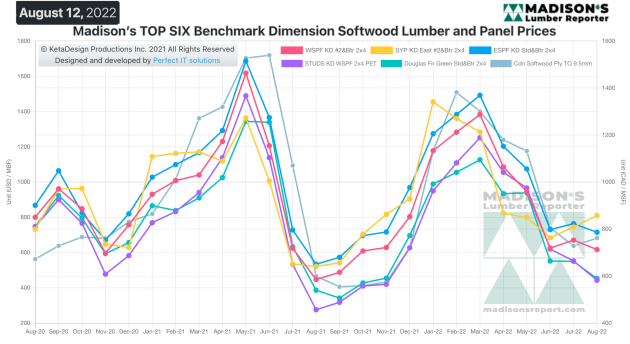

Madison’s Benchmark Top-Six Softwood Lumber and Panel

Prices: Monthly Averages

Compared to the same week last year, when it was $439 mfbm, the price of

Western Spruce-Pine-Fir 2×4 #2&Btr KD (RL) for the week ending August

12, was up by $185, or 42 per cent. Compared to two years ago when it

was $746, that week’s price is down by -$122, or 16 per cent.

.

-

U.S. & Canada softwood and panel markets - week

31 2022 (Aug

16,

2022)

-

U.S. & Canada softwood and panel markets - week

30 2022 (Aug

09,

2022)

-

U.S. & Canada softwood and panel markets - week

29 2022 (Aug

02,

2022)

-

U.S. & Canada softwood and panel markets - week

28 2022 (Jul

26,

2022)

-

U.S. & Canada softwood and panel markets - week

27 2022 (Jul

19,

2022)

-

U.S. & Canada softwood and panel markets - week

26 2022 (Jul

12,

2022)

-

U.S. & Canada softwood and panel markets - week

25 2022 (Jul

05,

2022)

-

U.S. & Canada softwood and panel markets - week

24 2022 (Jun

29,

2022)

-

U.S. & Canada softwood and panel markets - week

23 2022 (Jun

22,

2022)

-

U.S. & Canada softwood and panel markets - week

22 2022 (Jun

15,

2022)

-

U.S. & Canada softwood and panel markets - week

21 2022 (Jun

08,

2022)

-

U.S. & Canada softwood and panel markets - week

20 2022 (Jun

01,

2022)

-

U.S. & Canada softwood and panel markets - week

19 2022 (May

25,

2022)

-

U.S. & Canada softwood and panel markets - week

18 2022 (May

18,

2022)

-

U.S. & Canada softwood and panel markets - week

17 2022 (May

11,

2022)

-

U.S. & Canada softwood and panel markets - week

16 2022 (May

04,

2022)

-

U.S. & Canada softwood and panel markets - week

15 2022 (Apr

26,

2022)

-

U.S. & Canada softwood and panel markets - week

14 2022 (Apr

19,

2022)

-

U.S. & Canada softwood and panel markets - week

13 2022 (Apr

12,

2022)

-

U.S. & Canada softwood and panel markets - week

12 2022 (Apr

05,

2022)

-

U.S. & Canada softwood and panel markets - week

11 2022 (Mar

29,

2022)

-

U.S. & Canada softwood and panel markets - week

10 2022 (Mar

22,

2022)

-

U.S. & Canada softwood and panel markets - week

9 2022 (Mar

15,

2022)

-

U.S. & Canada softwood and panel markets - week

8 2022 (Mar

08,

2022)

-

U.S. & Canada softwood and panel markets - week

7 2022 (Mar

01,

2022)

-

U.S. & Canada softwood and panel markets - week

6 2022 (Feb

22,

2022)

-

U.S. & Canada softwood and panel markets - week

5 2022 (Feb

15,

2022)

-

U.S. & Canada softwood and panel markets - week

4 2022 (Feb

08,

2022)

-

U.S. & Canada softwood and panel markets - week

3 2022 (Feb

01,

2022)

-

U.S. & Canada softwood and panel markets - week

2 2022 (Jan

25,

2022)

-

U.S. & Canada softwood and panel markets - week

1 2022 (Jan

18,

2022)

-

U.S. & Canada softwood and panel markets - week

47 2021 (Dec

22,

2021)

-

U.S. & Canada softwood and panel markets - week

46 2021 (Dec

15,

2021)

-

U.S. & Canada softwood and panel markets - week

45 2021 (Dec

08,

2021)

-

U.S. & Canada softwood and panel markets - week

44 2021 (Dec

01,

2021)

-

U.S. & Canada softwood and panel markets - week

43 2021 (Nov24,

2021)

-

U.S. & Canada softwood and panel markets - week

42 2021 (Nov17,

2021)

-

U.S. & Canada softwood and panel markets - week

41 2021 (Nov10,

2021)

-

U.S. & Canada softwood and panel markets - week

40 2021 (Nov

03,

2021)

-

U.S. & Canada softwood and panel markets - week

39 2021 (Oct

27,

2021)

-

U.S. & Canada softwood and panel markets - week

38 2021 (Oct

20,

2021)

-

U.S. & Canada softwood and panel markets - week

37 2021 (Oct

13,

2021)

-

U.S. & Canada softwood and panel markets - week

36 2021 (Oct

06,

2021)

-

U.S. & Canada softwood and panel markets - week

35 2021 (Sep

29,

2021)

-

U.S. & Canada softwood and panel markets - week

34 2021 (Sep

22,

2021)

-

U.S. & Canada softwood and panel markets - week

33 2021 (Sep

8,

2021)

-

U.S. & Canada softwood and panel markets - week

32 2021 (Sep

1,

2021)

-

U.S. & Canada softwood and panel markets - week

31 2021 (Aug

25,

2021)

-

U.S. & Canada softwood and panel markets - week

30 2021 (Aug

18,

2021)

-

U.S. & Canada softwood and panel markets - week

29 2021 (Aug

11,

2021)

-

U.S. & Canada softwood and panel markets - week

28 2021 (Aug

04,

2021)

-

U.S. & Canada softwood and panel markets - week

27 2021 (Jul

28,

2021)

-

U.S. & Canada softwood and panel markets - week

26 2021 (Jul

21,

2021)

-

U.S. & Canada softwood and panel markets - week

25 2021 (Jul

14,

2021)

-

U.S. & Canada softwood and panel markets - week

24 2021 (Jul

07,

2021)

-

U.S. & Canada softwood and panel markets - week

23 2021 (Jun

30,

2021)

-

U.S. & Canada softwood and panel markets - week

22 2021 (Jun

23,

2021)

-

U.S. & Canada softwood and panel markets - week

21 2021 (Jun

10,

2021)

-

U.S. & Canada softwood and panel markets - week

20 2021 (Jun

03,

2021)

-

U.S. & Canada softwood and panel markets - week

19 2021 (May

26,

2021)

-

U.S. & Canada softwood and panel markets - week

18 2021 (May

19,

2021)

-

U.S. & Canada softwood and panel markets - week

17 2021 (May

12,

2021)

-

U.S. & Canada softwood and panel markets - week

16 2021 (May

5,

2021)

-

U.S. & Canada softwood and panel markets - week

15 2021 (Apr

28,

2021)

-

U.S. & Canada softwood and panel markets - week

14 2021 (Apr

21,

2021)

-

U.S. & Canada softwood and panel markets - week

13 2021 (Apr

15,

2021)

-

U.S. & Canada softwood and panel markets - week

12 2021 (Apr

8,

2021)

-

U.S. & Canada softwood and panel markets - week

11 2021 (Apr

1,

2021)

-

U.S. & Canada softwood and panel markets - week

10 2021 (Mar

25,

2021)

-

U.S. & Canada softwood and panel markets - week

09 2021 (Mar

17,

2021)

-

U.S. & Canada softwood and panel markets - week

08 2021 (Mar

10,

2021)

-

U.S. & Canada softwood and panel markets - week

07 2021 (Mar

03,

2021)

-

U.S. & Canada softwood and panel markets - week

06 2021 (Feb

24,

2021)

-

U.S. & Canada softwood and panel markets - week

05 2021 (Feb

16,

2021)

-

U.S. & Canada softwood and panel markets - week

04 2021 (Feb

04,

2021)

-

U.S. & Canada softwood and panel markets - week

03 2021 (Jan

29,

2021)

-

U.S.&nb303& Canada softwood and panel markets - week

02 2021 (Jan

22,

2021)

-

U.S. & Canada softwood and panel markets - week

01 2021 (Jan

15,

2021)

-

U.S. & Canada softwood and panel markets - week

49 2020 (Dec

16,

2020)

-

U.S. & Canada softwood and panel markets - week

48 2020 (Dec

09,

2020)

-

U.S. & Canada softwood and panel markets - week

47 2020 (Dec

02,

2020)

-

U.S. & Canada softwood and panel markets - week

46 2020 (Nov

25,

2020)

-

U.S. & Canada softwood and panel markets - week

45 2020 (Nov

18,

2020)

-

U.S. & Canada softwood and panel markets - week

44 2020 (Nov

11,

2020)

-

U.S. & Canada softwood and panel markets - week

43 2020 (Nov

4,

2020)

-

U.S. & Canada softwood and panel markets - week

42 2020 (Oct

28,

2020)

-

U.S. & Canada softwood and panel markets - week

41 2020 (Oct

21,

2020)

-

U.S. & Canada softwood and panel markets - week

40 2020 (Oct

14,

2020)

-

U.S. & Canada softwood and panel markets - week

39, 2020 (Oct

07,

2020)

-

U.S. & Canada softwood and panel markets - week

38, 2020 (Sep

30,

2020)

-

U.S. & Canada softwood and panel markets - week

37, 2020 (Sep

23,

2020)

-

U.S. & Canada softwood and panel markets - week

36, 2020 (Sep

16,

2020)

-

U.S. & Canada softwood and panel markets - week

35, 2020 (Sep

09,

2020)

-

U.S. & Canada softwood and panel markets - week

34, 2020 (Sep

02,

2020)

-

U.S. & Canada softwood and panel markets - week

33, 2020 (Aug

26,

2020)

-

U.S. & Canada softwood and panel markets - week

32, 2020 (Aug

19,

2020)

-

U.S. & Canada softwood and panel markets - week

31, 2020 (Aug

12,

2020)

-

U.S. & Canada softwood and panel markets - week

30, 2020 (Aug

05,

2020)

-

U.S. & Canada softwood and panel markets - week 29, 2020 (Jul

29,

2020)

-

U.S. & Canada softwood and panel markets - week 28, 2020 (Jul

22,

2020)

-

U.S. & Canada softwood and panel markets - week 27, 2020 (Jul

17,

2020)

-

U.S. & Canada softwood and panel markets - week 26, 2020 (Jul

10,

2020)

-

U.S. & Canada softwood and panel markets - week 25, 2020 (Jul

02,

2020)

-

U.S. & Canada softwood and panel markets - week 24, 2020 (Jun

25,

2020)

-

U.S. & Canada softwood and panel markets - week 23, 2020 (Jun

17,

2020)

-

U.S. &

Canada softwood and panel markets - week 22, 2020 (Jun

10,

2020)

-

U.S. &

Canada softwood and panel markets - week 21, 2020 (Jun

3,

2020)

-

U.S. &

Canada softwood and panel markets - week 20, 2020 (May 27,

2020)

-

U.S. &

Canada softwood and panel markets - week 19, 2020 (May 21,

2020)

-

U.S. &

Canada softwood and panel markets - week 18, 2020 (May 15,

2020)

-

U.S. &

Canada softwood and panel markets - week 17, 2020 (May 8,

2020)

-

U.S. &

Canada softwood and panel markets - week 16, 2020 (May 1,

2020)

-

U.S. &

Canada softwood and panel markets - week 15, 2020 (Apr

23,

2020)

-

U.S. &

Canada softwood and panel markets - week 14, 2020 (Apr

17,

2020)

-

U.S. &

Canada softwood and panel markets - week 13, 2020 (Apr

08,

2020)

-

U.S. &

Canada softwood and panel markets - week 12, 2020 (Mar

31,

2020)

-

U.S. &

Canada softwood and panel markets - week 11, 2020 (Mar

24,

2020)

-

U.S. &

Canada softwood and panel markets - week 5, 2020 (Feb

11,

2020)

-

U.S. &

Canada softwood and panel markets - week 4, 2020 (Feb

4,

2020)

-

U.S. &

Canada softwood and panel markets - week 3, 2020 (January

27,

2020)

-

U.S. &

Canada softwood and panel markets - week 2, 2020 (January

20,

2020)

-

U.S. &

Canada softwood and panel markets - week 1, 2020 (January

13,

2020)

-

U.S. &

Canada softwood and panel markets - week 50, 2019 (December

17,

2019)

-

U.S. &

Canada softwood and panel markets - week 49, 2019 (December

10,

2019)

-

U.S. &

Canada softwood and panel markets - week 48, 2019 (December

3,

2019)

-

U.S. &

Canada softwood and panel markets - week 47, 2019 (November

26,

2019)

-

U.S. &

Canada softwood and panel markets - week 46, 2019 (November

19,

2019)

-

U.S. &

Canada softwood and panel markets - week 45, 2019 (November

12,

2019)

-

U.S. &

Canada softwood and panel markets - week 44, 2019 (November

5,

2019)

-

U.S. &

Canada softwood and panel markets - week 43, 2019 ( October

29,

2019)

-

U.S. &

Canada softwood and panel markets - week 42, 2019 ( October

22,

2019)

-

U.S. &

Canada softwood and panel markets - week 41, 2019 ( October

15,

2019)

-

U.S. &

Canada softwood and panel markets - week 40, 2019 ( October

8,

2019)

-

U.S. &

Canada softwood and panel markets - week 39, 2019 ( October

1,

2019)

-

U.S. &

Canada softwood and panel markets - week 38, 2019 ( September 24,

2019)

-

U.S. softwood and panel markets - week 37, 2019 ( September 17,

2019)

-

U.S. softwood and panel markets - week 36, 2019 ( September 10,

2019)

-

U.S. softwood and panel markets - week 35, 2019 ( September 3,

2019)

-

U.S. softwood and panel markets - week 34, 2019 ( August 23,

2019)

-

U.S. softwood and panel markets - week 33, 2019 ( August 16,

2019)

-

U.S. softwood and panel markets - week 32, 2019 ( August 09,

2019)

-

U.S. softwood and panel markets - week 31, 2019 ( August 02,

2019)

-

U.S. softwood and panel markets - week 30, 2019 ( July

26, 2019)

-

U.S. softwood and panel markets - week 29, 2019 ( July 19,

2019)

-

U.S. softwood and panel markets - week 28, 2019 ( July 12,

2019)

-

U.S. softwood and panel markets - week 27, 2019 ( July 03,

2019)

-

U.S. softwood and panel markets - week 26, 2019 ( June 28,

2019)

-

U.S. softwood and panel markets - week 25, 2019 ( June 21,

2019)

-

U.S. softwood and panel markets - week 24, 2019 ( June 14,

2019)

-

U.S. softwood and panel markets - week 23, 2019 ( June 07,

2019)

-

U.S. softwood and panel markets - week 22, 2019 ( May 31,

2019)

-

U.S. softwood and panel markets - week 21, 2019 ( May 24,

2019)

-

U.S. softwood and panel markets - week 20, 2019 ( May 17,

2019)

-

U.S. softwood and panel markets - week 19, 2019 ( May 10,

2019)

-

U.S. softwood and panel markets - week 18, 2019 ( May 03,

2019)

-

U.S. softwood and panel markets - week 17, 2019 ( April 26,

2019)

-

U.S. softwood and panel markets - week 16, 2019 ( April 19,

2019)

-

U.S. softwood and panel markets - week 15, 2019 ( April 12,

2019)

-

U.S. softwood and panel markets - week 14, 2019 ( April 05,

2019)

-

U.S. softwood and panel markets - week 13, 2019 ( March

29, 2019)

-

U.S. softwood and panel markets - week 12, 2019 ( March

22, 2019)

-

U.S. softwood and panel markets - week 11, 2019 ( March

15, 2019)

-

U.S. softwood and panel markets - week 10, 2019 ( March

08, 2019)

-

U.S. softwood and panel markets - week 9, 2019 ( March

01, 2019)

-

U.S. softwood and panel markets - week 8, 2019 ( February.

22, 2019)

-

U.S. softwood and panel markets - week 7, 2019 ( February.

15, 2019)

-

U.S. softwood and panel markets - week 6, 2019 ( February.

08, 2019)

-

U.S. softwood and panel markets - week 5, 2019 ( February.

01, 2019)

-

U.S. softwood and panel markets - week 4, 2019 (January. 25,

2019)

-

U.S. softwood and panel markets - week 3, 2019 (January. 18,

2019)

-

U.S. softwood and panel markets - week 2, 2019 (January. 11,

2019)

-

U.S. softwood and panel markets - week 1, 2019 (January. 04,

2019)

|

|

|