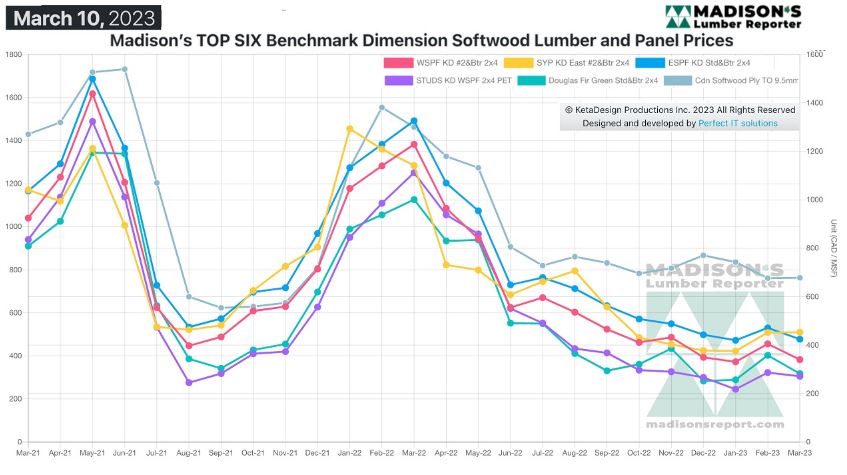

With cold winter weather still a serious issue across the continent,

secondary suppliers of construction framing dimension softwood lumber

competed fiercely for whatever small sales volumes they could muster. As for

producers, sawmills held their ground on pricing only to be met with

resistance from customers. As such, prices did drop – precipitously back to

lows seen in the depths of January.

Lumber manufacturers and resellers alike could only wait for better weather

to come on, bringing with it a return to the hammers-and-nailing of renewed

construction activity for this year. The good news is that there has been no

impediment to timber harvesting, thus log supplies at sawmills across Canada

and the U.S. are good; in expectation of increasing demand once the weather

actually does improve.

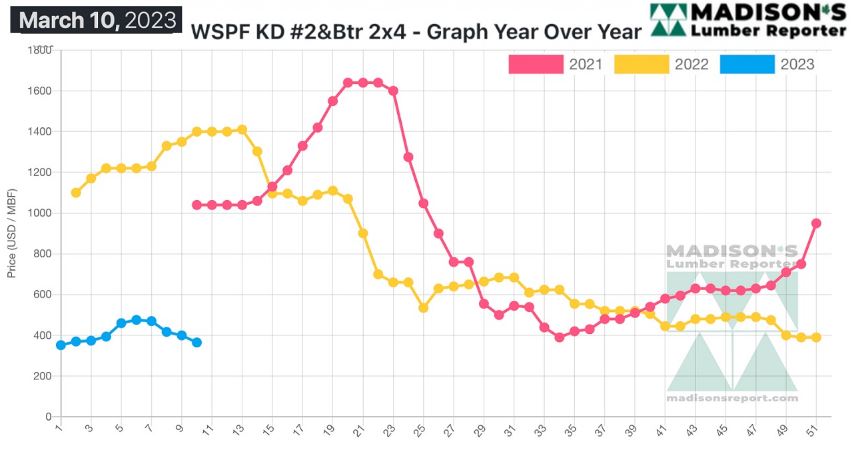

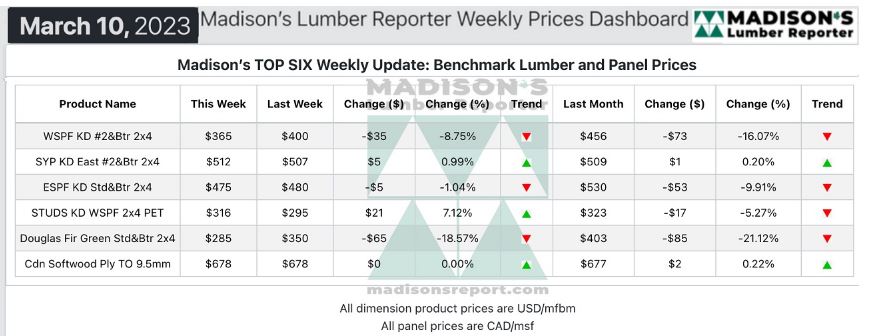

In the week ending March 10, the price of Western Spruce-Pine-Fir 2×4 #2&Btr

KD (RL) was US$365 mfbm, which is down by $35, or nine per cent, from the

previous week when it was $400. That week’s price is down by $91, or 20 per

cent, from one month ago when it was $456.

Demand for North American lumber meandered aimlessly as ongoing winter

weather stalled spring buying once again.

“

Ongoing winter weather in many key markets kept demand to a minimum,

while commodity prices were messy and indeterminate.” — Madison’s Lumber

Reporter

Producers of Western S-P-F lumber and studs in the United States described

mid-March as a sloppy week for inquiry and sales. Asking prices were

adjusted on several bread-and-butter items. Secondary suppliers engaged in a

race to the bottom as they fiercely competed for limited business. Buyers

remained circumspect in their dealings, typically sticking to secondary

suppliers where they could haggle more freely on price point. Sawmill order

files were between two- and three-weeks out, with a few items showing up for

prompt delivery from some sources.

Western S-P-F lumber sales in Canada meandered aimlessly as buyers sat

firmly on the sidelines. Business continued to be confined to small-volume,

just-in-time purchases. The distribution network took care of most of that

volume, furnishing customers with highly-mixed truckloads of specific

tallies. Transportation has been a slower affair of late, with players

worrying that transit times will worsen significantly when spring buying

takes off.

“

Demand for Western S-P-F studs was hit-and-miss, though producers noted

that sales were stronger than for dimension. Buyers maintained their

cautious approach, feeling little pressure to cover more than immediate

needs. When they did step in to make purchases, the distribution network had

sufficient availability at more flexible price points, and with faster

arrival times, than did producers. Sawmills hoped prices had reached a

bottom, as winter weather persisted in many important consuming regions.” —

Madison’s Lumber Reporter

Compared to the same week last year, when it was US$1,400 mfbm, the price of

Western Spruce-Pine-Fir 2×4 #2&Btr KD (RL) for the week ending March 10, was

down by $1,035, or 74 per cent. Compared to two years ago when it was

$1,040, that week’s price is down by $675, or 65 per cent.

More Reports: