By mid-March many regions across the continent faced yet another bout of bad

weather. Meanwhile the densely populated southern U.S. states ramped up

construction activity. Demand for lumber materials remained somewhat muted,

yet suppliers booked enough sales to keep prices generally even from the

previous week.

Sawmills claimed to have extended order files out to two weeks or so, but

resellers suspected this might be an exaggeration. However, the ability of

manufacturers to dismiss counter-offers suggested their order files would

stretch out that far soon enough. Transportation delays continued as harsh

weather remained for another week.

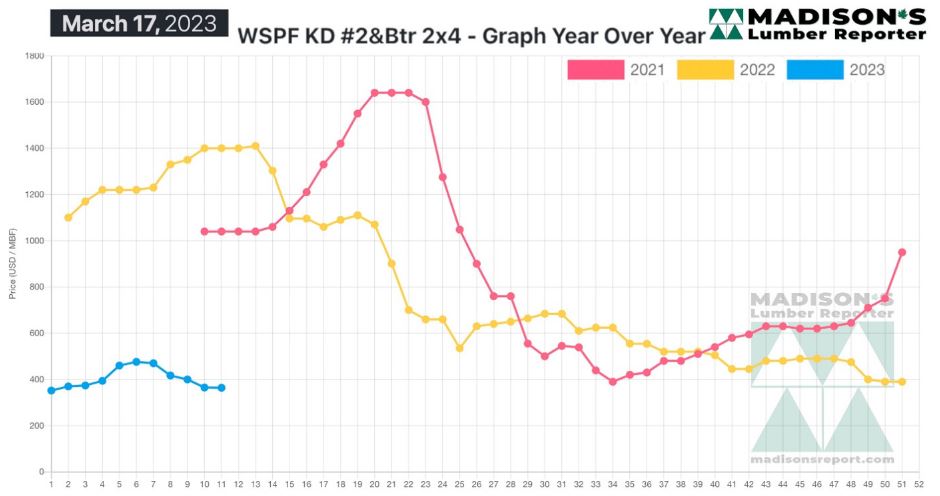

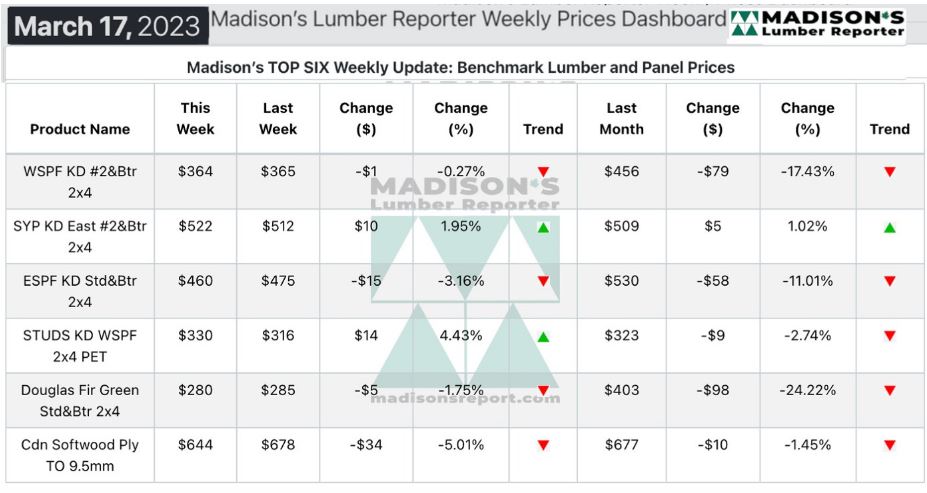

In the week ending March 17, the price of benchmark softwood lumber item

Western Spruce-Pine-Fir 2×4 #2&Btr KD (RL) was US$364 mfbm, which is down by

$1 or zero per cent, from the previous week when it was US$365 mfbm. This is

down by $91, or 20 per cent, from one month ago when it was $456.

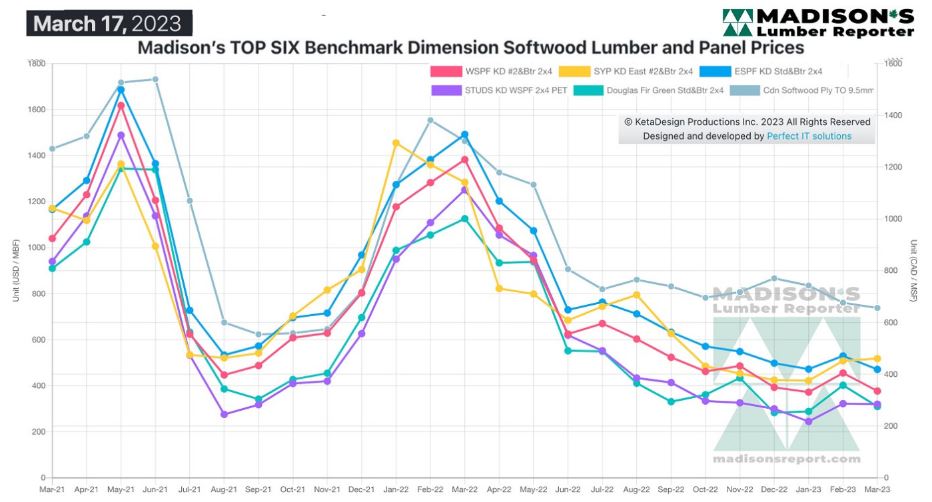

Demand for standard dimension lumber improved a little, while sales of

panels continued to languish by comparison.

“The effects of winter weather still abounded, especially in production

regions where frigid temperatures persistently hampered timber harvesting

and log transportation.” — Madison’s Lumber Reporter

Amid a mushy market, Western S-P-F traders in the U.S. saw better sales

volumes in mid-March. Producers showed a little more confidence as they kept

asking prices at or on either side of the previous week’s levels. Despite

the banking tumult, buyers actively sought near-term coverage to fill holes

in their inventories. Players voiced their concerns that government

intervention in the financial system would negatively affect investment and

growth in the housing sector. Having done enough business to extend order

files into the first week of April, producers were decreasingly interested

in accepting counter-offers.

Western S-P-F lumber prices in Western Canada stabilized as suppliers

reported a more balanced supply-demand equation. Sales of low grade

continued to outperform standard and high grade. Industrial customers stayed

more active than those in the #2&Btr game. While the spring building boost

has yet to materialize, suppliers were more confident in its imminence due

to long-term forecasts showing warmer weather patterns in many key areas.

Demand for Eastern S-P-F panel market was much the same as the previous

week, with the added disincentive of tumbling plywood prices. Buyers smelled

blood and were happy to wait and see how much further this correction might

go. Oriented Strand Board prices were flat amid a tale of two markets; where

demand out of Eastern Canada remained snowed under for the time being while

several key markets south of the border were lumbering to life. Inventory

holders in Ontario and Quebec hoped for warmer weather to melt away the snow

piles eating up their yard space. Suppliers of OSB and plywood in Western

Canada didn’t have much new to report. Wholesalers and distributers in Lower

Mainland British Columbia were able to buy OSB cheaper than print levels for

the first time in several weeks. Prices of plywood meanwhile stumbled around

five points as producers approached their alleged early-April order files

and tried to drum up some interest. Late shipments were commonly reported.”

— Madison’s Lumber Reporter

Compared to the same week last year, when it was US$1,330 mfbm, the price of

Western Spruce-Pine-Fir 2×4 #2&Btr KD (RL) for the week ending March 17,

this price was down by $966, or 73 per cent. Compared to two years ago when

it was $1,040, that week’s price is down by $676, or 65 per cent.

More Reports: