Among Forest Industry Players, All Eyes Were On The Looming Spring Building

Even As Sentiment Continued Very Cautious.

However extremely lean field inventories, an ongoing condition for about two

years, remained. Sawmill kept manufacturing volumes low, waiting for when

demand will actually increase before ramping up production. While prices on

several commodity groups rose, this was more a function of restricted supply

and delayed transportation times than a bump in demand.

Conversations focussed on the future 60- to 90-days time frame as buyers and

sellers alike tried to gauge where this year’s housing construction levels

will be.

There is a perception of return to stability as current price levels match

quite closely with the first two weeks of last year and of 2024. This makes

planning for spring somewhat easier, as the great volatility of recent years

is truly in the past.

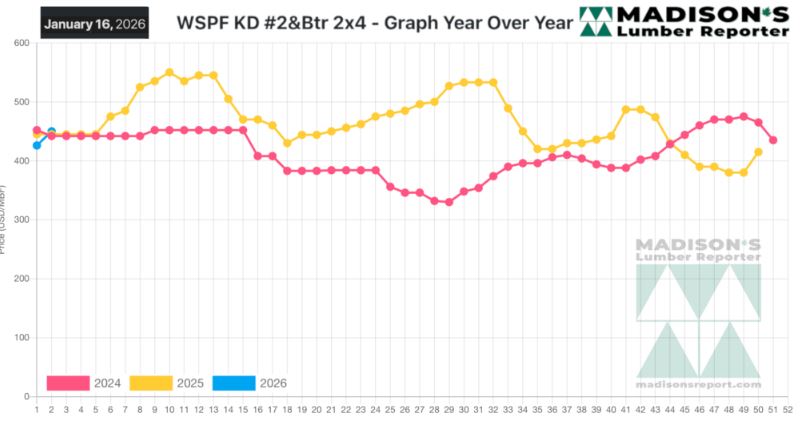

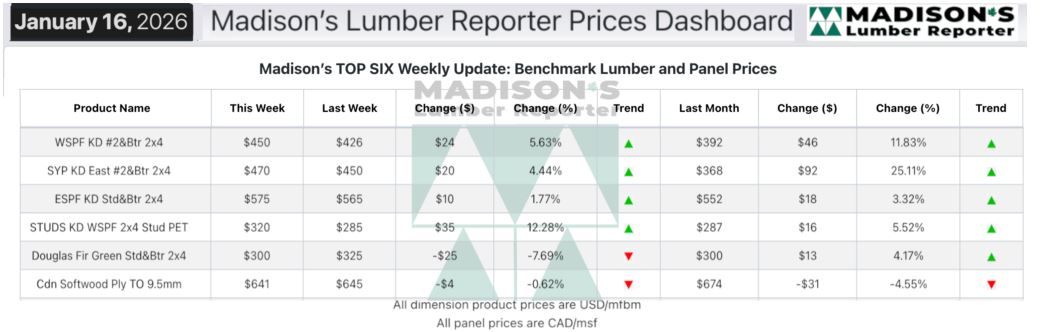

In the week ending January 16, 2026, the price of benchmark softwood lumber

item Western Spruce-Pine-Fir 2×4 #2&Btr KD (RL) was US$450 mfbm. This was up

+$20, or +4%, from the previous week when it was $426, said weekly forest

products industry price guide newsletter Madison’s Lumber Reporter.

That week’s price was up +$58, or +15%, from one month ago when it was $392.

Compared To The Same Week Last Year, When It Was Us$445 Mfbm, The Price Of

Western Spruce-Pine-Fir 2×4 #2&Btr Kd (Rl) For The Week Ending January 16,

2026 Was Up +$5, Or +1%.

Compared To Two Years Ago When It Was $442, That Week’S Price Was Up +$8, Or

+2%.

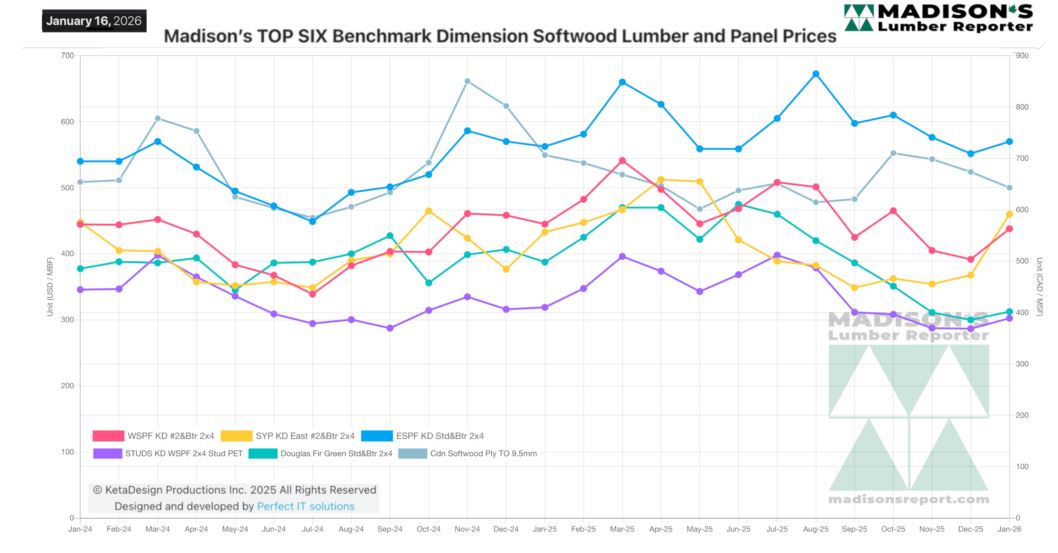

Prices of many lumber and studs items increased somewhat while that of

panels lagged behind.

KEY TAKE-AWAYS:

Limitations on supply continued to drive decent overall business for

Western-SPF sellers in the US.

The market was feeling the squeeze of supplies even as winter weather put a

damper on building activity.

Western-SPF sawmill lists in Canada continued to look thin due to marginally

better-than-expected demand running up against low supply.

Price considerations became secondary to access as disruptions to the supply

chain continued to occur with unsettling frequency.

Eastern-SPF price discovery was much more common on a week-to-week basis due

to a sustained reduction in overall contract business.

Inventories of Southern Yellow Pine remained resoundingly undersupplied.

Eastern stocking wholesalers reported cold weather and apathetic buying kept

a lid on overall business.

Vendors who wanted to get wood on the ground to the ports in New Jersey

prior to spring buying were mindful of cross-country transit in winter.

MADISON’S BENCHMARK TOP-SIX SOFTWOOD LUMBER AND PANEL PRICES: MONTHLY

AVERAGES

Source: madisonsreport.com

More Reports: