Customers Remained Cautious As The Effects Of Ongoing Winter Weather Kept

Construction Activity Low.

Sellers warned of looming supply shortages in the future if everyone held

off buying until they absolutely needed the wood. Sawmills and wholesalers

alike were generally fielding orders highly-specified mixed loads. The

large-volume, bulk purchases which usually signal the spring building season

has arrived had not yet materials. Prices remained firm as suppliers held

their ground, knowing that the flow of orders will start coming in sooner or

later.

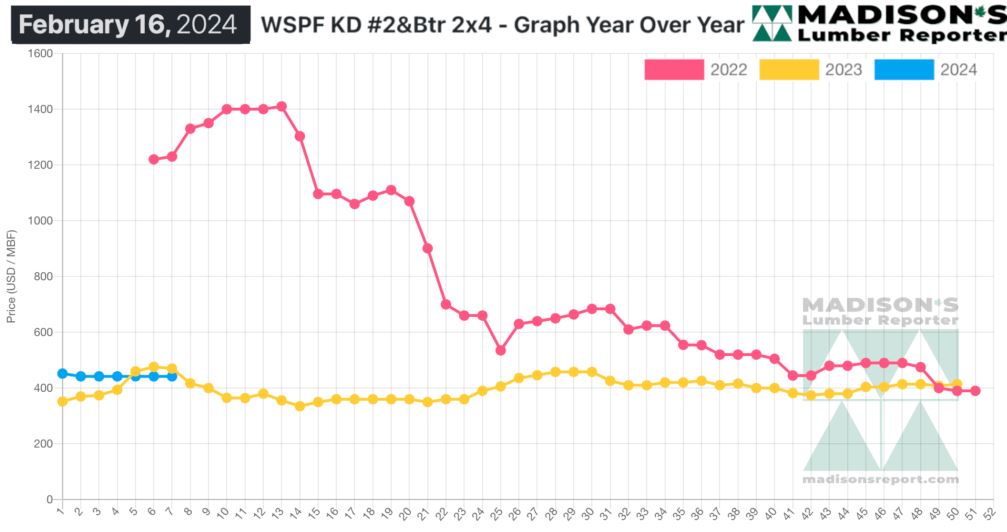

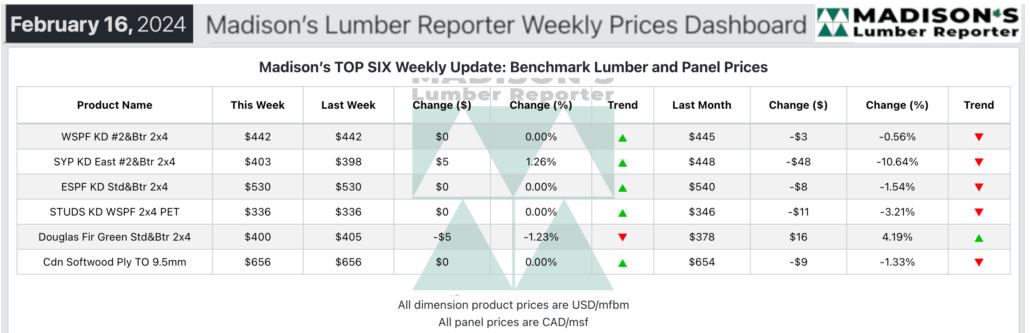

In the week ending February 16, 2024, the price of Western Spruce-Pine-Fir

2×4 #2&Btr KD (RL) was US$442 mfbm, which is flat from the previous week

when it was $442. That week’s price is down by -$3, or -1%, from one month

ago when it was $445.

Uncertainty prevailed in much of the North American lumber market; field

inventories were lean in every lumber product category.

Western S-P-F suppliers in the United States faced ongoing challenges in

matching sputtering demand this. Buyers were indecisive, often switching

between multiple suppliers before making small purchases or leaving the

market altogether. Distributors and wholesalers managed to maintain decent

business levels however, albeit at a slower pace typical for this time of

year.

Pockets of winter weather created disruptions in consumption and

transportation, often in the same region. Purchasers continued to carry

light field inventories as they strongly relied on the distribution network

to have material ready to ship when they needed it.

Uncertainty prevailed in the Canadian Western S-P-F market as buyers largely

remained on the sidelines, effecting subpar demand. While secondary

suppliers reported a steady stream of purchases, actual sales volumes were

low as customers focused on mixed loads and LTL orders. Buyers remained

cautious, opting to hold off despite the widely acknowledged lack of

potential for lower prices.

Larger sawmills held firm on prices, while smaller regional producers in

Western Canada offered discounts on certain items to move accumulated stock.

This discrepancy added to the confusion in spruce and the broader market.

Green Douglas-fir trading mirrored the previous week. Hemlock/fir commodity

prices in general hovered close to the previous week’s levels as supply and

demand remained in a loosely balanced state. With construction activity

uninspiring even in the warmer California markets, trading was slow and

consumption was slower. Buyers continued to purchase conservatively, keeping

inventories low. This raised questions about supply levels once spring

building starts.

MADISON’S BENCHMARK TOP-SIX SOFTWOOD LUMBER AND PANEL PRICES: MONTHLY

AVERAGES

Compared To The Same Week Last Year, When It Was Us$470 Mfbm, The Price

Of Western Spruce-Pine-Fir 2×4 #2&Btr Kd (Rl) For The Week Ending February

16, 2024 Was Down By -$28, Or -6%.

More Reports: