Even As True Spring Weather Has Not Yet Begun This Year, Lumber Sales

Improved To The Point That Prices Surpassed The Levels Of One Year Ago.

Even As True Spring Weather Has Not Yet Begun This Year, Lumber Sales

Improved To The Point That Prices Surpassed The Levels Of One Year Ago.

Since mid-2022 when mortgage lending rates started increasing, both

construction activity and lumber sales dropped somewhat. The trend line for

lumber prices during last year was quite stable, as most industry folks

waited to see how the home building levels would respond to increasing

interest rates. Now in 2024, expectations are that new home construction

will be higher than last year. At this time there is significant lumber

manufacturing capacity still offline, as so many sawmills took curtailment

and downtime in response to soft market conditions.

Once this spring building season gets going, lumber production volumes will

increase back to previously normal levels.

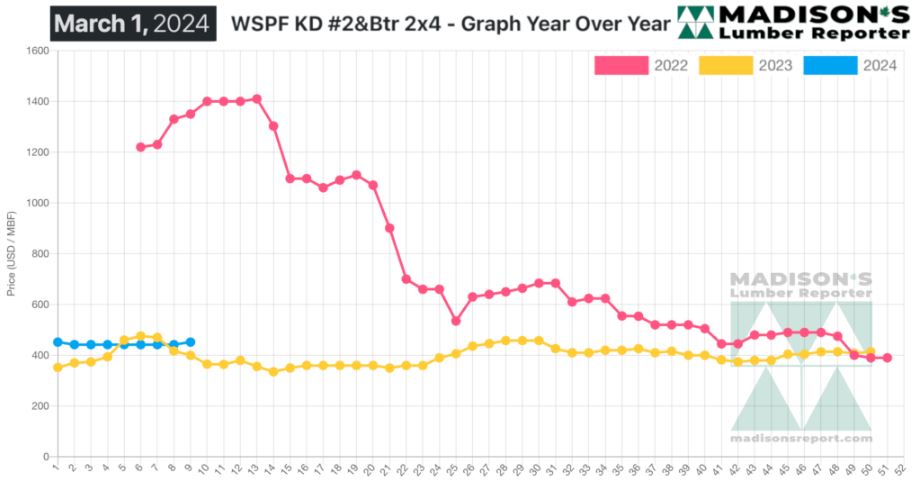

In the week ending March 1, 2024, the price of Western Spruce-Pine-Fir 2×4

#2&Btr KD (RL) was US$452 mfbm, which is up by +$10, or +2%, from the

previous week when it was $442. That week’s price is up by +$8, or +2%, from

one month ago when it was $444.

Lumber and stud prices advanced steadily as demand marched forward.

Panels were a hand-wringing affair for secondary suppliers.

Western S-P-F suppliers in the United States faced ongoing challenges in

matching sputtering demand. Buyers were indecisive, often switching between

multiple suppliers before making small purchases or leaving the market

altogether. Distributors and wholesalers managed to maintain decent business

levels however, albeit at a slower pace than typical for this time of year.

Pockets of winter weather created disruptions in consumption and

transportation, often in the same region. Purchasers continued to carry

light field inventories as they strongly relied on the distribution network

to have material ready to ship when they needed it.

Uncertainty prevailed in the Canadian Western S-P-F market as buyers largely

remained on the sidelines, effecting subpar demand. While secondary

suppliers reported a steady stream of purchases, actual sales volumes were

low as customers focused on mixed loads and LTL orders. Buyers remained

cautious, opting to hold off despite the widely acknowledged lack of

potential for lower prices.

Green Douglas-fir trading mirrored the previous week. Hemlock/fir commodity

prices in general hovered close to the previous week’s levels as supply and

demand remained in a loosely balanced state. With construction activity

uninspiring even in the warmer California markets, trading was slow and

consumption was slower.

Buyers continued to purchase conservatively, keeping inventories low. This

raised questions about supply levels once spring building starts.

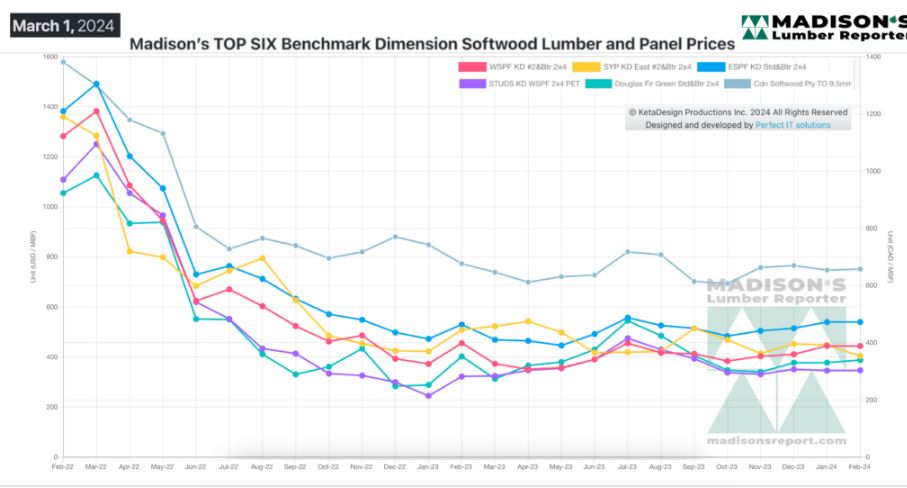

MADISON’S BENCHMARK TOP-SIX SOFTWOOD LUMBER AND PANEL PRICES: MONTHLY

AVERAGES

Compared To The Same Week Last Year, When It Was Us$400 Mfbm, The Price

Of Western Spruce-Pine-Fir 2×4 #2&Btr Kd (Rl) For The Week Ending March 1,

2024 Was Up By +$52, Or +13%.

More Reports: