As January Marched Onward And New Business For 2026 Got Going After The

Annual Holiday Break, Lumber Prices Increased Slightly From The Usual

Seasonal Lows Of Year-End.

Current levels were quite close to the beginning of both last year and 2024,

providing good stability of price trends. This meant industry folks could

better plan for the oncoming spring construction season than has been true

for several years. With the great price volatility of 2020 to 2022 now

firmly in the past, lumber sellers and buyers had their eyes strictly on the

future.

Sawmill production volumes remained lower as operators continue to be

cautious about keeping manufacturing in line with demand. At the same time,

however, inventories throughout the supply chain are so lean as to be

non-existent.

Due to so many unknowns continually cropping up in recent years, lumber

producers will not increase production until there is a true rise in actual

sales.

Customers, meanwhile, have become accustomed to getting the small amounts of

wood they need in relatively short order so have seen no reason to build up

inventory. In this context, no one knows what the market situation will be

over the next few weeks.

The prevailing sentiment is: to just hope there is no shock or surprise

which catches people unprepared.

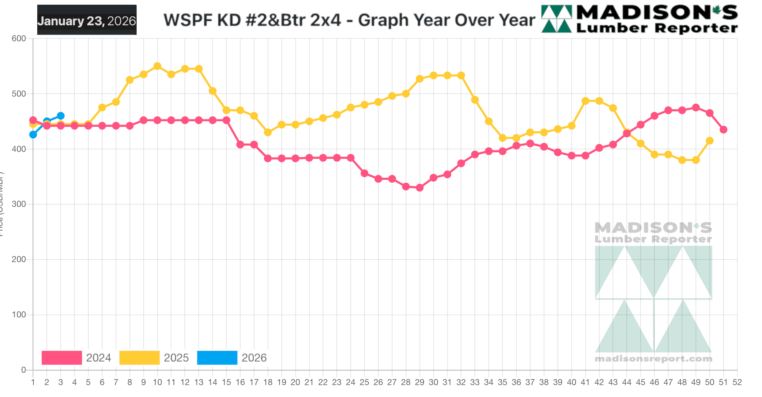

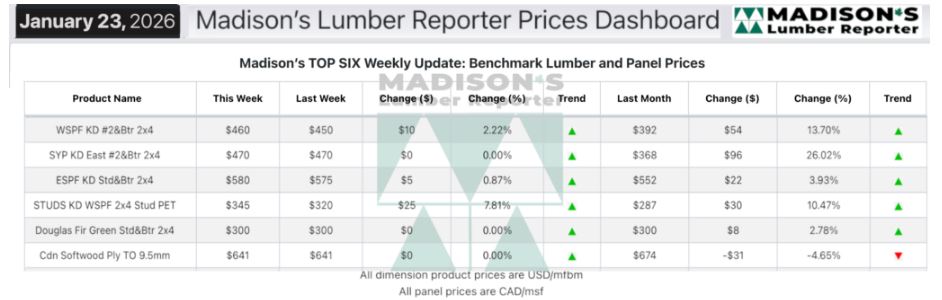

In the week ending January 23, 2026 the price of Western Spruce-Pine-Fir 2×4

#2&Btr KD (RL) was US$460 mfbm, which was up +$10, or +2%, from the previous

week when it was $450, said weekly forest products industry price guide

newsletter Madison’s Lumber Reporter.

That week’s price was up +$68, or +17%, from one month ago when it was $392.

Compared To The Same Week Last Year, When It Was Us$445 Mfbm, The Price Of

Western Spruce-Pine-Fir 2×4 #2&Btr Kd (Rl) For The Week Ending January 23,

2026 Was Up +$15, Or +3%.

Compared To Two Years Ago When It Was $442, That Week’S Price Was Up +$18,

Or +4%.

The supply-driven strengthening trend in SPF and Hem/Fir sales

continued apace as this year’s business got going.

KEY TAKE-AWAYS:

KEY TAKE-AWAYS:

The supply-driven nature of Western-SPF sales persisted for traders in the

United States.

Sawmills managed their production schedules to avoid potential price

corrections.

Prices climbed further on key Western-SPF items in Canada as tight supply

continued to drive upward momentum.

It was another week of strong demand for purveyors of Eastern-SPF

commodities.

Transportation issues abounded as suppliers fielded daily inquiries for

material to be delivered the following week.

Due to severe weather, lumber sellers were unable to ship quicker than

mid-February.

Anemic demand for Southern Yellow Pine retreated even further as buyers

balked at the sharp rise in prices so far this year.

Movement of product continued to be restricted by uneven truck availability,

with the feeling of inconsistent business coming from freight windows

opening and closing rather than fluctuations in demand.

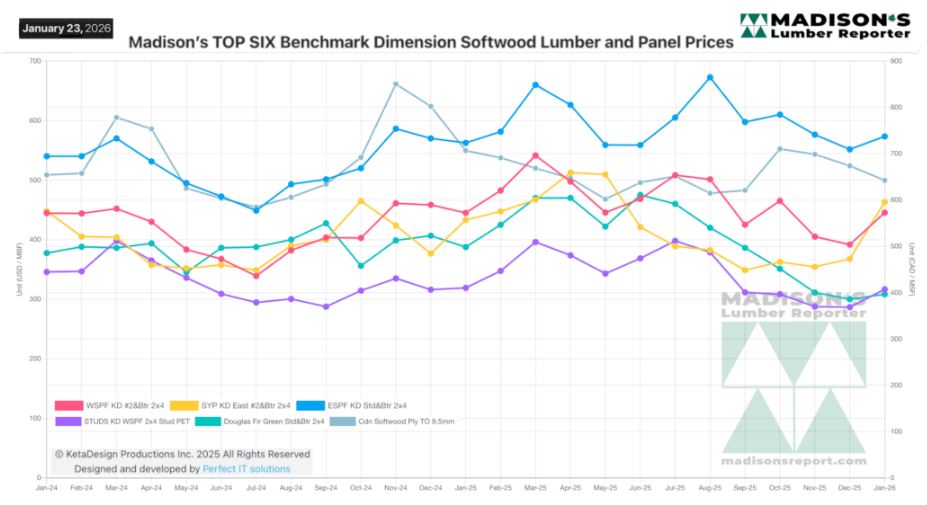

MADISON’S BENCHMARK TOP-SIX SOFTWOOD LUMBER AND PANEL PRICES: MONTHLY

AVERAGES

Source: madisonsreport.com

More Reports: