The North American Construction Framing Dimension Softwood Lumber Market

Maintained A Holding Pattern At The Beginning Of February.

As quite harsh weather continued in many parts of Canada and the US, the

focus was on transportation delays. Customers waited for shipment of solid

wood products already ordered which were slowly moving somewhere along the

supply chain. At these ongoing lower manufacturing volumes, most sawmills

maintained order files out to a couple of weeks.

The goal for producers has been to keep supply in check with continued weak

demand. At the same time, lumber manufacturers put their efforts during

these slower months for construction activity into loading up their yards

with logs.

This is usual for the winter months. As such, lumber producers are ready

with plenty of fibre supply on hand for when demand increases once spring

weather materializes.

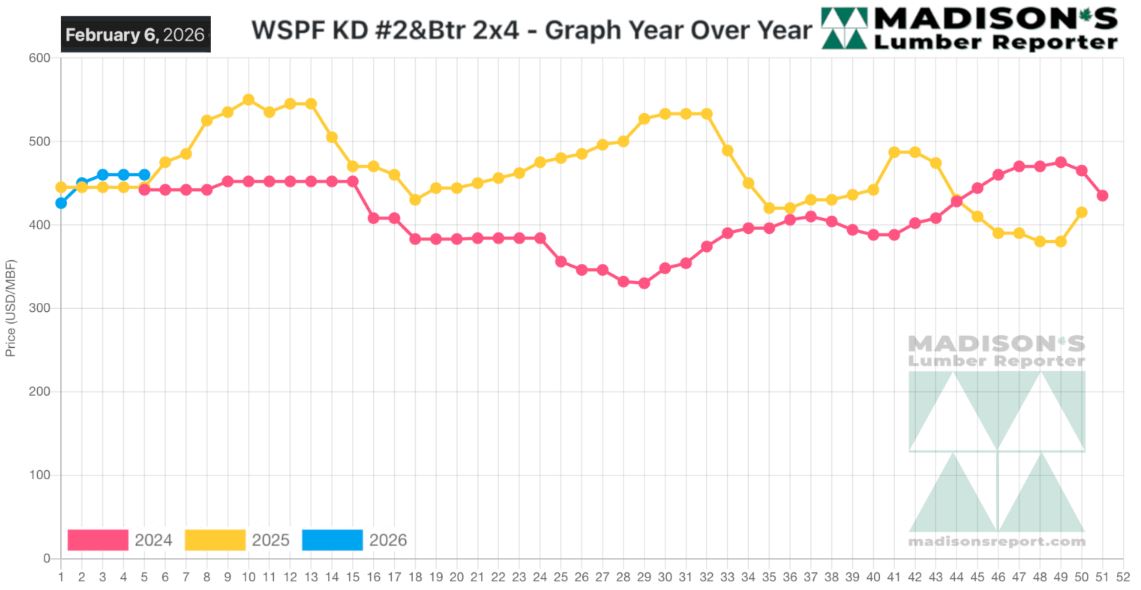

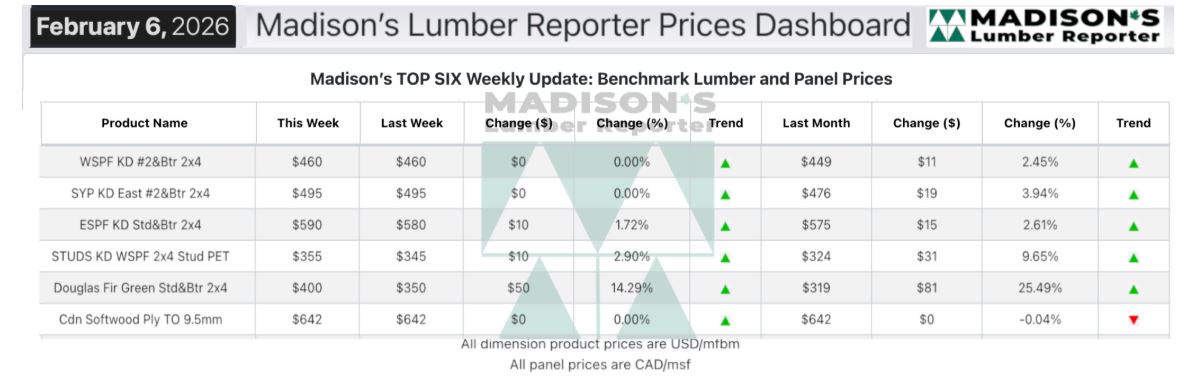

In the week ending February 06, 2026 the price of Western Spruce-Pine-Fir

2×4 #2&Btr KD (RL) was US$460 mfbm, which was flat from the previous week

when it was $460, said weekly forest products industry price guide

newsletter Madison’s Lumber Reporter.

That week’s price was up +$12, or +4%, from one month ago when it was $449.

Compared to the same week last year, when it was US$445 mfbm, the price of

Western Spruce-Pine-Fir 2×4 #2&Btr KD (RL) for the week ending February 06,

2026 was up +$15, or +3%.

Compared to two years ago when it was $442, that week’s price was up +$18,

or +4%.

North American sawmills maintained firm pricing and decent order

files, while buyers digested their current positions and pondered their next

moves.

KEY TAKE-AWAYS:

KEY TAKE-AWAYS:

Western-SPF sellers in the US felt that lower overall lumber supply could be

a difference maker this year.

These sawmills felt no urgency to push prices any further, nor to extend

order files beyond the current two-ish weeks.

Rail service in the West was increasingly unreliable; causing mills to run a

couple of weeks behind on shipments.

In Canada Western-SPF producers held their dimension asking prices firm,

leaning on solid two- to three-week order files.

The logistics pipeline for Eastern-SPF operators was backed up tremendously

in the wake of the recent polar vortex.

In the NorthEast, commodity prices climbed again.

Southern Yellow Pine players described a constrained feel to business where

demand wasn’t fully satisfied in many cases.

Distributers of SYP felt pressure to replenish as persistent inquiry from

buyers in secondary markets whittled their inventories down.

Harsh weather in the US NorthEast caused logistical challenges, as Eastern

Stocking Wholesalers dealt with rail car and truck delays.

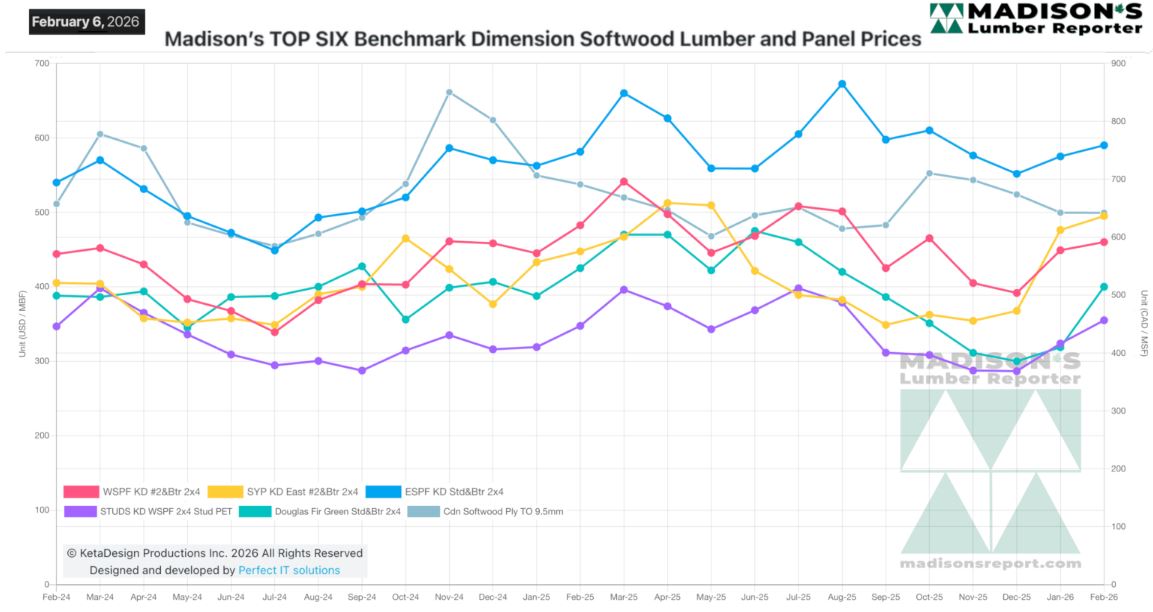

MADISON’S BENCHMARK TOP-SIX SOFTWOOD LUMBER AND PANEL PRICES: MONTHLY

AVERAGES

Source: madisonsreport.com

More Reports: