Yet More Harsh Winter Storms Raged Across North America In Mid-February,

Keeping Demand For Construction Framing Dimension Lumber Soft.

Most operators were focussed on deliveries; as railways and trucking

companies had great difficulty moving solid wood products. Customers eyed

their dwindling inventories with patience as home building activity was

almost non-existent due to below-freezing temperatures and significant

snowfall.

For their part, producers were able to maintain their sawmill order files

out to approximately two weeks, however this in an environment of quite low

demand. Regardless, log yards at mills are stuffed with fibre for whenever

spring does arrive and demand picks up.

Sawmills will be able to ramp up production quite quickly since there is

plenty of feedstock on hand for them.

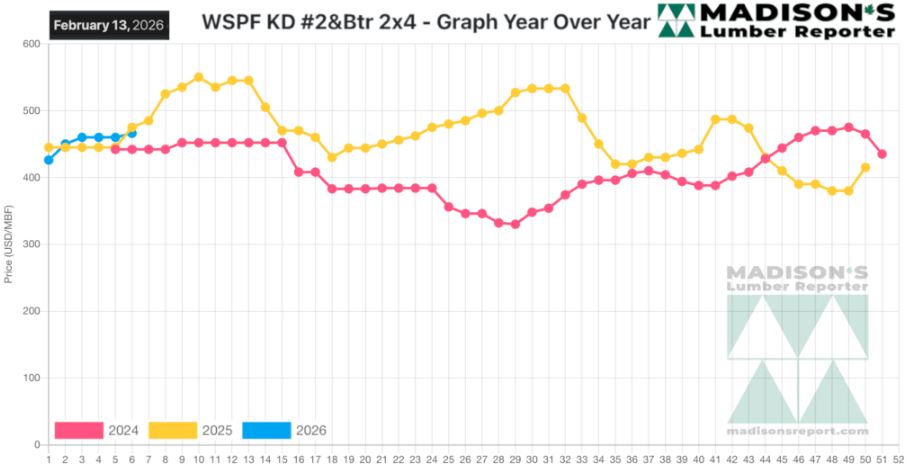

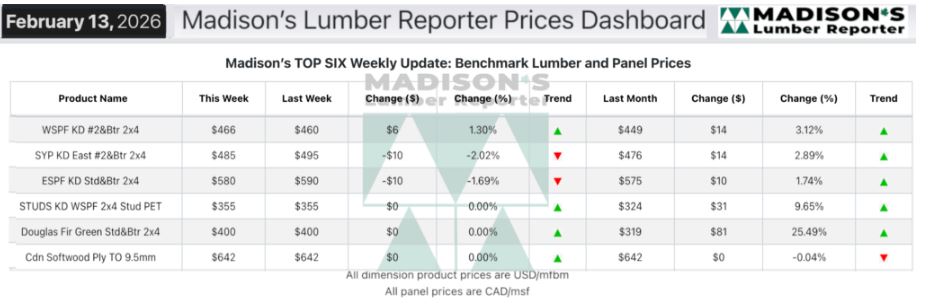

In the week ending February 13, 2026, the price of benchmark softwood lumber

item Western Spruce-Pine-Fir 2? #2&Btr KD (RL) was US$466 mfbm.

This was up +$6, or +1%, from the previous week when it was $460, said

weekly forest products industry price guide newsletter Madison’s Lumber

Reporter.

That week’s price was up +$17, or +4%, from one month ago when it was $449.

Compared To The Same Week Last Year, When It Was Us$475 Mfbm, The Price Of

Western Spruce-Pine-Fir 2? #2&Btr Kd (Rl) For The Week Ending February 13,

2026 Was Down -$9, Or -2%.

Compared To Two Years Ago When It Was $442, That Week’S Price Was Up +$24,

Or +5%.

It was a tale of two markets; as tight truck business was reported in

the West, while activity remained frozen solid in the East.

KEY TAKE-AWAYS:

KEY TAKE-AWAYS:

Due to the disjointed nature of this trading landscape, sellers of

Western-SPF in the US had vastly different appraisals.

Purchasers kept their inventories lean as they continued to feel uncertain

about the direction of the market heading into spring.

Experienced players kept their sights on ground-level factors like lumber

inventory buildups, weather patterns, and major transportation corridors.

After a strong January, buyers of Western-SPF in Canada remained on the

sidelines for an extended period.

There was limited prompt availability, as sawmill order files were largely

into late-February or early-March.

Ongoing severe winter weather in most regions of Eastern-SPF affected

business at all levels.

Retailers hesitated to put more stock on the ground while their yards

remained filled with snow piles, and downstream demand was in hibernation.

Some secondary suppliers sold at below-replacement costs to keep product

flowing.

In Southern Yellow Pine there was demonstrable downside pressure on key

dimension items.

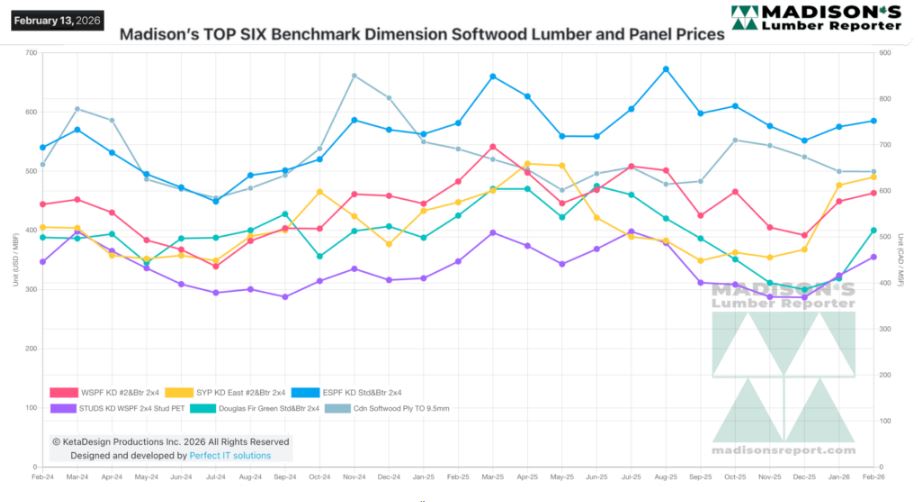

MADISON’S BENCHMARK TOP-SIX SOFTWOOD LUMBER AND PANEL PRICES: MONTHLY

AVERAGES

Source: madisonsreport.com

More Reports: