True Spring Weather And Ongoing Low Inventory Volumes Served To Bring Enough

New Demand For Lumber Prices To Increase Somewhat.

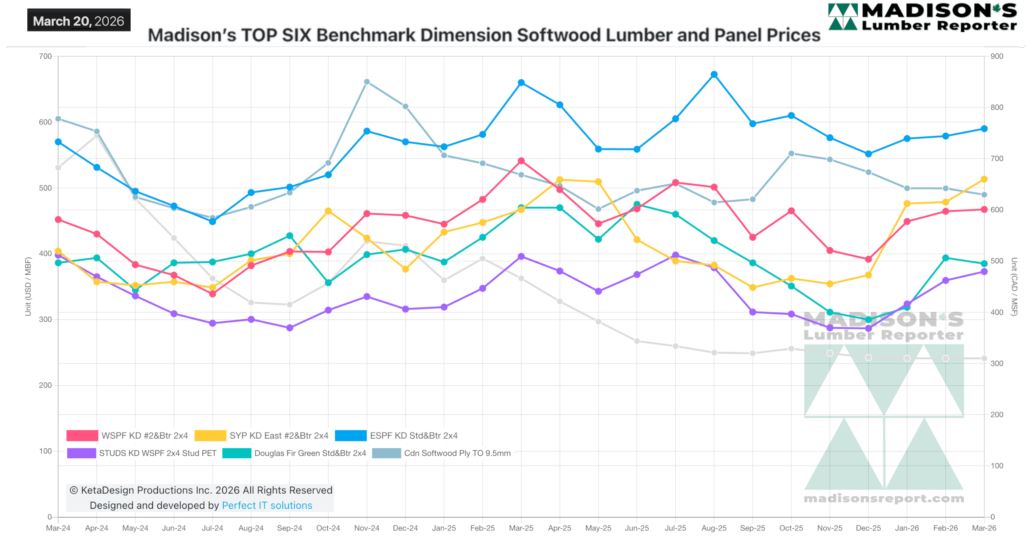

The graphs attached here show a good, stable trend-line over the past two

years, with prices ranging approximately $200 between the lowest and the

highest points annually. So far in 2026 prices are right in the middle of

that range.

While customers remained cautious, the inevitable oncoming construction

season brought an increase in sales. Sawmills across North America continue

at lower production volumes, so order files stretched out in mid-April and

prices rose slightly.

Further uncertainty globally, both with trade and more dramatic

developments, only made things more confusing.

Specifically regarding transportation, which was already a serious issue for

lumber buyers and sellers this year; both trucking and rail are expected to

become even more of a challenge. Delivery time, and costs, will grow

accordingly.

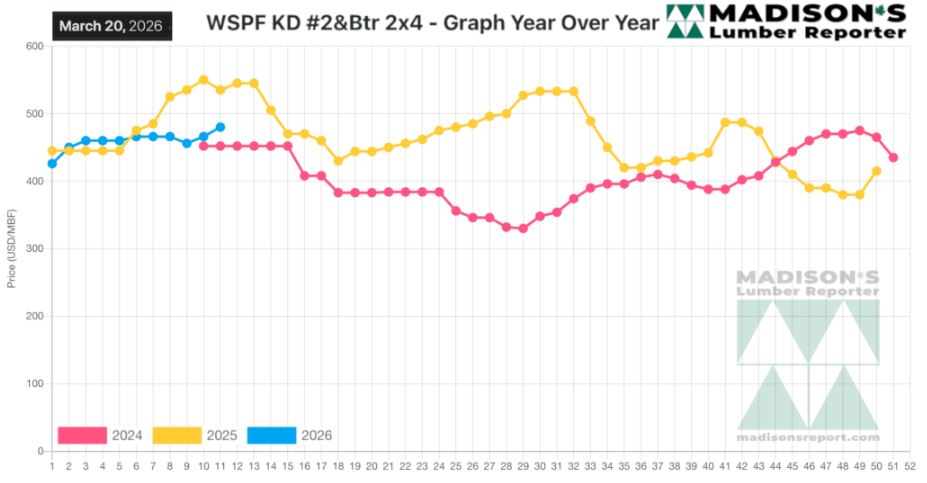

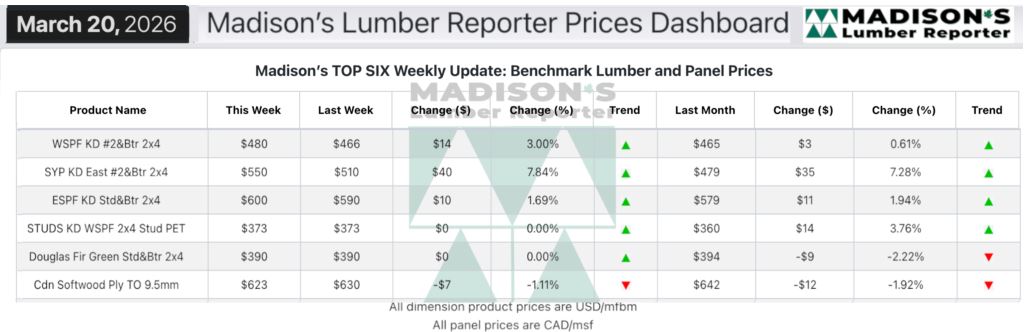

In the week ending March 20, 2026 the price of Western Spruce-Pine-Fir 2×4

#2&Btr KD (RL) was US$480 mfbm, which was up +$14, or +3%, from the previous

week when it was $466, said weekly forest products industry price guide

newsletter Madison’s Lumber Reporter.Wood & Plastics

That week’s price was up +$16, or +3%, from one month ago when it was $465.

Compared To The Same Week Last Year, When It Was Us$535 Mfbm, The Price Of

Western Spruce-Pine-Fir 2×4 #2&Btr Kd (Rl) For The Week Ending March 20,

2026 Was Down -$55, Or -10%.

Compared To Two Years Ago When It Was $452, That Week’S Price Was Up +$28,

Or +6%.

The upward trend in demand for Southern Yellow Pine and

Spruce-Pine-Fir commodities continued, while sales of panels still lagged.

Eastern Canadian traders lamented persistently awful business in Southern

Ontario.

KEY TAKE-AWAYS:

KEY TAKE-AWAYS:

Sellers of Western-SPF in the US reported a relatively busy week as

strengthening prices brought out many heretofore reluctant buyers.

Prices of many key dimension and stud items were incrementally boosted.

Purchasers had to work extra hard to find their preferred mix of lengths,

grades, and origin-destination pairings.

Sawmills extended their order files into the first half of April.

Suppliers of Western-SPF in Canada were encouraged by sporadically improving

demand, and breaking weather in many regions.

Transportation continued a real challenge; specifically sharply rising

freight rates, as well as lack of equipment and operator availability.

Just south of the border the Great Lakes market was quite busy according to

Eastern-SPF traders in the United States.

The surge in Southern Yellow Pine sales went on unabated as spring demand

continued to come online.

Treaters showed plenty of participation as they looked to shore up their

positions in advance of fulfilling their own quoted production volumes.

Sawmills in the US south showed thin lists and inconsistent tallies, adding

further frustration to a market that was already strained.

MADISON’S BENCHMARK TOP-SIX SOFTWOOD LUMBER AND PANEL PRICES: MONTHLY

AVERAGES

Source: madisonsreport.com

More Reports: