As March Drew To A Close Many Lumber Prices Started To Rise Slightly. Levels

Currently Were Right In The Middle, Between Those Of The Same Time Last Year

And In 2024.

Despite an extended winter and soft demand, this is encouraging to industry

as regular seasonal price stability is best for planning.

Expectations for housing construction this year are for similar activity to

last year, however no one really knows. At this time of great upheaval and

much uncertainty, it is not clear how business will be as summer comes on.

For their part, sawmills had no plans to ramp up production volumes until

there were obvious signs that improved demand will be ongoing. Customers,

behaving with equal caution, continued to not stock inventory.

If home building does increase this year, the very weak field inventories

throughout the supply chain might become a problem for end-users.

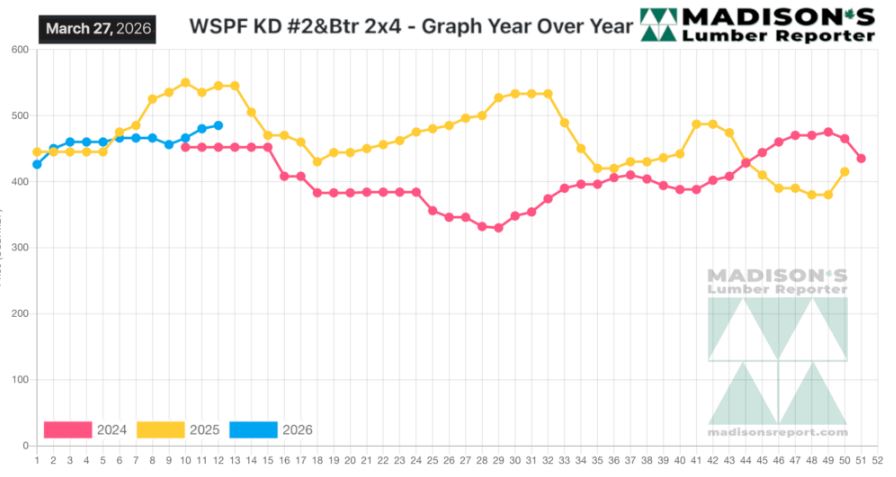

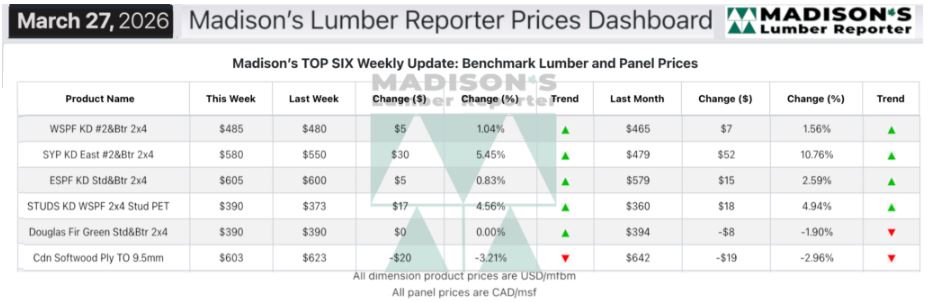

In the week ending March 27, 2026, the price of benchmark softwood lumber

item Western Spruce-Pine-Fir 2? #2&Btr KD (RL) was US$485 mfbm. This was up

+$5, or +1%, from the previous week when it was $480, said weekly forest

products industry price guide newsletter Madison’s Lumber Reporter.

That week’s price was up +$21, or +4%, from one month ago when it was $465.

Compared To The Same Week Last Year, When It Was Us$545 Mfbm, The Price Of

Western Spruce-Pine-Fir 2? #2&Btr Kd (Rl) For The Week Ending March 27,

2026 Was Down -$60, Or -11%.

Compared To Two Years Ago When It Was $452, That Week’S Price Was Up +$33,

Or +7%.

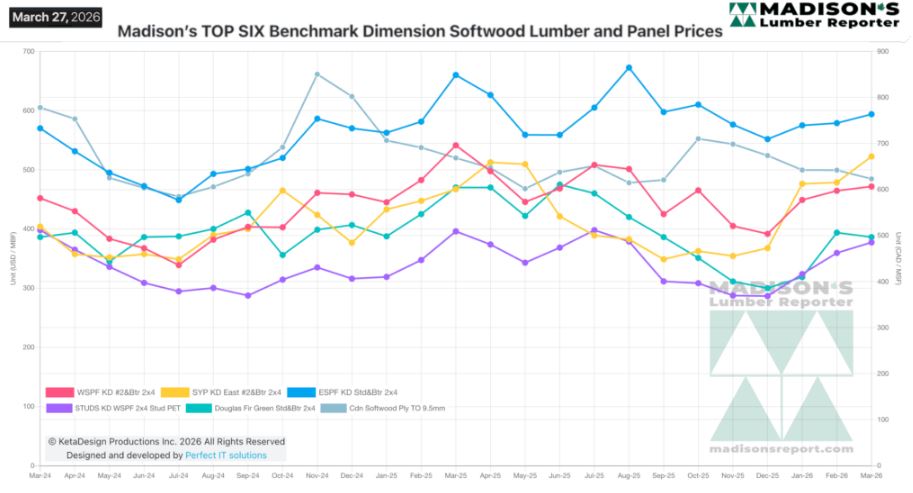

Most lumber prices rose, in a somewhat fragile manner, except Southern

Yellow Pine and plywood which popped upward.

KEY TAKE-AWAYS:

KEY TAKE-AWAYS:

Buyers of Western-SPF in the US jammed suppliers’ phone lines.

Inquiries were either to fill holes in thin inventories or check on

previously-ordered material due to delivery delays.

Sellers described the market as fragmented.

Canadian suppliers of Western-SPF pointed out that inquiry and sales were

slow.

Strengthening prices, tight supply, and tenuous demand combined to lend an

air of fragility to an otherwise robust tone.

Sawmills spent a lot of time dealing with enduring issues of rising freight

rates in the transportation sector.

Successful transactions for Eastern-SPF were more dependent on reload and

freight logistics than on mill availability.

Low-grade items were a tricky gambit for US buyers as duties and tariffs on

Canadian lumber all but shut off those exports.

Order files were pushing into mid-April, sawmills slowly extended lead times

as they nudged prices up.

Suppliers of Southern Yellow Pine boosted their asking prices again across

all regions and items with few exceptions.

Eastern Stocking Wholesalers reported Douglas-fir commodity prices were flat

but firm.

Rush loads were a thing of the past, and spring had only just sprung.

MADISON’S BENCHMARK TOP-SIX SOFTWOOD LUMBER AND PANEL PRICES: MONTHLY

AVERAGES

Source: madisonsreport.com

More Reports: