There Was No Noticeable Increase In Demand For North America Construction

Framing Dimension Softwood Lumber In The Middle Of April.

Prices remained mostly flat, with some items correcting down slightly.

Players spent a lot of time tracking down where was delivery of their solid

wood products already ordered.

Sellers were managing the location of trucks and rail cars which had not yet

arrived to waiting customers. Customers repeatedly called back to suppliers

asking that very question.

During all this, prices of most lumber commodities hovered very close to the

levels of same week last year and in 2024. This, at least, was one aspect of

business that provided some consistency and clarity.

As for the rest, industry folks could only do their best to manage the

continued uncertainty and unknowns with macroeconomic conditions.

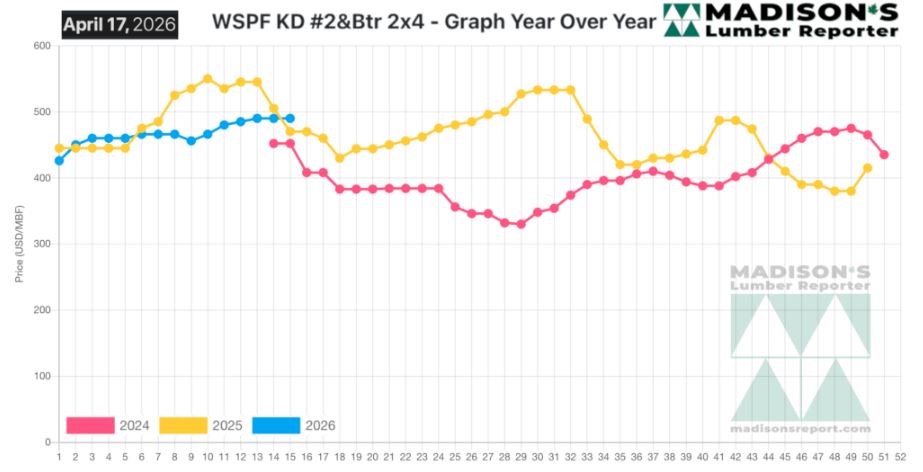

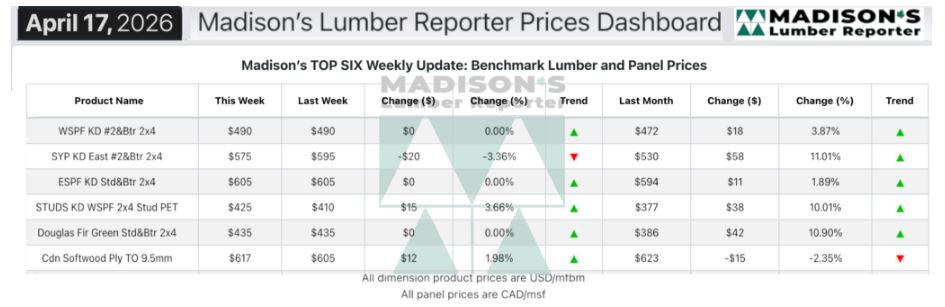

In the week ending April 17, 2026 the price of Western Spruce-Pine-Fir 2×4

#2&Btr KD (RL) was US$490 mfbm, which was flat from the previous week, said

weekly forest products industry price guide newsletter Madison’s Lumber

Reporter.

That week’s price was up +$18, or +4%, from one month ago when it was $472.

Compared To The Same Week Last Year, When It Was Us$470 Mfbm, The Price Of

Western Spruce-Pine-Fir 2×4 #2&Btr Kd (Rl) For The Week Ending April 17,

2026 Was Up +$20, Or +4%.

Compared To Two Years Ago When It Was $452, That Week’S Price Was Up +$38,

Or +8%.

Lumber demand continued to be broadly supply-driven, with limited

availability propping up prices even as many buyers took the week to step

back, digest, and reassess.

KEY TAKE-AWAYS:

KEY TAKE-AWAYS:

Prices of bread-and-butter Western-SPF commodities in the US were firm or

slightly up.

Players agreed on a situation of persistently subpar spring buying activity.

Buyers of Western-SPF in Canada were cautious, and unwilling to carry

inventory for more than 30 days.

Rising rail and truck rates were an undeniable thorn in everyone’s side.

Eastern-SPF sawmills maintained their asking prices across virtually every

item.

Sustained demand and consumption of lower grades indicated a strong

undercurrent of industrial sales that remained persistent.

Multiple sources reported Southern Yellow Pine prices felt toppy.

A sustained undercurrent of SYP demand from pallet & crating manufacturers

and other industrial buyers kept those prices more buoyant.

Commodity prices were trending upward in the tri-state area, according to

Eastern Stocking Wholesalers.

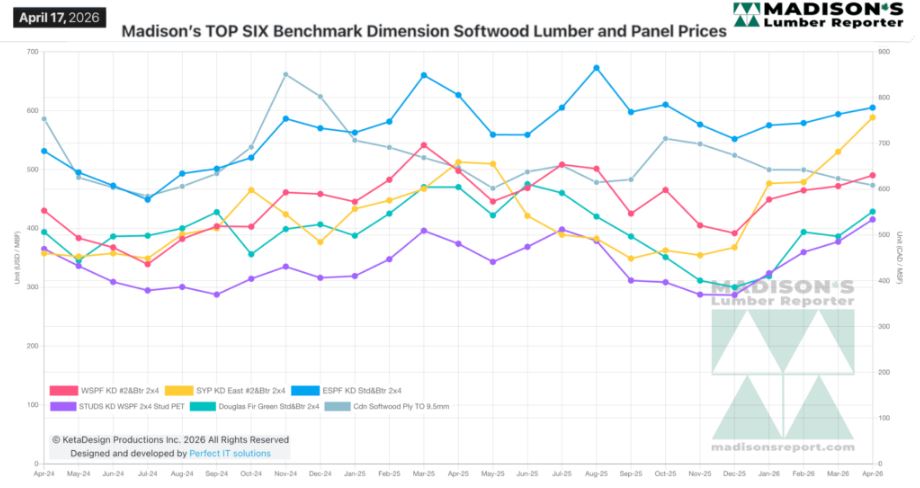

MADISON’S BENCHMARK TOP-SIX SOFTWOOD LUMBER AND PANEL PRICES: MONTHLY

AVERAGES

Source: madisonsreport.com

More Reports: