The dual mid-May long weekends in canada and the us provided a break for

north america lumber sales.

Top of everyone’s minds was delivery; freight charges and tight supply of

trucks and rail cars. Conversations swirled about where was wood previously

ordered in the supply chain, and what was the expected date of that arrival.

There was some back-and-forth between customers and suppliers about placing

new orders for wood, but no one was thinking more than two or three weeks

out.

The sawmills were satisfied with their order files, which were in that time

range, and were unwilling to commit to sales beyond that for fear of a

change in prices. Buyers had a similar attitude, although some hunted around

for future deals to see if they could lock-in a purchase at current prices.

Generally speaking though this was more tire-kicking than actually placing

of orders.

On both sides of the border most thoughts were on grilling hot dogs and

other beginning-of-summer activities than on increasing lumber inventories.

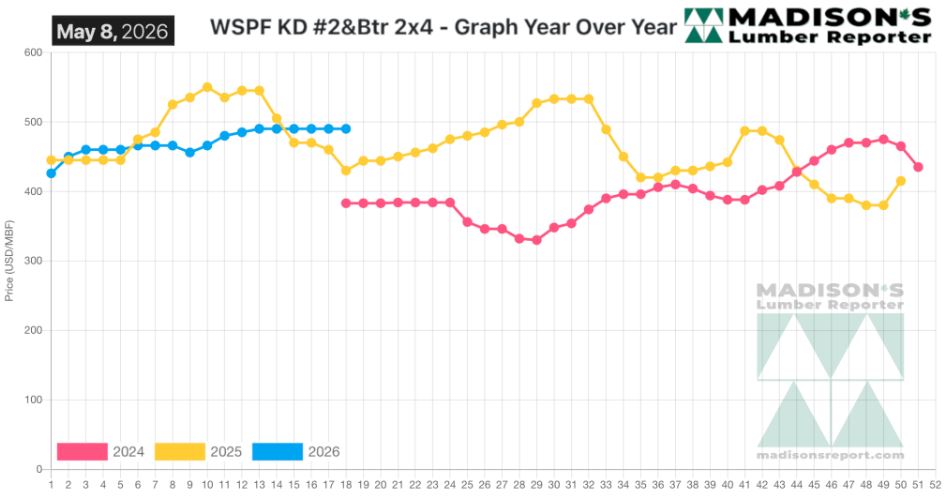

In the week ending May 8, 2026 the price of Western Spruce-Pine-Fir 2×4

#2&Btr KD (RL) was US$490 mfbm, which was flat from the previous week, said

weekly forest products industry price guide newsletter Madison’s Lumber

Reporter.

That week’s price was flat from one month ago when it was $490.

Compared To The Same Week Last Year, When It Was Us$430 Mfbm, The Price Of

Western Spruce-Pine-Fir 2×4 #2&Btr Kd (Rl) For The Week Ending May 8, 2026

Was Up +$60, Or +14%.

Compared To Two Years Ago When It Was $383, That Week’S Price Was Up +$107,

Or +28%.

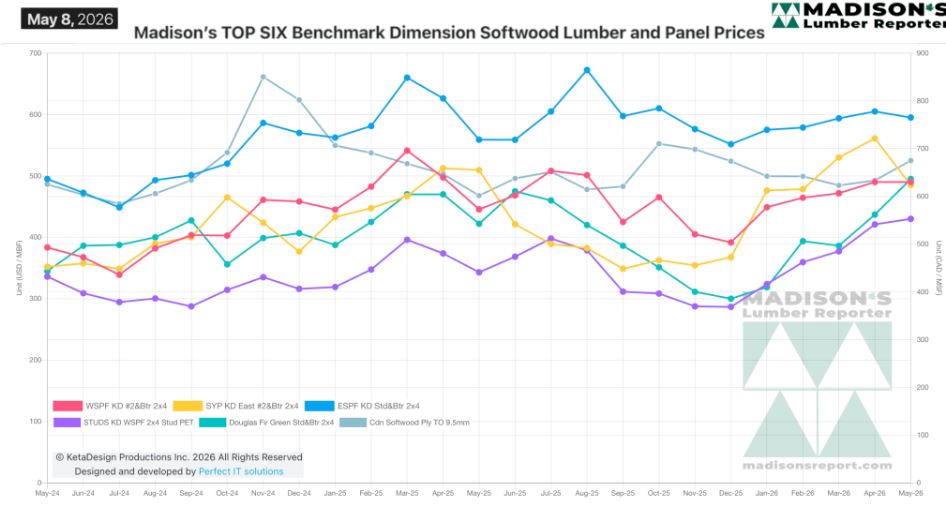

Most lumber prices were flat while Southern Yellow Pine continued to

search for a reliably tradable bottom.

KEY TAKE-AWAYS:

KEY TAKE-AWAYS:

There wasn’t enough production of Western-SPF in the US to allow buyers

slack to make counter-offers.

Western-SPF suppliers in Canada had sustained inquiry and takeaway from

buyers which kept both sawmills and distributors busy.

Sentiment among customers remained cautious, as they committed only to

coverage in a near-term, two- to four-week, range.

On May 1st, the UP and BN railroads added another $6 to $10 per thousand in

fuel surcharges, substantially increasing shipping costs per rail car.

Trucking availability remained tight across Western Canada, with limited

capacity reducing flexibility on prompt orders.

Eastern-SPF mills maintained order files in a roughly three-week range.

As buyers refused to build inventory in anticipation of spring jobs,

distributors and sawmills also avoided carrying or processing excess

inventory.

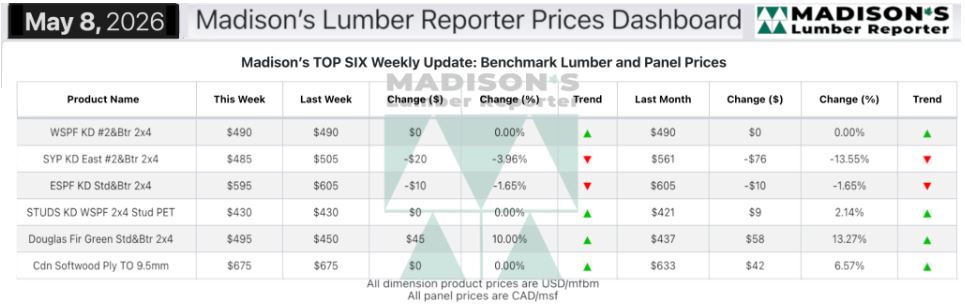

Producers of Southern Yellow Pine now had order files, so buyers who needed

quick coverage had to pay to get it.

Commodity prices and tight supply increasingly occupied the minds of Eastern

Stocking Wholesalers.

Vendors in the tri-state area faced the fact their cross-country shipments

were subject to sky-high freight rates.

MADISON’S BENCHMARK TOP-SIX SOFTWOOD LUMBER AND PANEL PRICES: MONTHLY

AVERAGES

Source: madisonsreport.com

More Reports: