There Was No Sense Of Urgency In The Week Prior To Canada’S May Long

Weekend, With The Us Heading Into Theirs The Following Weekend.

While lumber sales were proceeding at nominal volumes, there remained

external factors causing issues. Specifically deliveries were a big

uncertainty, both in regard to sourcing trucks and rail cars and with

increasing fuel charges. Some buyers used this temporary lull as an

opportunity to hunt around for deals, but suppliers refused to commit to

price quotes beyond three weeks out.

The ongoing situation of very lean inventories throughout the supply chain

did not seem to trouble customers much. For their part, sawmills continued

to keep manufacturing volumes low to prevent lumber prices from falling

further.

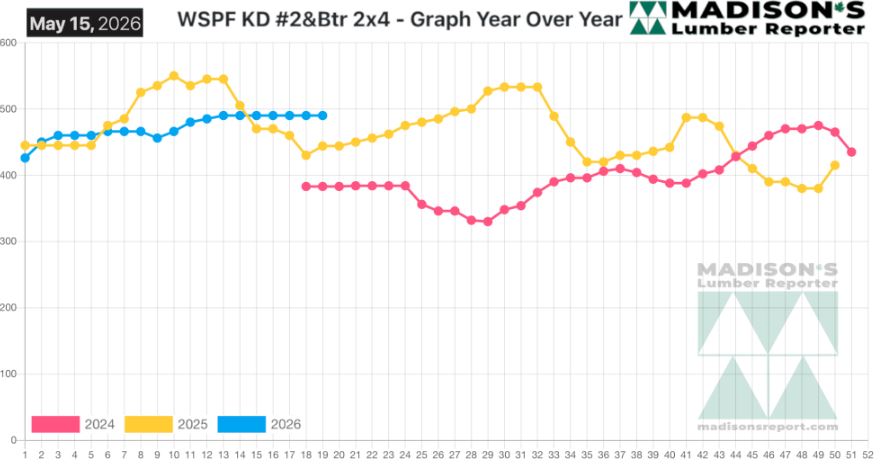

Currently, in the middle of May 2026, the price trendlines of the three main

benchmark 2×4 dimension lumber items — Western and Eastern-SPF and Southern

Pine East Side — were nicely within close range for the same week last year

and in 2024.

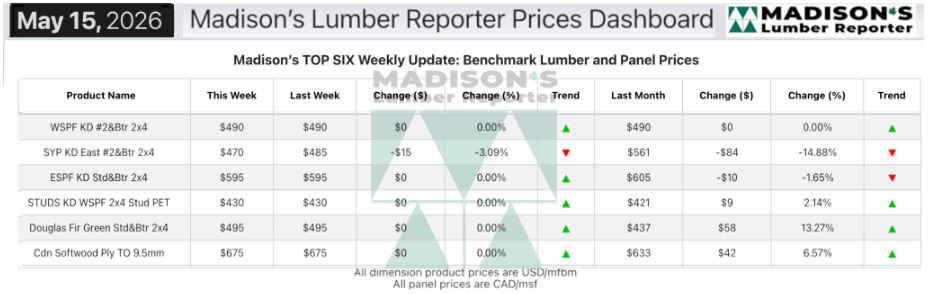

In the week ending May 15, 2026, the price of benchmark softwood lumber item

Western Spruce-Pine-Fir 2×4 #2&Btr KD (RL) was US$490 mfbm. This was flat

from the previous week, said weekly forest products industry price guide

newsletter Madison’s Lumber Reporter.

That week’s price was flat from one month ago.

Compared To The Same Week Last Year, When It Was Us$444 Mfbm, The Price Of

Western Spruce-Pine-Fir 2×4 #2&Btr Kd (Rl) For The Week Ending May 15, 2026

Was Up +$46, Or +10%.

Compared To Two Years Ago When It Was $383, That Week’S Price Was Up +$107,

Or +38%.

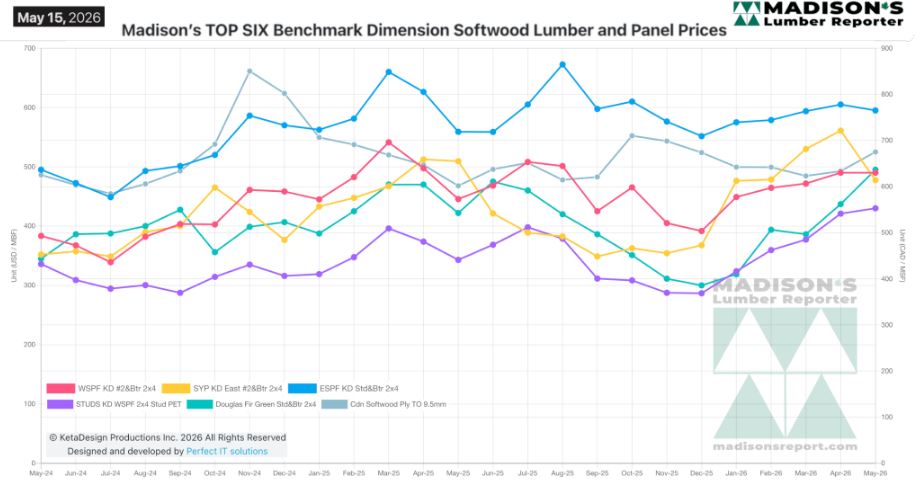

Prices of Western- and Eastern-SPF settled into a holding pattern

while Southern Yellow Pine slid further. Panel prices seemed to have topped

out, but it was hard to tell.

KEY TAKE-AWAYS:

KEY TAKE-AWAYS:

Some traders of Western-SPF in the US decried weak conditions while others

thought demand looked pretty good.

Distributors and buyers were content to play it close while the market was

mired in uncertainty.

Sawmills adopted a similar aspect, refusing to build order files while they

felt the market wasn’t firing on all cylinders.

Overall supply remained tight however, limiting any potential for downward

pressure on pricing.

As for Western-SPF in Canada, there were many reports of mills pushing out

buildups of material at notable discounts to print.

Prompt shipments often ended up behind schedule, particularly when

originating out of Northern BC.

Eastern-SPF producers suffered hit-or-miss business.

ESPF secondary suppliers in the US bought more than they sold over the past

two weeks, in a period of seasonal weakness.

Southern Yellow Pine commodities continued to trend downward in search of a

price bottom.

SYP buyers looking for specific mixes or cleaner lengths had a tough time.

MADISON’S BENCHMARK TOP-SIX SOFTWOOD LUMBER AND PANEL PRICES: MONTHLY

AVERAGES

Source: madisonsreport.com

More Reports: