June Arrived To Forest Products And Building Materials Industry Folks

Acknowledging The Reality Of Ongoing Tight Supply.

The rapidly increasing transportation costs only made the difficulty of

sourcing solid wood products at lower prices more severe. Customers with the

mentality of prior economics found themselves stymied by sellers who refused

even small counter-offers. As sawmill order files ranged into the end of

this month, lumber producers were unwilling to offer discounts.

The now-entrenched practice of not stocking inventory came to a head in

mid-June as a bullish movement of lumber Futures caused more customers to

place orders, since they felt confirmed that prices would not go lower soon.

Continued production cuts and lean supply resulted in a lack of available

prompt wood.

As such, customers scrambled to contact all their various sources in search

of the products they needed. Often to come up short, and have to wait longer

for their new orders to arrive.

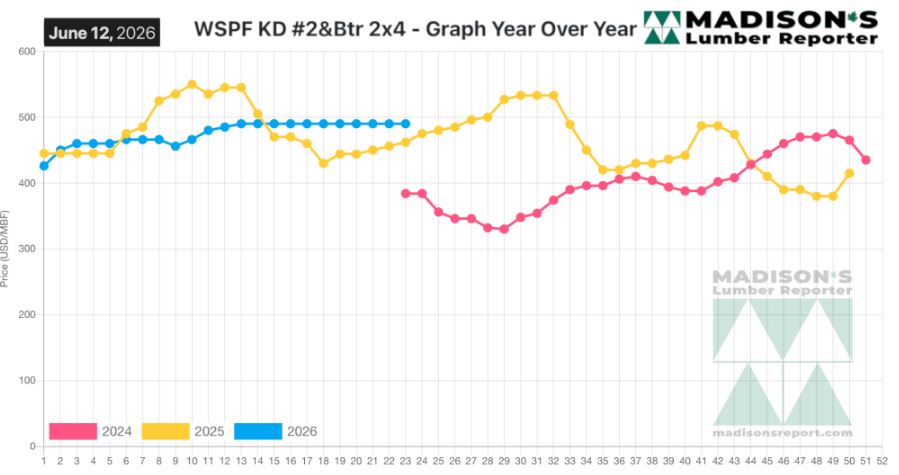

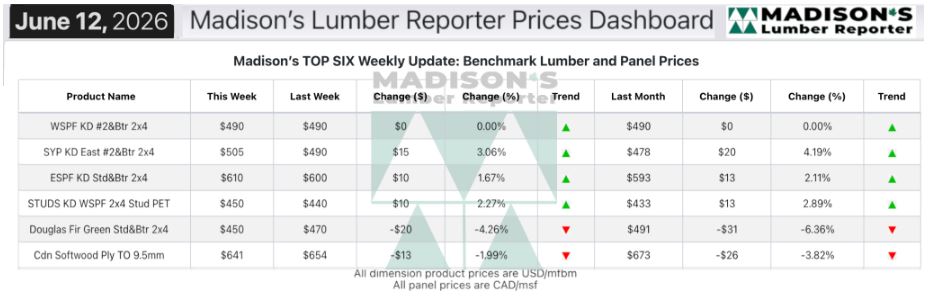

In the week ending June 12, 2026, the price of benchmark softwood lumber

item Western Spruce-Pine-Fir 2×4 #2&Btr KD (RL) was US$490 mfbm.

This was flat from the previous week, said weekly forest products industry

price guide newsletter Madison’s Lumber Reporter.

That week’s price was flat from one month ago.

Compared to the same week last year, when it was us$462 mfbm, the price of

western spruce-pine-fir 2×4 #2&btr kd (rl) for the week ending June 12, 2026

was up +$28, or +6%.

Compared to two years ago when it was $384, that week’s price was up +$106,

or +28%.

Northwestern and Southern lumber item prices showed positive trends,

while Coastal species (Hemlock and Douglas Fir KD) prices were flat by

comparison.

KEY TAKE-AWAYS:

KEY TAKE-AWAYS:

Buyers of Western-SPF in the US had difficulty finding wood at the sawmill

level, especially for specific mixes on clearcut timelines.

Western-SPF sellers in Canada were encouraged by several trends which seemed

to point to an upward price trajectory.

Discounted materials were not as prevalent and delivery timelines weren’t as

flexible as in recent weeks.

Commodity prices continued to show firmness while freight costs marched

upward.

Any product that landed in vendor yards was spoken for almost immediately.

The undersupplied state of the Eastern-SPF market was exposed in a big way

as buyers increasingly saw no-quotes from sawmills.

Suppliers of Southern Yellow Pine reported every order was a tug of war.

Eastern Stocking Wholesalers remained in the ongoing situation of limited

supply running up against anemic demand.

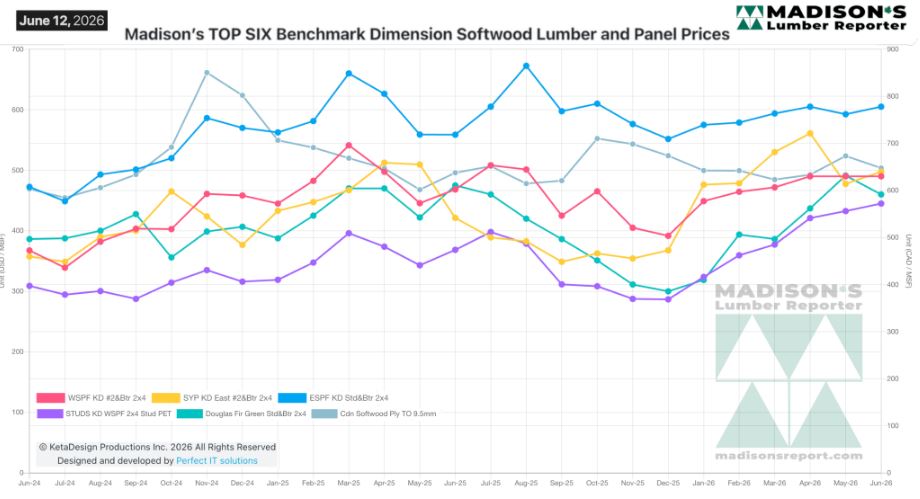

MADISON’S BENCHMARK TOP-SIX SOFTWOOD LUMBER AND PANEL PRICES: MONTHLY

AVERAGES

Source: madisonsreport.com

More Reports: