Contrary to the usual seasonal trend historically, late-June construction

framing softwood lumber prices rose somewhat this year.

Traditionally by this time most customers had ordered, and indeed received,

the wood they needed for summer building projects. As prices have generally

started softening, the trend lines tend to drop starting in June.

This, of course, is not every single year as disruptions like labour

disputes, transportation delays, wildfires, or an unexpected spike in new

home building have at times increased lumber prices during summer.

In 2026 it seems the reason for flat-to-higher wood prices is the ongoing

decrease of supply. As the continent heads into the truly hot months, when

Québec takes its annual 2-week restriction on industrial operations and

construction, as well as

other regions where high temperatures prohibit this kind of activity; the

balance of supply-and-demand will become more clear.

At this point, no one knows how the lumber market will play out through July

and into August.

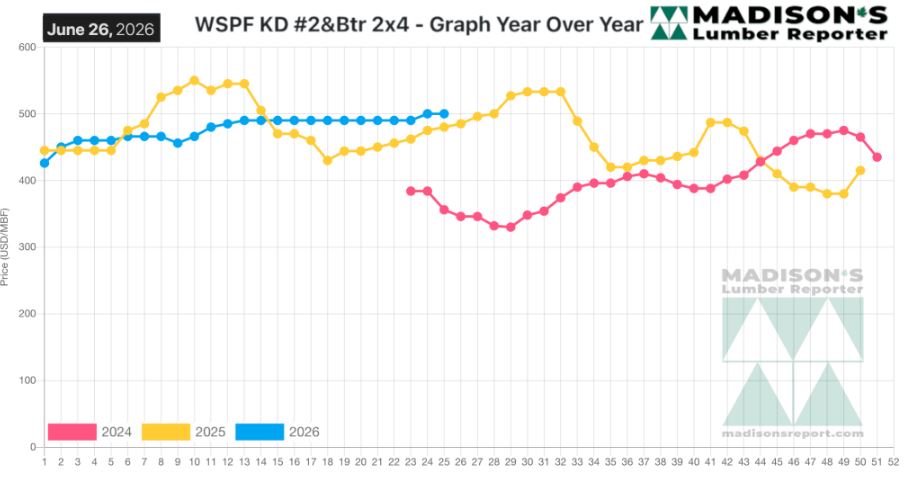

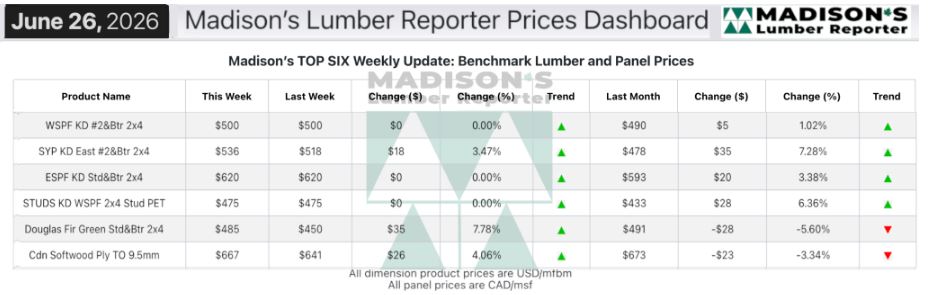

In the week ending June 26, 2026, the price of benchmark softwood lumber

item Western Spruce-Pine-Fir 2×4 #2&Btr KD (RL) was US$500 mfbm.

This was flat from the previous week, said weekly forest products industry

price guide newsletter Madison’s Lumber Reporter.

That week’s price was up +$59, or +12%, from one month ago when it was $478.

Compared to the same week last year, when it was us$400 mfbm, the price of

western spruce-pine-fir 2×4 #2&btr kd (rl) for the week ending June 26, 2026

was up +$20, or +4%.

Compared to two years ago when it was $356, that week’s price was up +$144,

or +40%.

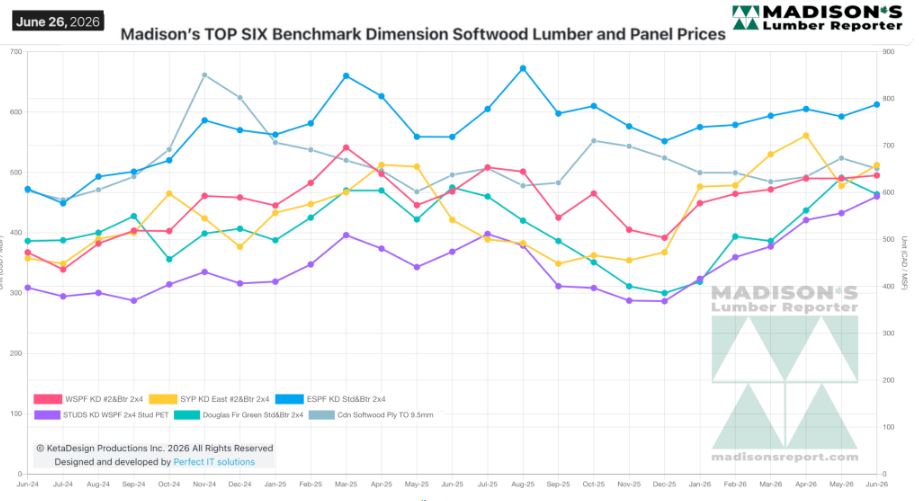

Hemlock/fir and Douglas-fir prices surged as that of Plywood showed

some sneaky strength in the background.

KEY TAKE-AWAYS:

• Overall supply of Western-SPF in the US was persistently well-short of

typical levels for this time of year.

• Sales of Western-SPF in Canada was considered one of the best showings so

far in 2026.

• Downstream consumption was steady.

• Fibre baskets across the continent were beset by hot and dry weather, with

severe wildfires already erupted.

• Some customers did their best to hold off buying if they had positions to

sit on, but most were reluctantly forced to pay higher prices.

• Limited state of supply of Eastern-SPF was increasingly apparent as

sawmills showed firm or upward pricing.

• Buyers in the East scrambled to cover short-term inventory needs.

• Buyers of Southern Yellow Pine with thin inventory positions were tearing

out their hair searching for amenable tallies in definable delivery times.

• Reports indicated that many southern mills were running upwards of two

weeks behind on shipments.

MADISON’S BENCHMARK TOP-SIX SOFTWOOD LUMBER AND PANEL PRICES: MONTHLY

AVERAGES

Source: madisonsreport.com

More Reports: